By Wolf Richter for WOLF STREET.

The used-vehicle wholesale market is normally very liquid. Millions of vehicles a year are run through these auction houses around the US and establish day-to-day pricing. The sellers are leasing companies, rental car companies, lenders with repossessed vehicles, and the like. These auctions are where dealers buy part of their used-vehicle retail inventory. The wholesale market is a crucial component in the vast and complex apparatus of the US auto industry that sells 17 million new vehicles and 40 million used vehicles in a good year. But sales at these auctions have collapsed.

In response to Covid-19, auction houses have now switched all auctions to simulcast, where buyers and sellers participate online. So now, after everyone got used to dealing with simulcast auctions, transactions have begun to tick up from catastrophically low levels to near-catastrophically low levels.

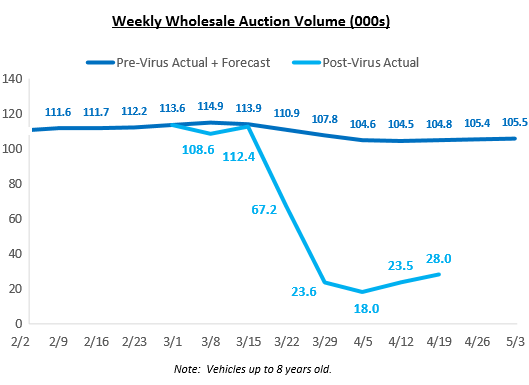

It sounded like this, from J.D. Power Valuation Services today: “Wholesale auction sales reached nearly 28,000 units the week ending April 19, a 19% lift over the prior week’s 23,500 units.”

In the good times through the week ended March 15, auction volume ran in the range from 109,000 to 114,000 vehicles a week. But then volume collapsed by 84% to 18,000 vehicles by the week ending April 5.

It is from this catastrophically low level of 18,000 units that sales via simulcast have started to rise to the still catastrophically low 28,000 units in the week ended April 19. Auction volume from mid-March through April 19 has plunged by 72% to just 160,000 units, down from 579,000 units in the same period last year.

In the chart from the report by J.D. Power Valuation Services, the light blue is actual sales; the dark blue is actual sales through February and then the old projections – now obviated by events – for the rest of the year:

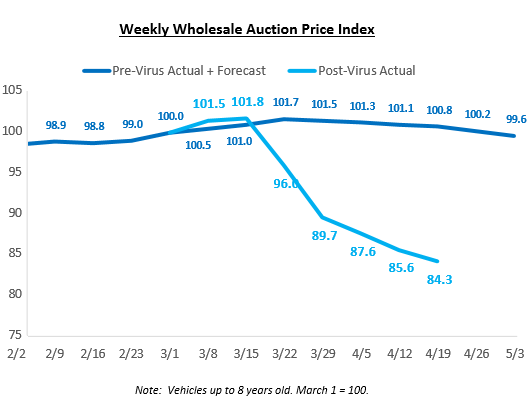

Wholesale prices of vehicles up to eight years old dropped 17% from the week ended March 15 through the week ended April 19, according to JD Power, and so far, there have only been relentless downticks – without upticks in sight (chart by J.D. Power Valuation Services):

Looking at this from the auction house’s point of view, Manheim, the largest auto auction house in the US and a unit of Cox Automotive, reported that price declines “accelerated over the last four weeks, with the first two weeks of April seeing a decline of 4.8% in the Three-Year-Old Index.” And it added:

It should be noted that, given the unprecedented downturn in sales and market disruption that the industry is experiencing because of the COVID-19 pandemic, the decline we have observed thus far in MMR [Manheim Market Report] values at the vehicle level and at all aggregation levels does not fully reflect the declines occurring in the relatively limited number of sales transactions taking place. Adjusting MMR for retention, which is the average difference in price relative to current MMR, results in a decline of 11.9% for 3-year-old since the end of March.

“Rental risk” vehicles have seen steeper price declines at auctions, Manheim reported. These are vehicles that rental car companies bought from automakers and that they have to sell later at whatever price the market might bear – as opposed to vehicles that they buy with repurchase guarantees from the automaker, where the automaker takes the risk associated with the resale value.

The average price for rental risk units sold at auction in the first 15 days of April plunged 17.1% year-over-year, and 18.5% from March.

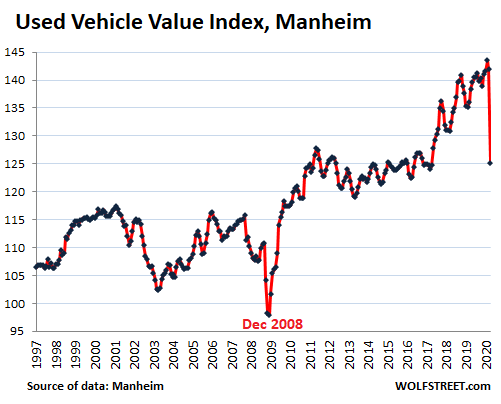

The broad Manheim Used Vehicle Value Index (which is mix-, mileage-, and seasonally adjusted), has so far in April dropped 9.6% compared to April a year ago. If it stays there for the rest of April, it will be the steepest drop ever in the data, far outpacing the prior year-over-year plunge-record of 5.5% set in November 2008:

This collapse in volume of the wholesale market – lack of demand from dealers – and the resulting price declines that are still getting worse, pose a large risk to:

- Leasing companies, from the smallest outfit to Ford Credit and big banks

- To rental-car companies for their rental risk units

- To automakers on their program rental units where they agreed to provide repurchase guarantees.

There are millions of vehicles per year that fall into these categories. And they all are collateral. Those inventories have been funded with debt.

The whole math of leases with a low monthly payment is pegged on a high resale value of the vehicle. A leasing company buys the vehicle and owns it. It then leases it to the customer. At lease-end, the customer turns the vehicle in, and the leasing company has to sell it. When proceeds from the sale are below the residual value figured into the lease, the leasing company loses money. This is no big deal if it happens on a few units. But it’s a huge deal if there are double-digit losses across the fleet that persist month after month as the constant flow of these units has to go through auction.

Rental car companies have a similar issue with their “rental risk” units: large potential losses built into their inventory that become apparent when they sell that inventory. This comes in addition to the swoon in revenues. Rental car companies have not been included in the bailout mania.

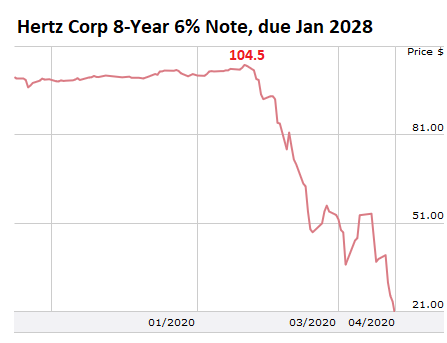

For example, Hertz shares [HTZ] have plummeted to $3.71 at the moment, from over $60 in 2016. Its bonds have collapsed. This eight-year 6% note, issued in November 2019 at around 100 cents on the dollar, and that traded at 104.5 cents on the dollar on February 21, closed today at 21 cents on the dollar (chart via Finra-Morningstar):

Hertz has hired restructuring and bankruptcy advisors, as have its lenders, the Wall Street Journal reported this afternoon.

Automakers like Ford, get hit from several sides. Ford Credit was the big money maker at Ford in recent years. But the resale value issues of its units that will be coming off lease – in addition to the credit problems associated with tens of millions of people suddenly losing their jobs – are going to put the hurt on it. Ford is also exposed through its rental program units that it will have to buy back from the rental-car companies at a price that will be higher than what Ford will be able to obtain at auction.

This impacts all automakers with captive leasing companies and that sell program cars to rental companies.

Then there is the volume issue: Auto sales are a constant flow. It starts with new vehicles that cycle through the system as they get older. The sales of new vehicles to leasing companies and rental-car companies by automakers in prior years become an onslaught of used-vehicle supply that no one can stop. These vehicles are coming down the pike whether anyone wants them or not.

And they must be sold, ultimately to a retail customer. But if retail demand has collapsed by 50% – which is about what preliminary numbers indicate – then the whole flow gets backed up.

Pricing solves those kinds of problems. Once prices drop far enough on the retail side, retail customers will gradually come out of the woodwork and poke around for deals. This mechanism works. But it’s this precise mechanism of lower prices to get the flow going that causes havoc among leasing companies and rental-car companies and their lenders, bond holders, and stockholders.

[Ah yes, I was just going to say that the Fed announced after hours that it will buy a million used vehicles at the auction and park them in its Special Purpose Vehicles (SPVs) to push up prices so that Americans will have to pay more for their used cars in order to bail out those stockholders, bondholders, and banks… I’m just kidding, I hope].