The Federal Reserve is a natural born spread killer!

(Bloomberg) — The tsunami of money and credit pouring into financial markets has washed away much of the available spread for mortgage bond investors.

The Bloomberg Barclays U.S. MBS index option-adjusted spread fell to just 0.07% last Wednesday — lowest in at least a decade. The Fannie Mae 30-year current coupon spread over a blend of the 5- and 10-year Treasury yields closed last week at 0.66%, tighter than all but 13 days over the last ten years, with six of those 13 days coming earlier this year.

The paucity of spread is a fact discussed throughout financial markets in our age of quantitative easing; it is not a phenomenon unique to agency mortgage bonds. Which leads to a greater question: has the Fed injected enough credit into the markets? We already know their answer to that question — it’s a resounding “no.”

The U.S. money supply has exploded during this latest round of QE, leaping 25% higher in 2020, fastest since at least the end of the 1950s. From 1960 until 2019 the average year-over-year growth was 6.8%. The latest release for February saw a 27.1% leap compared to the previous year. All that credit needs to go somewhere, and securities markets are deep and liquid.

So mortgage bond investors may at least console themselves with the thought that it’s difficult for spreads to widen when both the Fed and U.S. banks are putting such a bid under the market. The Fed’s gross mortgage bond purchases during this latest round of quantitative easing are rapidly approaching $2 trillion.

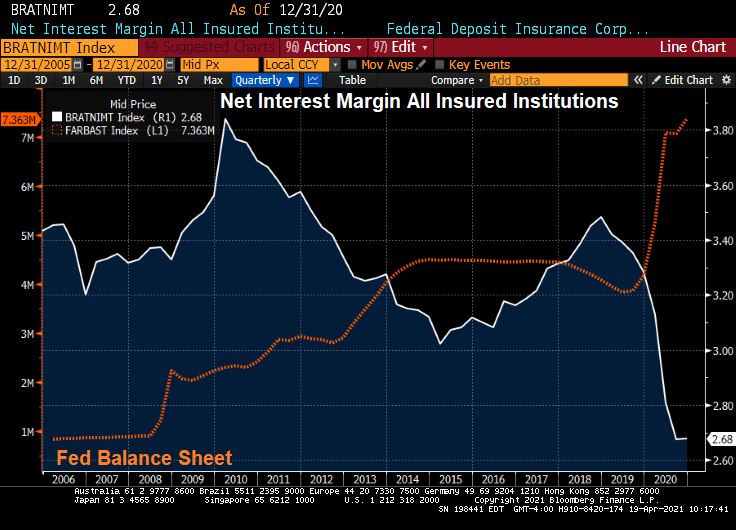

The banks have added $145 billion to their agency mortgage bond holdings this year alone, as the Fed’s QE security purchases increase their reserves. And with those U.S. commercial banks’ reserves about 21% higher since the latest round of QE began, and with loan growth tepid, they will likely continue investing in mortgages in order to bulked up their net interest margins.

Mortgage bonds last week — the UMBS 30-year stack in particular — outperformed their Treasury hedges, though without any clear pattern. Despite the 2- and 10-year Treasury curve flattening by nine basis points during the week in aggregate, the 3.5% coupon was best in show at 10 ticks, followed by the 2.5% at seven.

The highlight of this week’s economic data will be existing home sales on Thursday followed by new home sales on Friday. The former declined to a six-month low in its last report, with a lack of inventory fingered as the culprit.

MBS Option Adjusted Spread? It has gotten crushed by The Fed’s ludicrous speed of money printing.

Fed Chair Jerome “Dark Helmet” Powell says “Prepare for Ludicrous Speed!”