Unscrupulous stockbrokers and advisers are always dangling yield in front of unsuspecting clients. “I can get you (fill in the blank with a percentage),” they say to yield-starved investors. But capturing current yield is one thing; buying shares of a firm that can sustain a dividend beyond the next quarter or two is something else.

I ran a screen on REITs using two factors – enterprise value/EBIT of 25 or less and a dividend yield of 6% or higher. I got 12 companies back. And EV/EBIT of 25 is quite high, which tells you something about how REITs are priced right now. Also, the screen was just the beginning of the process. The fun part is examining each company to see if dividends were sustainable and if it had any other warts such as a high debt load, a declining business, competition from Amazon, etc…

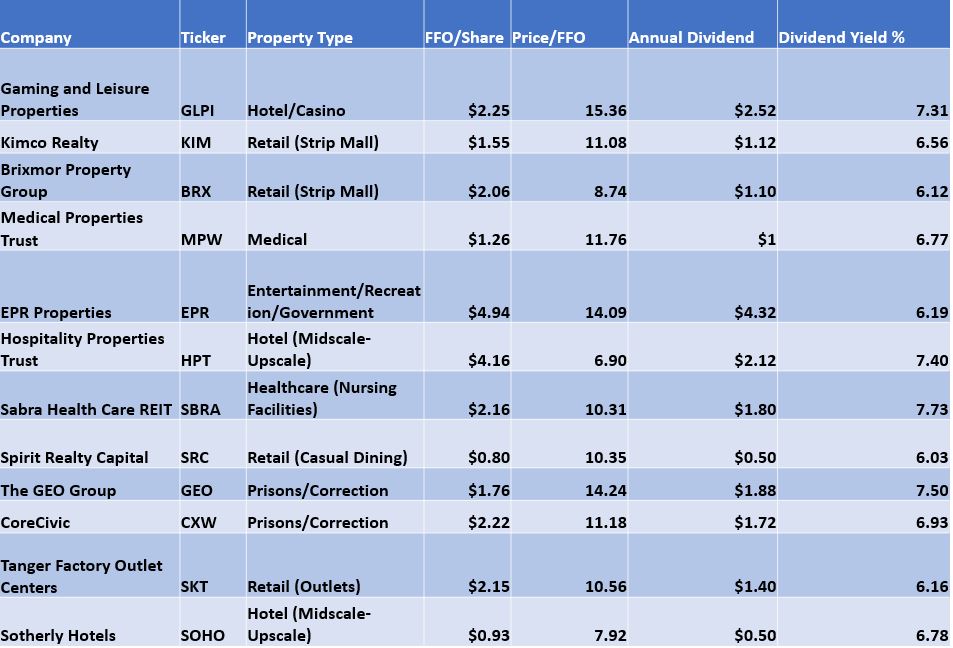

Here’s the list of the original screen followed by comments on some of the companies.

The Good

After compiling the names from the screen, I included FFO or Funds from Operations, a REIT cash flow metric, and calculated Price/FFO, a common, though imperfect, REIT valuation metric. Funds from operations or FFO is a measure of REIT cash flow calculated by adjusting net income for property sales and depreciation. A big depreciation charge runs through a REIT income statement, and it usually doesn’t correspond to economic reality. FFO isn’t perfect because some depreciation should be calculated for any property, but FFO is uniform and allows for some comparison between companies.

FFO is also useful for understanding dividend coverage. In every company on our list except for two (Gaming and Leisure Properties and The GEO Group) FFO covers the dividend. When FFO is less than the dividend it can be a sign of a dividend cut coming. Companies not covering the dividend with FFO have to hope for FFO-per-share growth or borrow to pay the dividend. Still, all the Price/FFO metrics were reasonable or downright cheap in some cases. None of the stocks on this list is outrageously expensive in my opinion.

Also, despite some tightness on dividend coverage, the companies on this list are surprisingly healthy in terms of their debt levels. None of them is in financial distress or unable to pay its interest and preferred dividends in my opinion.

The Bad And Ugly

Despite being financially stable and not inordinately expensive, the companies on this list don’t have what anyone would call outstanding, irreplaceable real estate. Buying shares in them arguably violates the old “location, location, location” rule of real estate investing with the exception of a few properties in the hotel portfolios. None of the companies own trophy office buildings in New York or San Francisco, Rodeo Drive retail space (which had some vacancies the last time I was there), or upscale apartments on the coasts where it’s hard to build. Instead the list is filled with strip mall retail space under attack from Amazon (KIMCO, Brixmor, and Tanger) hotel companies that are economically sensitive and always trade with lower valuation multiples than other property types (Hospitality Properties Trust and Sotherly), casinos under pressure from states allowing their proliferation (Gaming and Leisure Properties), medical facilities including nursing homes (Medical Properties Trust and Sabra), and prisons (The GEO Group and CoreCivic). In other words, these are cheap, high-yielding REITs because they arguably deserve to be based on the quality of their property.

Conclusion

Although these companies don’t own the best property, their stocks are reasonably priced, and in most cases their dividends are sustainable. Investors who understand that REITs are stocks, not bonds, in terms of risk and volatility can own a basket from this list as a small part of an income-generating portfolio. Nobody should bet the ranch on any of these stocks or on a basket of these stocks. Investors should also understand that monitoring that basket is required – not just in terms of how the stocks are performing, but also in terms of how the businesses are performing, including debt levels, occupancy, natural disasters potentially damaging the assets, management decisions, and many other things.

We at Clarity Financial LLC, a registered investment adviser, specialize in preserving and growing investor wealth. If you are concerned about your financial future, click here to ask me a question and find out more.

Disclosure: We are long SKT in some portfolios.