Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Amid rampant market expectations of another and even bigger and grander round of QE by the ECB, which would also be buying corporate bonds and old bicycles, the total amount of bonds with negative yields has risen to nearly $13 trillion, according to Bank of America Merrill Lynch.

The perversion of negative interest rates imposed by central banks such as the ECB, the Bank of Japan, the Swiss National Bank and a slew of others, and the even bigger perversion of negative-yielding corporate debt apparently does a job on investors’ minds.

In a negative-yield environment, you can no longer buy bonds to hold them to maturity because you’d be guaranteed a loss. You’d have to buy them solely on the hopes of even more deeply negative yields in the near future that would allow you to slough off these critters to the next guy before they eat you up.

And this type of thinking has now completely wiped out whatever was left of investors’ capacity to act rationally. Once you start getting into central-bank mandated negative yields, rationality no longer applies because negative-yielding debt is irrational by definition: Why would you pay someone to borrow money from you?

And this type of intellectual short-circuit has now spread to euro-denominated junk bonds. These are risky bonds that are too risky to be considered “investment grate.” They were issued by over-leveraged companies with iffy or negative cashflows and a considerable probability of default, especially during a downturn.

And yes, you guessed it: there are now 14 junk-rated companies with euro-denominated bonds that have negative yields, according to Bloomberg:

- Ardagh Packaging Finance plc /Ardagh Holdings USA Inc.

- Altice Luxembourg SA

- Altice France SA

- Axalta Coating Systems LLC

- Constellium NV

- Arena Luxembourg Finance Sarl

- EC Finance Plc

- Nexi Capital SpA

- Nokia Corp.

- LSF10 Wolverine Investments SCA

- Smurfit Kappa Acquisitions ULC

- OI European Group BV

- Becton Dickinson Euro Finance Sarl

- WMG Acquisition Corp.

What does it even mean if you buy a junk bond with a negative yield?

If you’re lucky and the company does not default, it will redeem the bond at face value, and the company will pay you the face value of the bond on the date when the bond matures, plus accrued interest. Face value and the coupon payments over the term of the bond are all you’re going to get if you hold till maturity.

If the company defaults on the way — which is not unlikely, given its precarious financial condition that led to the junk credit rating in the first place — you’re out part or all of your principal investment. For taking this considerable risk, you’re being rewarded with a big yield, in theory.

But if you pay a lot more for the bond than face value, and if this premium you’re paying is bigger than the remaining interest payments, you end up in the hole, with a guaranteed loss unless you can sell the bonds to someone else at an even bigger premium and even greater negative yield before the bond matures.

But the closer you get to the maturity date of the bond, the closer the value of the bond will be to its face value, because on maturity date, face value and the interest that has accrued since the last interest payment are all you’re going to get.

What causes these junk bonds to have a negative yield is not some kind of magic but benighted investors whose brain is malfunctioning to the point that they bid up these bonds to such levels that the premium they pay over face value guarantees them a negative yield.

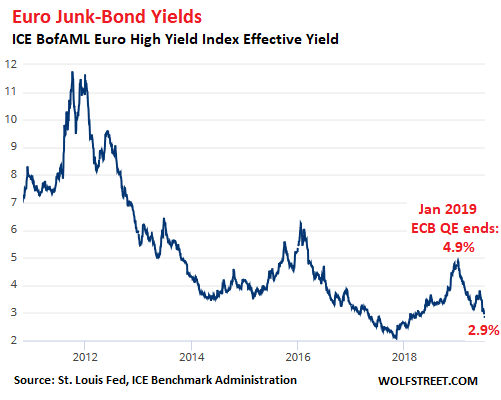

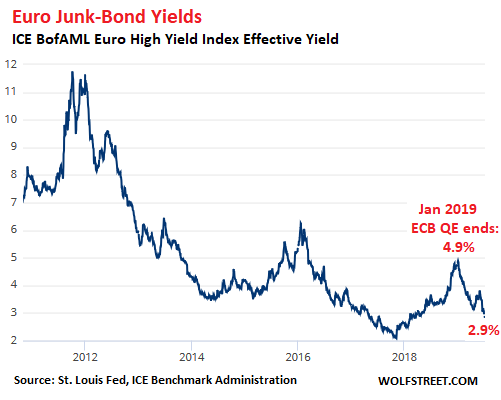

Not all euro junk bonds are adorned with a negative yield just yet. According to the ICE BofAML Euro High Yield Index, the average yield of these critters is 2.83% at the moment – down from 4.9% at the start of the year, when the ECB’s QE program ended:

Obviously, investors who’d bought euro junk bonds when euro junk bond yields were 10% or 6% or even 4% made out like bandits if they sold the bonds at current yields to some newcomers.

And these newcomers look at the above chart, and they see the trend that you can keep making out like bandits by buying junk bonds even at negative yields because surely yields will even be lower and more negative in the future, no matter what. And after years of central bank shenanigans and scorched-earth tactics, you can’t really blame these investors for having lost their minds and playing this idiotic game.