by GoldCore

The Brexit deadline of December 31st, the date beyond which the transition or implementation period cannot be extended, now looms large and the dreaded “No-Deal” Brexit outcome looks increasingly possible by the day.

There is plenty of brinkmanship, rhetoric and passionately held views on the Brexit issue and recent days have seen this again. It is and will continue to be a highly partisan and divisive issue.

It is important to tune out the political noise and realise that whether you are pro-Brexit or anti-Brexit, it will impact most British people’s finances and wealth in a negative way, particularly those who are complacent and unprepared.

The draconian response to the COVID-19 coronavirus and the now second UK lockdown is set to badly impact the UK economy and indeed the global economy. An even greater toll is being placed on already badly impacted and struggling consumers and companies.

The timing of Brexit could not be worse given the state of the world macroeconomically, geopolitically and monetarily. An already vulnerable global economy is in turmoil due to the COVID-19 virus and the economic lockdowns of most nations.

Throw the Brexit financial and very significant economic uncertainty into the mix and you have a very lethal cocktail indeed.

The Likelihood of a ‘No Deal,’ ‘Hard Brexit’ Has Increased

Even at this “eleventh hour” as the clock approaches midnight, the UK and EU continue to be at loggerheads over a post Brexit trade deal to replace a transitional agreement that expires at the end of the year on December 31st. Negotiators for both sides continue to warn that there are very wide divergences between the UK and the EU positions in the ongoing negotiations.

There are ongoing fresh bids to break the current Brexit deadlock at the highest level by the EU’s European Commission’s Head of Task Force for Relations with the UK, Michael Barnier and the UK’s Chief Negotiator of Task Force Europe, Lord David Frost. UK Prime Minister, Boris Johnson says a deal is there to be agreed between the UK and the EU but at the same time Johnson and his team have warned the EU there are only days left for a deal to be reached.

This has sparked renewed concern in the EU, whose senior negotiators say they need a longer period to finalise details. Michael Barnier has warned that he sees deepening divergences with the UK. Barnier signaled all was not well in a tweet on November 4th:

“Despite EU efforts to find solutions, very serious divergences remain in Level Playing Field, Governance & Fisheries. These are essential conditions for any economic partnership. [The EU] is prepared for all scenarios.”

Sir David Frost replied on Twitter very soon thereafter:

“We’ve just finished two weeks of intensive talks with the EU. Progress made, but I agree with Michael Barnier that wide divergences remain on some core issues. We continue to work to find solutions that fully respect UK sovereignty.”

Boris Johnson’s defeat in the House of Lords over his plans to breach international law on Brexit further complicate matters and may weaken his team’s position. The bill is set to return to the House of Commons in December, when MPs are likely to reinsert the offending clauses.

The plans would have allowed the UK government to ignore the Northern Ireland Protocol, handing UK ministers sole power to determine customs regulations on a unilateral basis and to determine when U.K. state aid rules might undercut EU companies, rather than having this decided by joint EU and UK committees.

The election of Joe Biden as American President is another complicating factor as Biden is known to be pro-European Union and in favour of the Good Friday Agreement and the Irish government’s position on Brexit due to his Irish ancestry. Johnson and his negotiators’ brinkmanship on the Irish border issue in the Brexit negotiations will likely not sit well with the president-elect.

Hopefully, the ongoing negotiations and somewhat trenchant positions being adopted are the typical brinkmanship of a very tough negotiation but it is possible that the UK and EU negotiators fail to find compromise solutions on the red line issues.

Hence the importance of taking steps to protect you, your families and your business’ finances.

How a ‘No-Deal’ Brexit Would Likely Negatively Impact the UK

A UK government 5 page “worst case planning” document (Operation Yellowhammer – the government’s no-deal contingency plan) outlines “reasonable worst case assumptions” in the event of a no-deal Brexit and warns of a lack of supply of certain consumer goods and food items, increasing inflation in the form of rising food prices and rising energy and fuel prices, disruption to medicine supplies and public disorder.

Besides negative impacts on consumers and citizens, there are also likely to be negative impacts on entire large economic sectors which employ thousands of people and generate significant tax revenue in the UK.

There are many employment creating industries that are exposed to a no-deal Brexit and just one of many examples of sectors very exposed to Brexit is the UK automotive industry. An illustration of how vulnerable is the fact that UK car manufacturers have spent more than £730 million on preparations for Brexit according to the industry’s trade body.

In excess of £235 million has been spent in just 2020 alone, the Society of Motor Manufacturers & Traders (SMMT) said November 10th. It published figures as it issued what it called a ‘last-chance plea’ for a zero-tariff, zero-quota trade deal between the UK and the EU.

The SMMT said their sector is doing ‘everything in its control’ to prepare for the end of the Brexit transition period on December 31. However, it warned that efforts are being greatly hampered by a lack of clarity on future trading arrangements between the UK and the EU economic bloc.

A no-deal scenario or failure to achieve a ‘workable deal’ for the automotive industry would result in the loss of thousands of jobs and see a £47 billion hit over the next five years, they warned.

The lack of clarity is badly impacting most sectors and most companies in the UK – from small and medium enterprises to giant corporations, not to mention that all important ingredient of economic confidence.

Global Uncertainty with Very Significant Macro, Monetary, Geopolitical and Systemic Risks to Support the Price of Gold in Dollars and Pounds

The global economic, geopolitical and monetary risks that confront America and indeed the world today are as great as any seen in living memory. The all-important wider global context means that most gold analysts are positive on gold’s outlook in the medium and the long term with calls for gold to rise to over $3,000 per ounce.

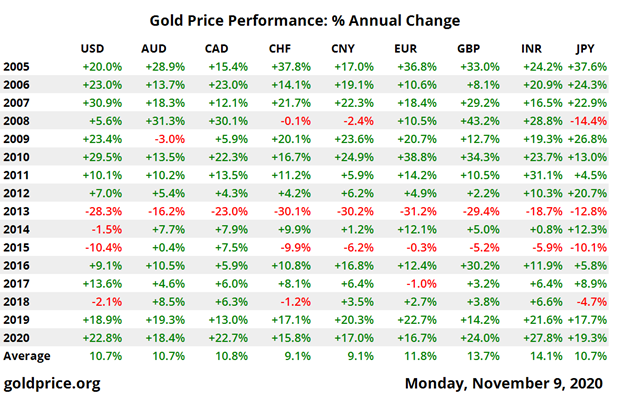

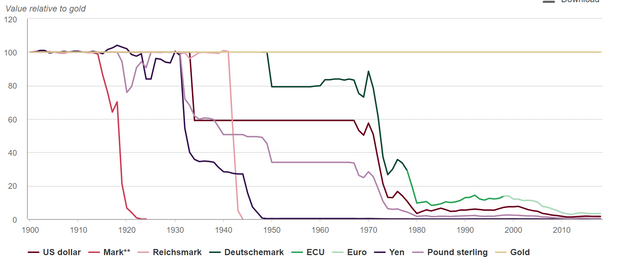

It also informs our view that gold will continue its bull market for some time as currencies continue to depreciate as they have done throughout history. All currencies, including British pounds, have lost between 97% to 100% in the last 120 years (see chart below).

British gold buyers resident in the UK ordinarily buy gold coins or gold bars in sterling and should consider their allocation to gold in terms of their exposure to sterling due to their house, property investments, savings, pensions and business, many of which are exposed to sterling.

The price of gold in GBP terms is determined by two factors: the price of gold in USD and the GBP/USD exchange rate which inform the gold price in British pounds. Currencies including the USD and GBP are akin to the shares of a country. If the country does well economically then the share or currency tends to appreciate and if the country does poor economically then the currency tends to depreciate.

It is nigh impossible to predict the outlook for the GBP/USD exchange rate but we can say with some confidence that it is very likely that both currencies will weaken against gold. We have looked at the poor fundamentals of the U.S. fiscal position for many years and below we delve deeper into the poor fundamentals of the UK economy.

The bottom line is that all currencies are likely to be devalued versus gold in competitive currency devaluations or indeed in a central bank orchestrated “currency reset” that will likely coincide with an economic and political “great reset” as being pushed for by the World Economic Forum, mega corporations and the billionaire elites of Davos.

The current risks posed to both the UK and the U.S. economies and indeed the global economy mean that the gold market is set-up for a perfect storm whereby the price of gold in dollar terms increases, while simultaneously sterling weakens sending gold in sterling terms much higher.

Why Sterling Looks Set to Weaken Further Against Gold

Brexit will impact the UK and EU economies badly and a ‘Hard Brexit’ would be even more damaging. The UK looks very vulnerable economically given the poor and deteriorating fiscal and economic position.

The UK national debt or total government debt has been surging higher for many years now but has surged even more during the COVID-19 outbreak and lockdowns. The ostensible or nominal UK national debt has surged another 33% in recent months – from £1.8 trillion at the start of the year to £2.42 trillion today.

The reality is even worse than this as all public sector liabilities including state and public sector pensions are not included when accounting for the national debt number. The real national debt including massive pension liabilities is closer to £5 trillion (as we explained in this video) or in clearer digit form £5,000,000,000,000 (or 5 with twelve zeros as there are twelve zeros in a trillion).

This works out at over £75,000 per person and per every single man, woman and child that constitute the UK population of 66.5 million people. There are 25 million households in the UK and this £5,000,000,000,000 constitutes £200,000 per household and this is on top of massive private debt in terms of all other forms of debt including credit card loans, student loans, car loans and mortgages to name just a few of the many debt burdens.

While all the focus is on Brexit, the UK faces a debt and currency crisis. It has over $8.5 trillion in external debt and total debt including government, private, business & bank debt as a percentage of GDP is over 500%. The increasingly disunited kingdom is the 2nd largest debtor in the world ever – coming only second to the world’s largest debtor ever – the U.S.

Thus, the pound is almost certain to weaken even further versus gold in the coming months and years and the 13.7% average return seen in the last 15 years (see table above) is almost certain to be equaled or surpassed in the next 10 to 15 years. Indeed, the very strong performance of gold seen in recent years is likely to be seen in the coming years.

Gold was trading at below £200 per ounce when Gordon Brown imprudently sold the UK gold reserves at the very bottom (Brown’s bottom!) of the market in 1999. Today gold trades at £1,400 per ounce. So, the pound has fallen some £1,200 pounds against gold or 85% in 20 years.

The Bank of England’s lack of gold reserves today when compared to the U.S. Federal Reserve’s putative 8,100 metric tonnes and the Eurozone’s combined nearly 10,000 metric tonnes (although the exact number is great disputed due to the reserves not being officially audited for many years), makes sterling even more vulnerable than the dollar and the euro. Even China and Russia have being greatly increasing their gold reserves for many years and this will support the Chinese Yuan and Russian Ruble.

Sterling and by extension and for the same reasons, UK government bonds or “gilts” also look very vulnerable as do certain still “elevated” property markets in the UK. This includes still frothy and unaffordable London which the Johnson government is desperately trying to keep inflated with government largesse including more tax breaks and inducements such as making banks offer reckless 95% mortgages.

Markets are normally quite good at pricing in significant economic risks. However, this does not appear to be the case today with UK gilts and many property markets remaining at or near record highs. UK gilts are near record highs in terms of price and record lows in terms of yields with the 10 year yielding just 0.3% despite significant fiscal, macro and monetary risks.

UK property markets and especially the London property market remain at elevated levels. Although both are obviously being supported by the massive quantitative easing (QE) which Mark Carney’s Bank of England is recklessly engaged in.

The Bank of England has boosted its quantitative easing (QE) “stimulus” package by another £150 billion, as central bankers use the coronavirus and attendant lockdowns to justify even greater currency creation in order to buy vulnerable government bonds and other assets.

The Bank warned that the surge in COVID-19 cases and the second lockdown means the UK economy will shrink in the current quarter. That means Britain would suffer a double-dip downturn this year.

QE was always positioned as a short-term emergency measure. We warned when it launched in November 2008 that there was a real risk that they would become a near permanent monetary injection in order to support fragile indebted banks, the massively over extended government debt markets and suppress interest rates to protect a hugely over indebted UK economy. And so it has come to pass.

There are no free markets anymore as markets are completely dependent on and hopelessly addicted to central bank monetary injections of trillions and trillions of pounds, euros, dollars, yen, yuan and other fiat currencies. Were they to withdraw them, the giant debt based Ponzi economy they have created since 1971, when Nixon went off the Gold Standard, would collapse.

“QE to infinity” as we and others dubbed it does not appear reckless now as much of the media completely fails to analyse the very real monetary risks and continues to cheerlead our central banks “saviours” and currency debasement on a scale never before seen in human history.

However in time, it will be realised that our monetary overlords have been and are engaged in a reckless QE and ‘currency reset’ experiment. Ultimately it will lead to massive currency devaluations and potentially the collapse of many currencies as with the German Mark in Weimar Germany or the Argentinian Peso in recent years. Prior to that we may see a coordinated global devaluation and a “currency reset” which devalues all currencies versus gold and pegs new electronic crypto fiat currencies to gold at a fixed price – say for example £10,000, €10,000 and $10,000.

Conclusion – Fail to Prepare Financially, Prepare to Fail Financially

It might seem odd to quote an Irish man who lived from 1856 to 1950 to conclude an article about Brexit and its likely impact on the financial wellbeing of British people but it seems quite appropriate.

Whether you are a Remainer or a Leaver, whether you voted to leave or to stay in the EU, or neither, the words of writer, playwright and political activist, George Bernard Shaw, are as apt today as they were when he said them:

“You have to choose between trusting to the natural stability of gold and the natural stability of the honesty and intelligence of the members of the government. And, with due respect to these gentlemen, I advise you, as long as the capitalist system lasts, to vote for gold.”

NEWS and COMMENTARY

Bidenomics: More stimulus, tougher regulation, and gridlock

Gold gains more than 1% as focus returns to loose monetary policy

Dollar dips on vaccine doubts

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

10-Nov-20 1874.90 1878.70 1416.49 1417.48 1589.54 1590.13

09-Nov-20 1957.45 1867.30 1489.23 1417.47 1648.76 1573.95

06-Nov-20 1947.95 1940.80 1483.17 1480.05 1642.71 1636.29

05-Nov-20 1916.80 1938.45 1468.84 1480.78 1624.68 1638.38

04-Nov-20 1888.55 1900.15 1455.69 1462.17 1616.41 1621.97

03-Nov-20 1899.85 1908.30 1462.31 1464.05 1624.37 1628.73

02-Nov-20 1886.75 1889.90 1460.34 1463.16 1620.72 1624.50

30-Oct-20 1875.80 1881.85 1448.12 1453.92 1607.19 1611.24

29-Oct-20 1876.85 1870.30 1444.24 1447.05 1600.58 1601.16

28-Oct-20 1896.85 1869.95 1461.71 1439.30 1614.22 1593.38

Buy gold coins and bars and store them in the safest vaults in Zurich, Switzerland with GoldCore.

Learn why Switzerland remains a safe-haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here