Authored by Mike Shedlock via MishTalk,

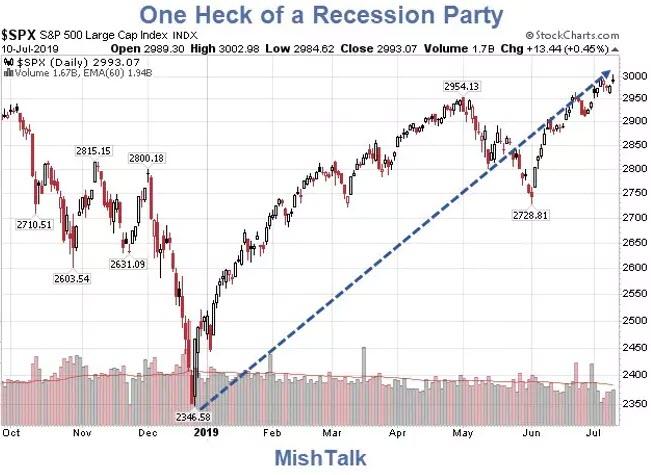

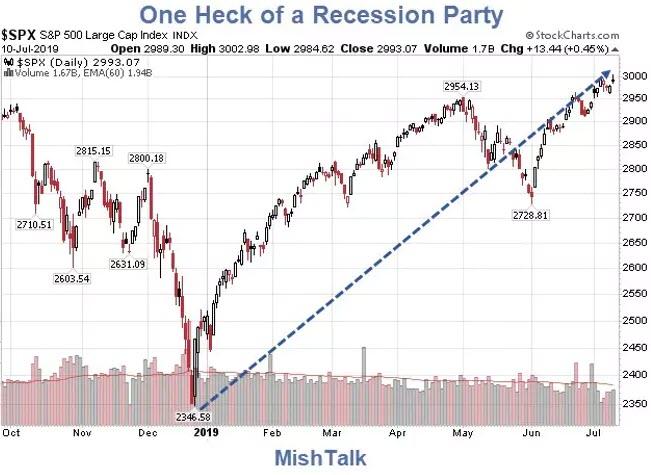

Stocks are on a tear. Celebrating rate cuts. With the rate cuts comes a recession. No recession? No more rate cuts.

It’s been one hell of a party.

Hold on, John Hussman says Warning: Federal Reserve Easing Ahead

Of all the distinctions that investors might make in the coming few years, one that I expect will serve investors particularly well is the distinction between how the market responds to monetary policy when investors are inclined toward speculation, versus how the market responds when investors are inclined toward risk-aversion.

Be very careful not to assume that ‘easy money’ means ‘rising market.’ Easy money amplifies speculation, provided that investors are already inclined to speculate. But if investors are inclined toward risk-aversion, safe, low-interest rate liquidity isn’t an ‘inferior’ asset at all; it’s a preferred one. As a result, creating more of the stuff simply doesn’t promote speculation.

The fact is that with the exception of 1967 and 1996, every initial easing of monetary policy by the Federal Reserve has been associated with an oncoming or ongoing recession.

Investors should recognize that there is a certain amount of information content in those initial rate cuts. Specifically, when the Federal Reserve shifts from tightening (or normalizing) monetary policy and instead begins a fresh round of rate cuts, it’s a clear indication that something in the economy has gone wrong.

The misplaced exuberance of investors is something my friend Danielle DiMartino Booth calls a “Recession Party.” We doubt this party will end well. Blind faith that rate cuts are always positive for the stock market is a mistake. This assumption is likely to be the hook that keeps investors holding on through a 60-65% market collapse over the completion of this market cycle.

Chuck Prince Still Dancing – July 10, 2007

Chuck Prince, then CEO of Citygroup, said there was no end to the buyout boom:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing”.

Question of Solvency – November 1, 2007

On November 1, 2007 I wrote Question of Solvency at Citigroup.

Richard Bove, an analyst with Punk Ziegel & Co., doesn’t dispute that Citigroup has issues, but solvency is not one of them, he said.

“These numbers indicate that this bank is both liquid and well-capitalized,” Bove wrote. “At the end of the third quarter, Citigroup posted $2.355 trillion in assets. This was more than any other American bank and possibly more than any bank in the world.”

Notice how Bove cleverly pointed out the asset side of the equation while conveniently forgetting about liabilities. Let’s rework Bove’s statement to see the other side of the story.

“At the end of the third quarter, Citigroup posted $2.227 trillion in liabilities. This was more than any other American bank and possibly more than any bank in the world. A mere 5.4% decline in the value of Citigroup’s assets would make Citigroup insolvent.”

Citigroup’s assets look great in a vacuum. However, those assets do not look so great in relation to liabilities. Leverage has never been greater, and much of that leverage is now in exactly the wrong places: residential and commercial real estate.

Citigroup CEO Chuck Prince’s next “dance step” is likely to be out the door.

Prophetic Words

Looking back, I am rather proud of that last sentence.

I don’t even remember writing it.

But it came up the very next day.

Next Dance Step – November 2, 2007

On November 2, 2007, I penned Music Stops for Chuck Prince

The party is over and the music has stopped for Chuck Prince. His last dance is a two-step out the door. Citi’s Prince Plans to Resign

Prince’s retirement solves nothing actually. And of all the issues at Citigroup, capital levels is the most critical one. With capital concerns come side issues such as a Question of Solvency at Citigroup.

Let’s play American Pie in honor of Chuck Prince.

We all got up to dance,

Oh, but we never got the chance!

`cause the players tried to take the field;

The marching band refused to yield.

Do you recall what was revealed

The day the music died?

Party On

I ended my November 1, 2007 Question of Solvency article with this thought:

“Solvency is the issue here, and I am not just talking about Citigroup. I am talking about solvency of the system itself. Rate cuts fueled this mess. Rates cuts cannot be the answer.”

The music is still playing. Party on dudes.

Still like those negative-yielding junk bonds?