By Wolf Richter for WOLF STREET.

Spooked by the Fed’s shock-and-awe surprise 50-basis-point rate cut, the already frazzled markets did a job today. Gold surged nearly 3%. The three major stock indices all swooned nearly 3%. And Treasury yields plunged across the board.

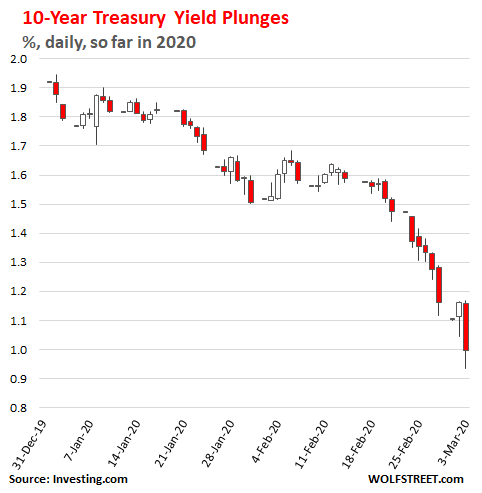

The 10-year Treasury yield plunged from 1.13% pre-announcement to an intraday low of 0.935%, and closed officially at 1.02%. When the yield drops, it means that bond prices rise. In late trading the yield fell below 1% again, and is currently at 0.997% reflected in the chart (data via Investing.com):

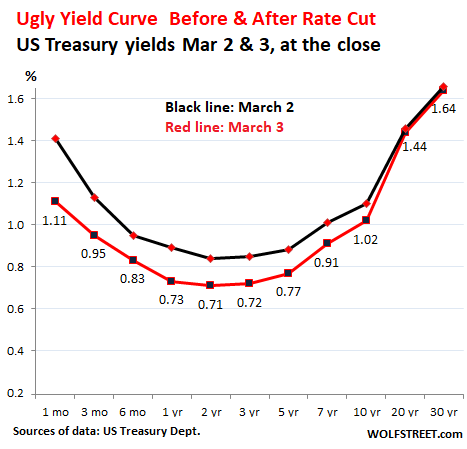

The one-month yield – in a sign that this was a surprise act – plunged 34 basis points, most of it instantly, from 1.45% just before the shock-and-awe rate-cut announcement to 1.11% at the close, which put it in the middle of the Fed’s new federal-funds target range between 1.0% and 1.25%.

The three-month Treasury yield plunged from 1.20% just before the announcement to 0.95%, already pricing in another rate cut well before its maturity in 90 days.

The two-year yield plunged to 0.72%, the lowest point on today’s yield curve. The 30-year yield ticked down 2 basis points to 1.64%, a record low.

The chart below shows the increasingly ugly yield curve yesterday at the close (black line) and today at the close (red line), for each maturity, from the one-month yield on the left, to the 30-year yield on the right:

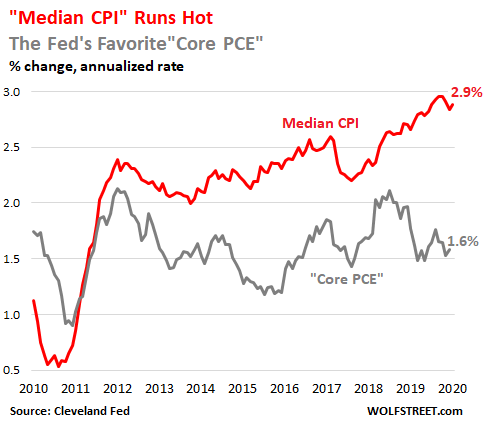

At this point, nearly the entire yield curve is below our most doctored and repressed US inflation gauge, the Fed’s preferred “core PCE,” which languishes at 1.6%. And the entire yield curve is far below the Cleveland Fed’s median CPI, which has surged to 2.9%.

The Median CPI is based on the data from the Consumer Price Index (CPI) but removes the extremes of price increases and price decreases, that are often temporary, to reveal underlying inflation trends:

Generally speaking, plunging Treasury yields, while inflation is rising, are not a sign of confidence, other than confidence in yields falling even further due to fears of more mayhem coming at the markets which would make the Fed react even more vigorously by cutting rates even further.

Investors who bought Treasuries before the rate cut and sold afterwards made a very quick buck, especially if it was a leveraged bet.

But lower yields are bad news for fixed-income investors of all kinds that have to replace maturing securities with new low-yielding securities. These fixed-income products amount to over $40 trillion in the US, including Treasury securities, bank savings products, investment-grade corporate bonds, municipal bonds, asset-backed securities, and the like.

Much of this stuff now yields below the rate of inflation as measured by median CPI, meaning that interest income doesn’t even compensate investors for the loss of purchasing power of their principal due to inflation. New buyers of these securities get their cash flows from interest payments confiscated by the Fed’s monetary policy.

So they can invest in the still immensely overpriced stock market, and count on meager and fragile dividend yields, or they can stand on the edge of a cliff and look down and see if they have enough of a death wish to buy Ford shares for their 8% dividend yield. Dividends can get cut any time, no sweat. And those fixed-income investors chasing yield among dividends have a good chance of losing a lot of principal a lot more quickly than the damage inflation might do.

By the stock market’s reaction today to the Fed’s shock-and-awe surprise 50-basis point rate cut – it should have caused stocks to soar, but caused them to plunge nearly 3% instead – it would seem that another such shock-and-awe event signals even more panic inside the Fed, and who knows how the stock market might react when it sees the Fed panicking.

There is historic precedent: Most recently, the Fed started cutting its policy rates in late 2007 and was slashing them wholesale in big panic-cuts in 2008, seeing whatever it saw. Then Lehman blew up, and by then, all heck had broken lose in the stock market.