“I don’t think we’ll have a long-lasting Great Depression…. But we may have a different kind of a mess. All this money-printing may start bothering us.”

By Wolf Richter for WOLF STREET.

There is something refreshing during these insane times when a guy in his mid-90s who has seen it all and has been successful at navigating it, and who, during the last Financial Crisis, was buying stocks and entire companies hand over-fist, now says that he has never seen anything like this before, and that he doesn’t know what to do except to sit tight. And they’re not buying the rally, and they weren’t buying the crash.

Charlie Munger, vice chairman of Berkshire Hathaway, was talking with The Wall Street Journal about the current situation and how he and Warren Buffett are looking at it. And they’re not buying.

During the Financial Crisis, they were lending money to Goldman Sachs and GE and getting warrants too that turned out to be very profitable, and they bought stocks, and they bought BNSF outright after the partial stake they’d acquired before the Financial Crisis went sour.

But today’s situation is different.

“Well, I would say basically we’re like the captain of a ship when the worst typhoon that’s ever happened comes,” he told The Wall Street Journal. “We just want to get through the typhoon, and we’d rather come out of it with a whole lot of liquidity. We’re not playing, ‘Oh goody, goody, everything’s going to hell, let’s plunge 100% of the reserves [into buying businesses].’”

“We’re always going to be on the safe side. That doesn’t mean we couldn’t do something pretty aggressive or seize some opportunity. But basically, we will be fairly conservative. And we’ll emerge on the other side very strong.”

And when the Journal asked him if executives of big companies aren’t now approaching Berkshire and asking capital – as they’d done during the Financial Crisis – he said, “No, they aren’t.”

“The typical reaction is that people are frozen,” he said. “Take the airlines. They don’t know what the hell’s doing. They’re all negotiating with the government, but they’re not calling Warren. They’re frozen. They’ve never seen anything like it. Their playbook does not have this as a possibility.”

“And the phone is not ringing off the hook,” he said. “Everybody’s just frozen in the position they’re in.”

“Take the airlines,” he said. OK, let’s.

Airline stocks are revealing how the thinking of Munger and Buffett has changed about this crisis. Back on February 27, Berkshire bought another 976,000 shares of Delta (at about $46 a share), bringing their total stake to nearly 72 million shares, for an 11% stake.

On March 13, as airline stocks were careening lower, Buffett told Yahoo Finance: “I won’t be selling airline stocks.” Which boosted Delta shares to $38 a share for that day.

At the time, according to SEC filings cited by Yahoo Finance, Berkshire held, in addition to the nearly 72 million shares of Delta [DAL], over 53 million shares of Southwest [LUV], 42 million shares of American [AAL], and nearly 22 million shares of United [UAL].

But then all heck continued to break loose, and on April 3, it emerged in an SEC filing that Berkshire had unloaded a chunk of the airlines, selling 13 million shares of Delta and 2.3 million shares of Southwest, bringing in about $389 million in cash. Upon the news, but well after Berkshire had sold, the airlines tanked even more.

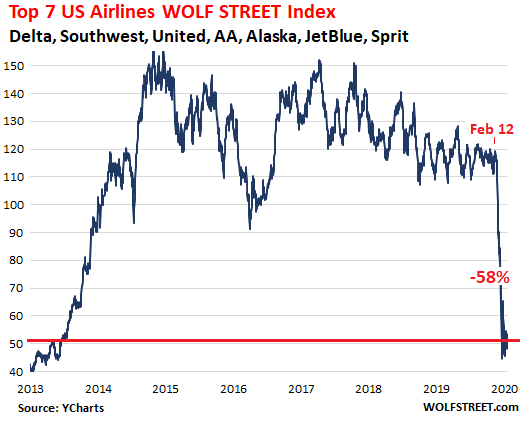

Airline stocks have barely ticked up during the historic spike of the broader market. The market-cap-based WOLF STREET Airlines Index, which tracks the seven largest US airlines, shows that together airlines are still near the March low. But it’s not a historic buying opportunity for Berkshire. Munger and Buffett decided to sell on the way down to lower the risk.

In the chart, the fat part at the bottom of the straight line indicates that the dictum on the WOLF STREET beer mugs – “Nothing Goes to Heck in a Straight Line” – after some serious doubts earlier, has once again been vindicated (market cap data via YCharts):

How long will this downturn last? How bad can it get?

“Nobody in America has ever seen anything else like this,” Munger said. “This thing is different. Everybody talks as if they know what’s going to happen, and nobody knows what’s going to happen.”

“Of course, we’re having a recession,” he said. “The only question is how big it’s going to be and how long it’s going to last. I think we do know that this will pass. But how much damage, and how much recession, and how long it will last, nobody knows.”

“I don’t think we’ll have a long-lasting Great Depression,” he said. “I think government will be so active that we won’t have one like that. But we may have a different kind of a mess. All this money-printing may start bothering us.”

“I do think, sooner or later, we’ll have an economy back, which will be a moderate economy. It’s quite possible that never again – not again in a long time – will we have a level of employment again like we just lost. We may never get that back for all practical purposes. I don’t know.”

In terms of Berkshire, he said that there would be damage too.

“This will cause us to shutter some businesses,” he said. “We have a few bad businesses that…we could be tolerant of as members of the family. Somebody else would have already shut them down. We’ve got a few businesses, small ones, we won’t reopen when this is over.”

And in terms of the stock market, he said, “I don’t have the faintest idea whether the stock market is going to go lower than the old lows or whether it’s not.”

Back in late 2008 and 2009, Buffett was out there on TV and in print, trying to calm panicked investors down, telling them that this was a once-in-a lifetime opportunity to buy stocks. In one of those efforts to get people to buy stocks and push the market higher, on October 16, 2008, after Lehman had collapsed, Buffett wrote in an Op-ed in the New York Times: “Be fearful when others are greedy, and be greedy when others are fearful.”

Now, instead of exhorting people to buy stocks, and instead of buying stocks and entire companies, Munger and Buffett sit on a huge pile of cash, and they added to that pile via the sale of airline stocks as they were collapsing, and they don’t know where this is going, and they don’t want to get run over by events, but they do want to come out on the other side of it more or less intact and have lots of liquidity ready in order to buy whatever deals might then be available.