by jessefelder

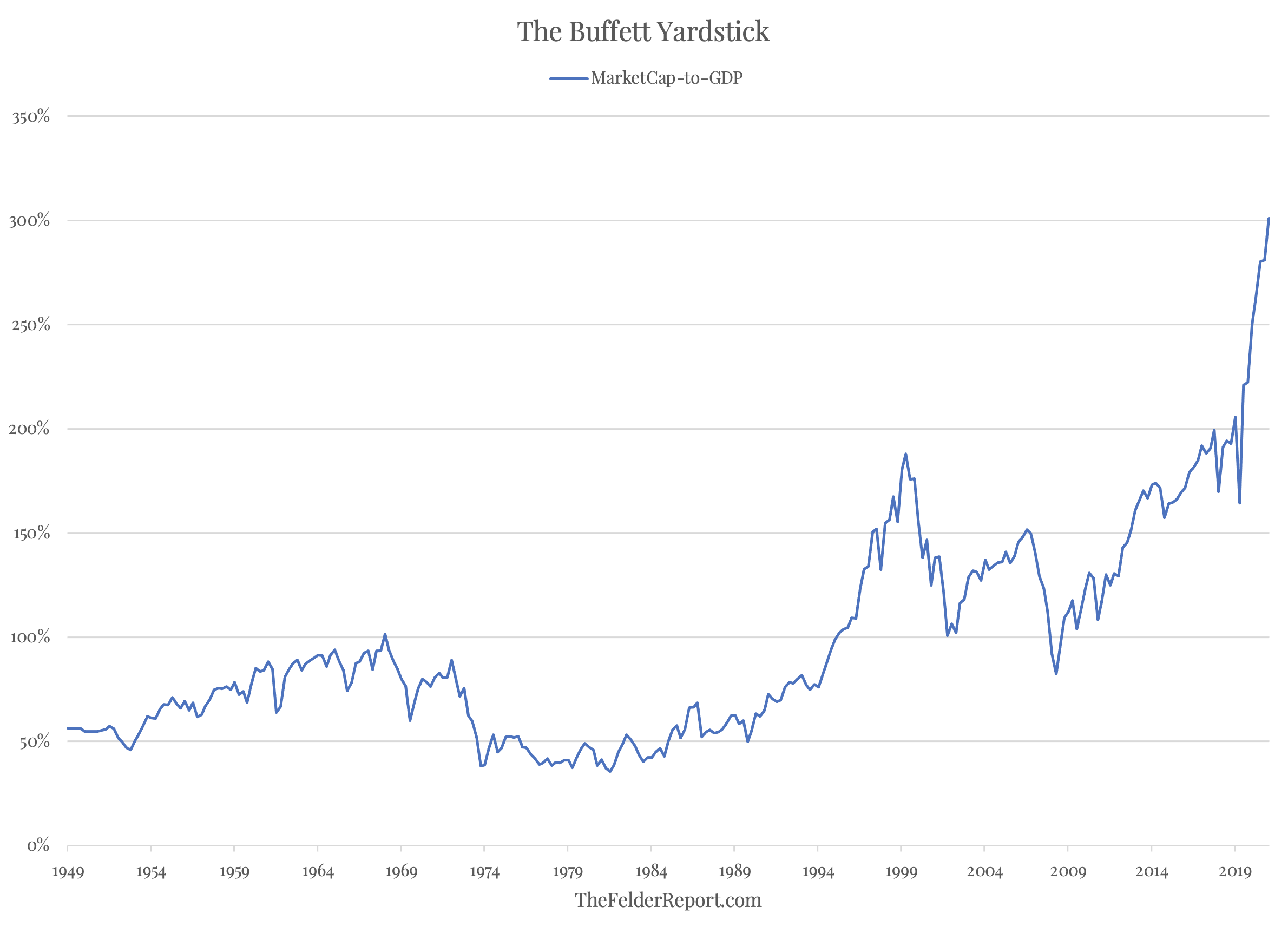

2021 is now in the books. Future historians will no doubt look back at the past two years and marvel at just how successful the dynamic duo of fiscal and monetary support was at levitating asset markets. It’s hard to look at the chart below and not be completely dumbfounded by it. To think that we looked at that quaint peak in valuations back in 2000 as the quintessential stock market bubble. Today’s stock market makes that earlier one look like child’s play in comparison.

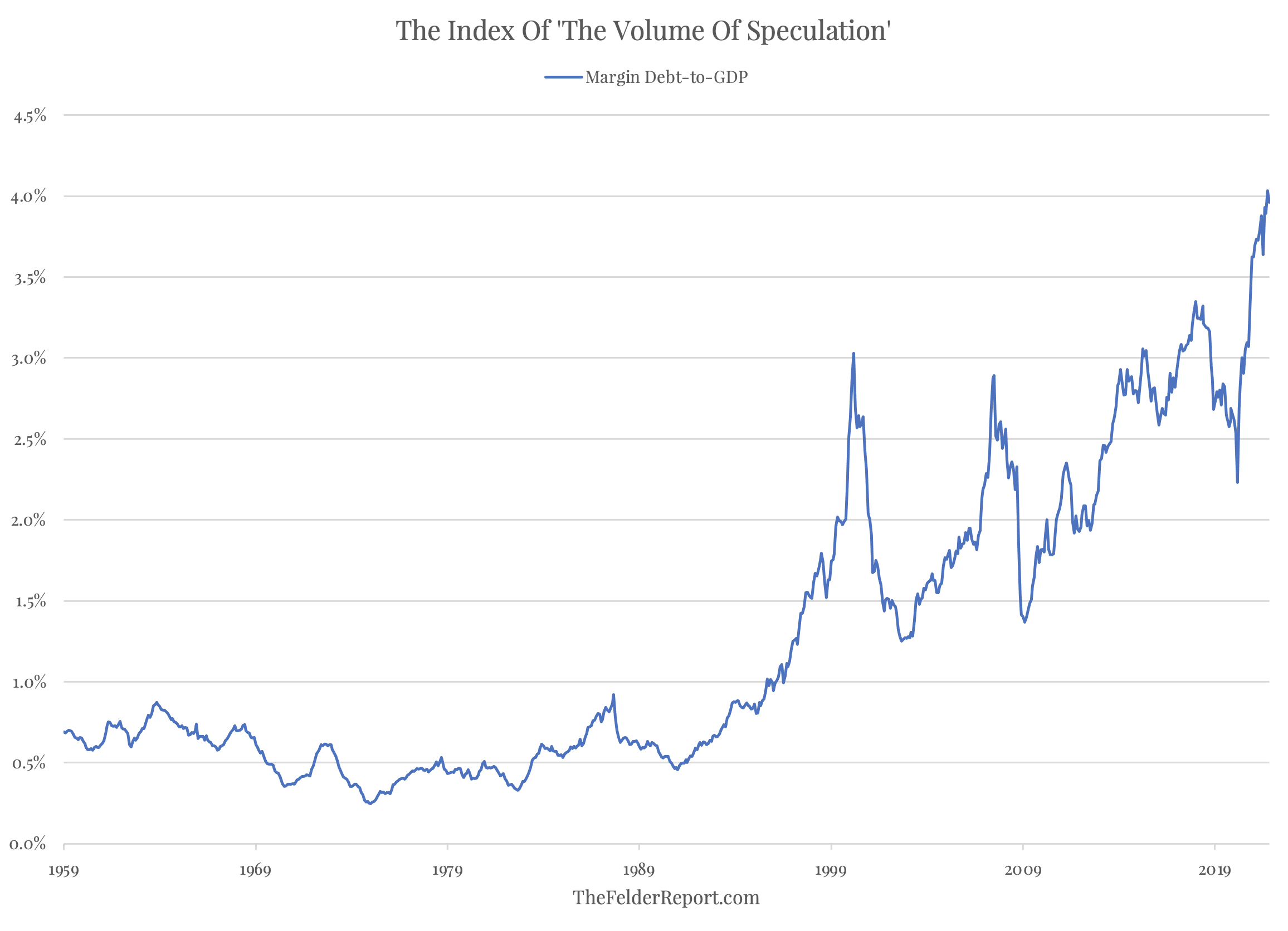

Indeed, the index of the “volume of speculation,” total margin debt in brokerage accounts as a percent of the economy, confirms the idea that we have recently seen a level of risk taking that we have never seen before. Investors have embraced the “greater fool theory,” and in a leveraged way, to a degree that exceeds anything prior including that famous “irrational exuberance” of the Dotcom Mania.

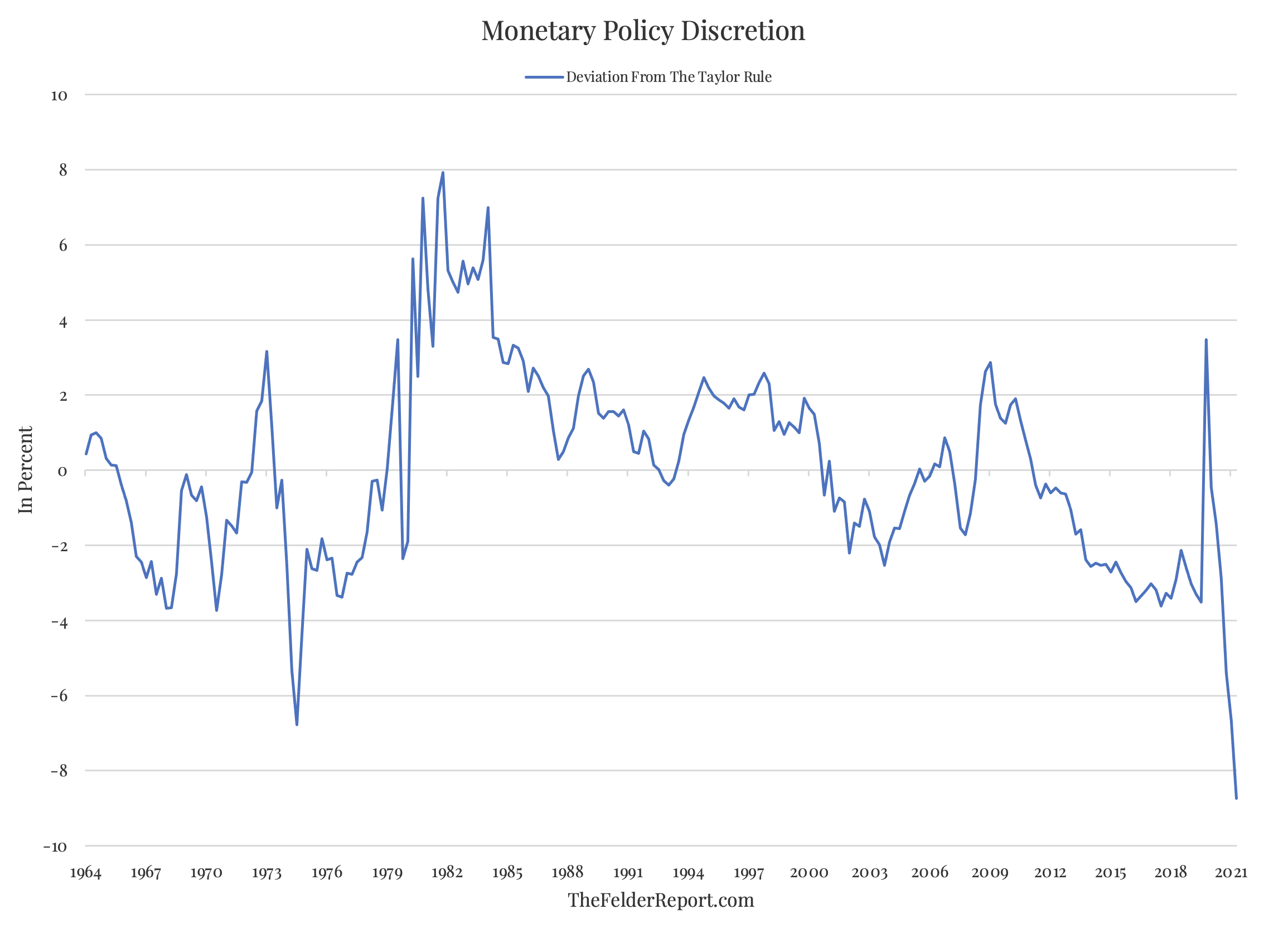

One way to view these valuation extremes is to simply see what extraordinary monetary accommodation has wrought. That near doubling of the Fed’s balance sheet on the right hand side of the chart below is largely responsible for the surge off the chart in the first two charts above. Print trillions of dollars in order to purchase financial assets in the open market and it’s not surprising to see all boats rise as a result. But notice the more recent direction of the red line in the chart below.

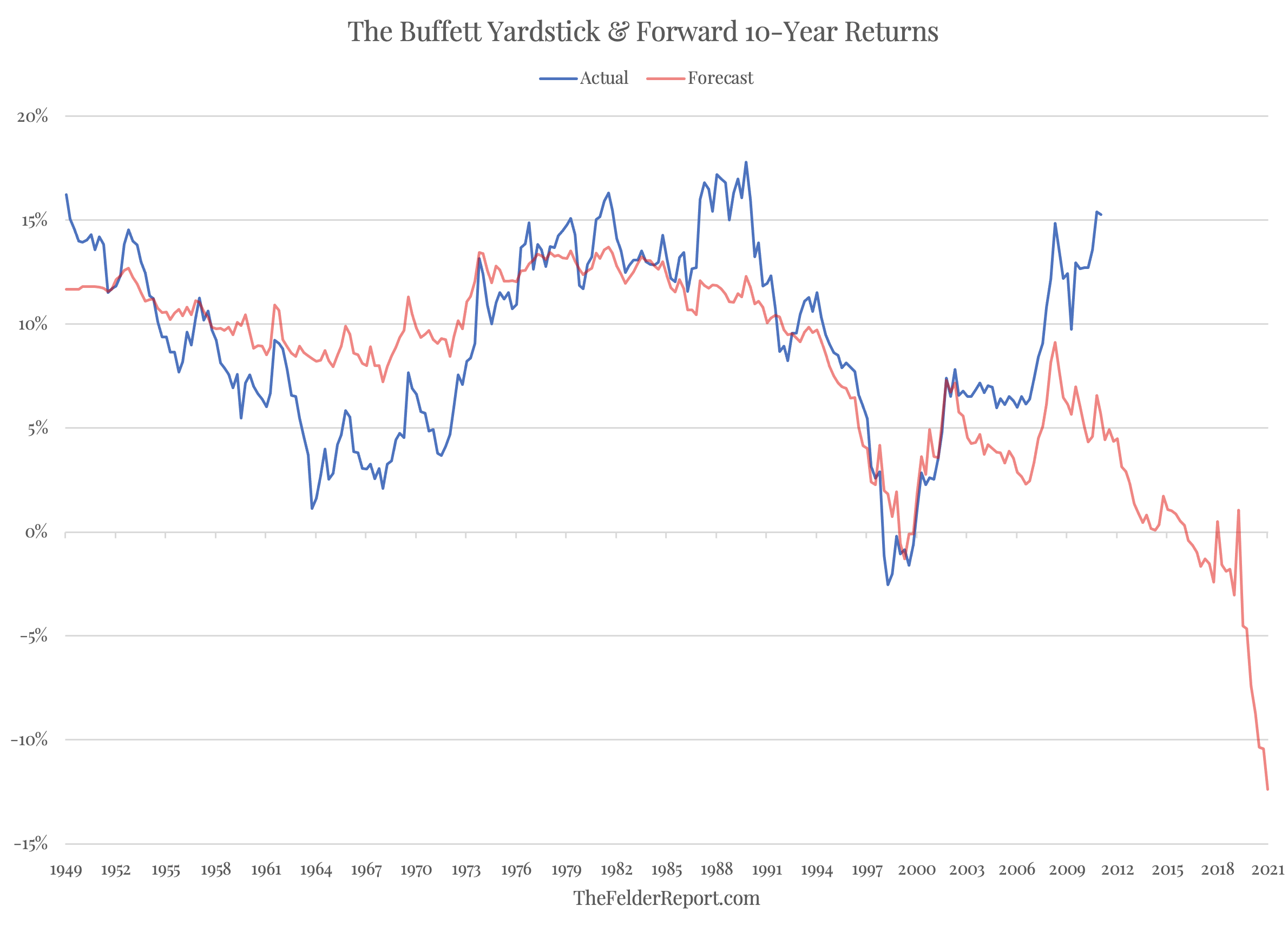

The Fed is now in the process of removing all of that accommodation responsible for the risk taking that saw valuations break records. As to those valuations, stock prices would need to fall 40% today merely to return to the Dotcom Mania peak of just over 20 years ago. What’s more, the strong negative correlation between this measure and forward 10-year returns in the S&P 500 Index suggests that the average annual return investors should expect over the coming decade is deeply negative (even before inflation is factored in). Of course, these sorts of negative returns typically come in bunches rather than some sort of steady erosion.

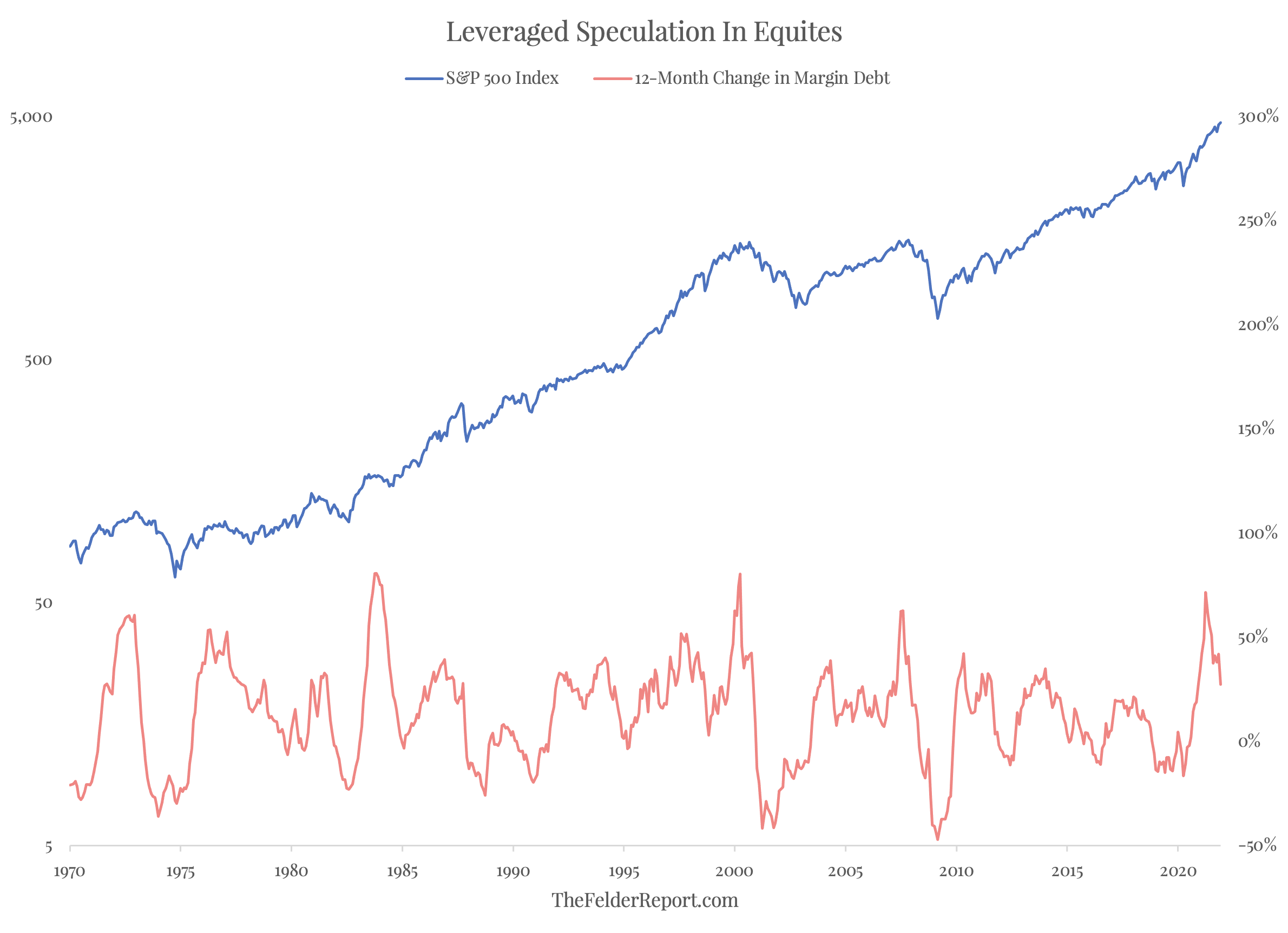

And margin debt is already following in the footsteps of waning Fed liquidity. Nearly every time margin debt has surged by more than 50% year-over-year and then reversed back below that level, as it has just done, it has coincided with a major peak in the stock market. The 1973-74 bear market was the first example in the chart below, followed by the 2000 stock market peak and the 2007 peak after that. Considering this most recent surge in margin debt comes off of the largest base, by far (even in relative terms), in history, it should be that much more significant.

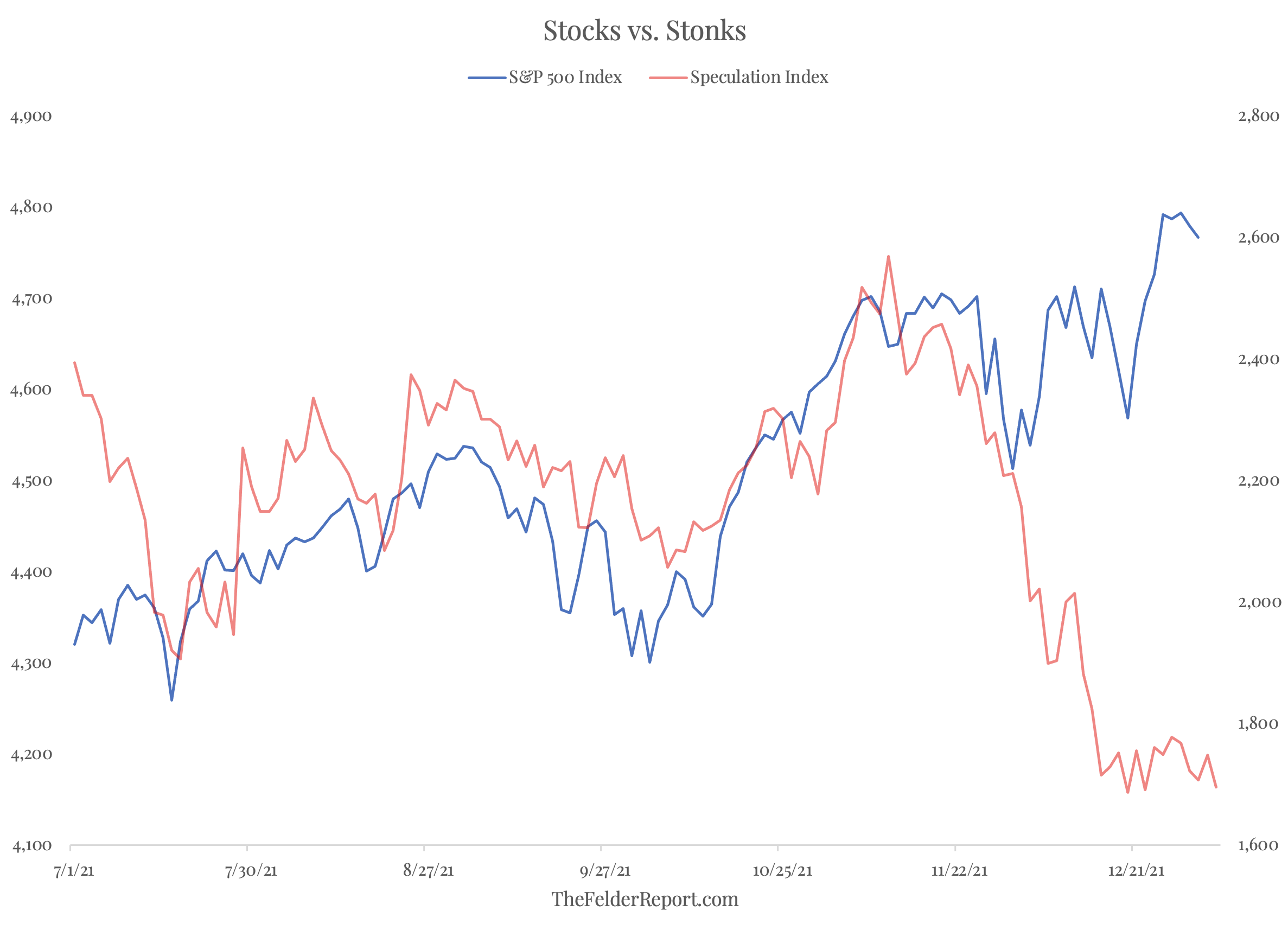

In addition to margin debt figures, the most speculative names within the stock market are already feeling the heat of waning liquidity. Our Stonks Index, comprised of the most popular meme stocks over the past couple of years, shows a rapid decline over the past six weeks or so. Taken together, these indicators suggest we are possibly witnessing a dramatic shift in risk appetites that could affect stocks more broadly in coming months. As these indicators imply, risk appetites have now become heavily dependent upon massive monetary accommodation. And the shift from extremely dovish to a bit less dovish is already creating ripple effects.

All told, it looks like a very dangerous time to be an investor in the broad indexes. Equities are extremely overvalued and the unprecedented monetary accommodation that made possible the sort of risk taking which enabled these valuations is now being removed. At the same time, inflation has risen dramatically, representing a potential catalyst for both falling valuations and increased monetary tightening. As to that latter point, the Fed has never been further behind the curve than it is today. In this context, it’s hard to call the central bank hawkish at present; it’s really only just begun to back off of the most dovish policy in history.

All told, it looks like a very dangerous time to be an investor in the broad indexes. Equities are extremely overvalued and the unprecedented monetary accommodation that made possible the sort of risk taking which enabled these valuations is now being removed. At the same time, inflation has risen dramatically, representing a potential catalyst for both falling valuations and increased monetary tightening. As to that latter point, the Fed has never been further behind the curve than it is today. In this context, it’s hard to call the central bank hawkish at present; it’s really only just begun to back off of the most dovish policy in history.

In order to play catch up, monetary policy will have to begin to normalize. Equity valuations will likely begin to normalize, too, as a result. But because the Fed cannot afford to crash the stock market in this process, it is unlikely monetary policy will be normalized enough to actually bring inflation under control. For this reason, monetary policy will likely remain relatively dovish, and thus inflation elevated, for a very long time. Ironically, in the midst of this situation, the best inflation protection known to investors is on sale today. Commodities, even after the splendid run they have had recently, have rarely been as cheap relative to equities as they are right now.

Furthermore, many commodities-focused companies look cheap relative to their underlying commodities. The oil price has rallied in a massive way since its 2020 lows but the relative performance of energy stocks doesn’t yet show it (even though they were the top-performing sector in the stock market last year). At the very least this suggests the bull market in energy is far closer to its beginning than its end. There’s a good chance the oil price continues higher this year (due to bullish supply and demand dynamics); eventually, energy stocks will need to reflect it.

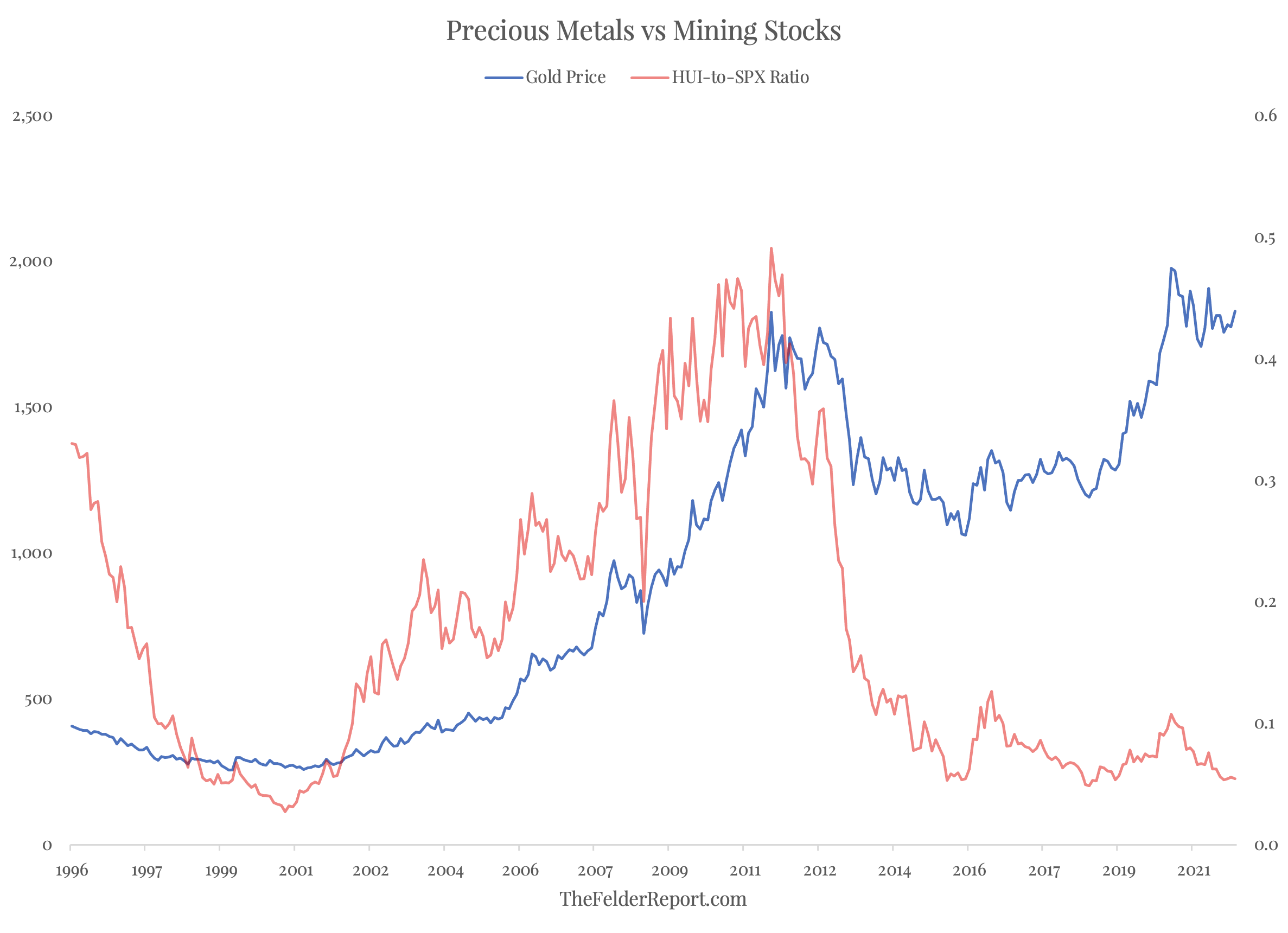

Even more dramatic is the relative performance of gold mining stocks. The gold price over the past five years has ripped to new, all-time highs but you would never know it from the looks of the gold mining stocks. They have acted as if gold was languishing at $1,000 an ounce rather than nearly double that level. If the gold price, after its long consolidation, resumes its bull market trend this year, mining stocks will likely be the best way to play it.

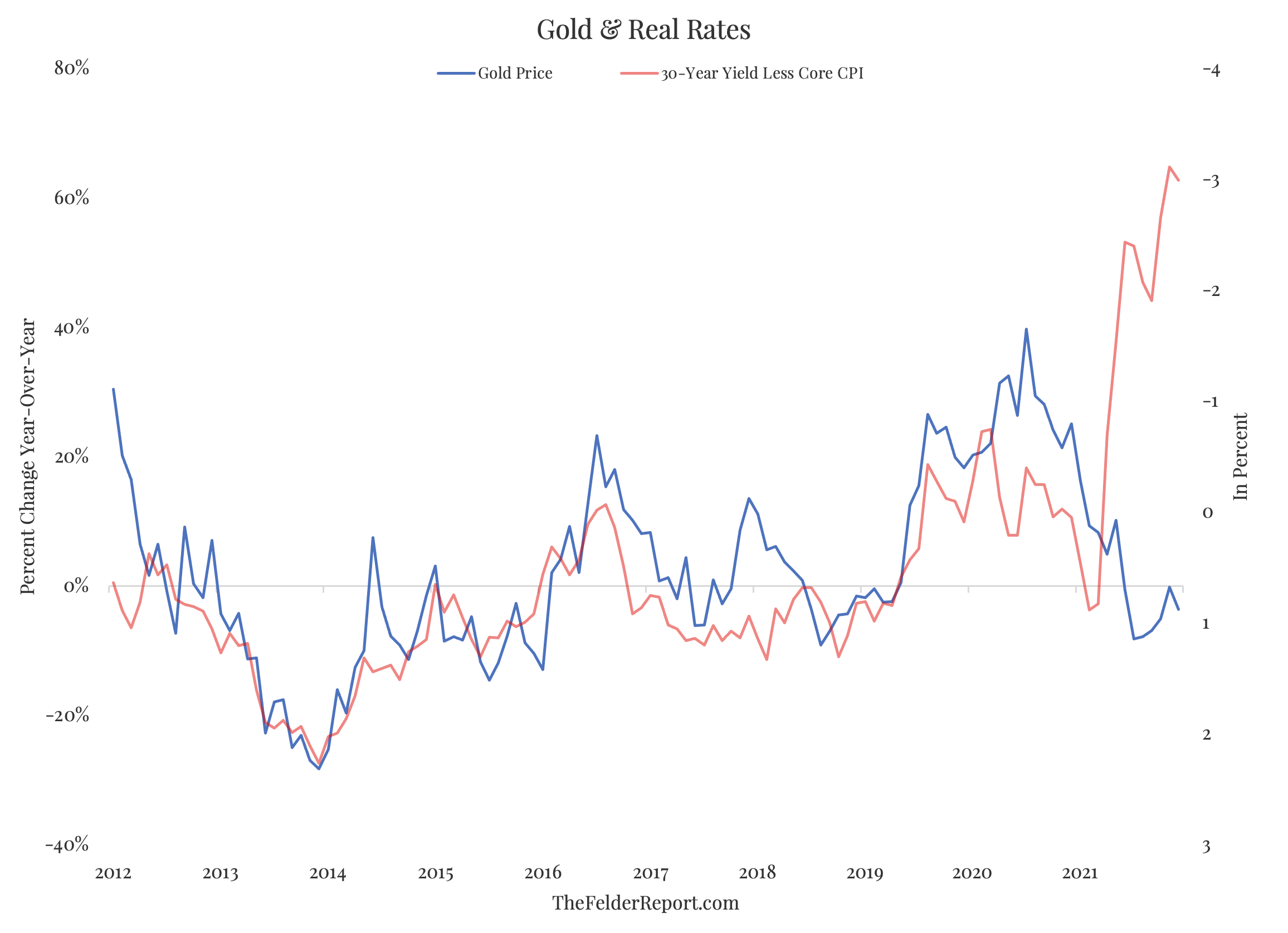

Fundamentally, the gold price remains deeply undervalued relative to real interest rates. This only makes sense if the Fed will, indeed, make good on its “stable prices” mandate, come hell (stock market crash) or high water (recession). To whatever extent the Fed delivers a dovish surprise relative to its “forward guidance” in regards to tightening monetary policy in addressing inflation, the gold price will soar.

Technically, that is exactly what the long-term chart suggests may lie ahead for the gold price. After peaking back in 2011, gold prices underwent a bear market that lasted several years. They bottomed in 2015 and broke out to new highs in 2020. Since that time, the gold price has fallen back to test the breakout level, a classic bullish setup. A breakout above the short-term downtrend line that dates back to the summer of 2020 would be very bullish as it would signify the continuation of the bull market that began in 2016.

Considering just how fraught the current equity environment appears, it makes sense to, at the very least, approach markets with a broadly diversified strategy as outlined by our Bulletproof Portfolio. For more intrepid investors, a tactical approach that limits exposure to market-cap weighted equity indexes while taking advantage of attractive opportunities in commodities-focused equities, as outlined by our Tactical ETF Portfolio, might be suitable. Either way, 2022 may be poised to test traditional passive investors in ways they haven’t ever been tested before.