Inflation Is Shortages And Thankfully Transitory.

I’ve got inflation on my mind these days. Who doesn’t? The U.S. 10-year Treasury yield is up nearly 3-fold in the past year, stoked by fears of inflation. Commodities too are rocketing higher for similar reasons (in part). However, I am not convinced these trends will hold. To me, the deck looks stacked against inflation. Its misinterpretation may present trading opportunities.

The COVID-19 pandemic is causing tremendous human and economic hardship across the United States and around the world (emphasis added). Amid progress on vaccinations and strong policy support, indicators of economic activity and employment have strengthened. The sectors most adversely affected by the pandemic remain weak but have shown improvement (emphasis added). Inflation has risen, largely reflecting transitory factors.

It’s rare that I agree with Federal Reserve (Fed) officials. However, I fall firmly in the “transitory” camp when it comes to today’s inflation. It’s not that I think the Fed has been a good steward of the U.S. dollar’s value. Rather, it’s that inflation has little to do with monetary policy anymore. It’s the way in which we define inflation that makes me a secular deflationist. You see, I’m an optimist. I simply expect human ingenuity to prevail.

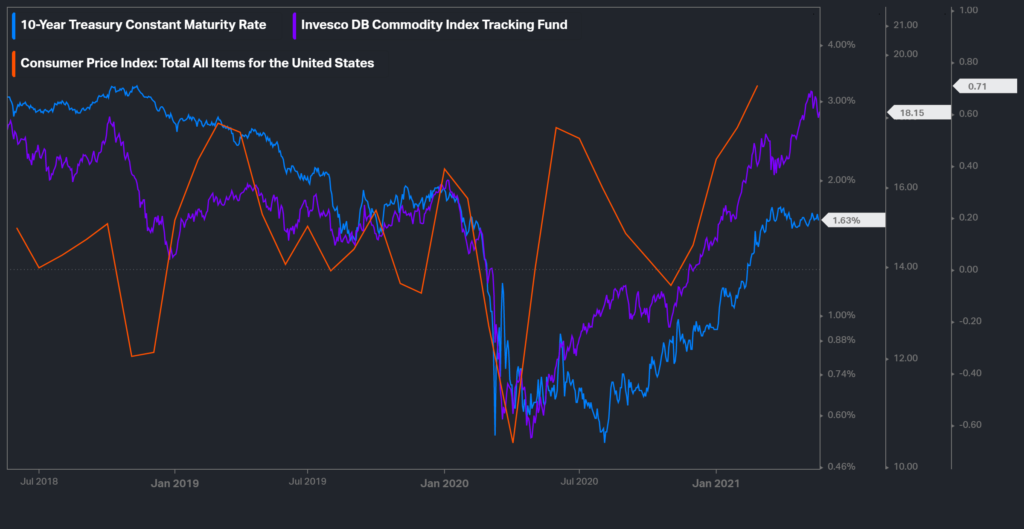

The U.S. 10-year treasury rate (blue) has nearly tripled from its all-time lows and commodities (purple) are rocketing higher as CPI (red) has increased.

Inflation’s meaning has stealthily changed

We take inflation’s meaning for granted today. It’s a foundational concept for valuing bonds that rolls off the tongues of laymen as easily as experts. There are volumes of books chronicling it, reams of academic literature analyzing it, and scores of metrics to measure it. Inflation is one of the most studied and commonplace financial concepts in the culture.

Yet, inflation is completely misunderstood today. Its definition has evolved over the years; however, many continue to hold onto its old one which no longer applies. Inflation once meant the debasement of a monetary standard of value. Today, it simply means “price increases.” These are very different definitions with equally distant implications.

A historical look at the origin and uses of the word inflation, arguing that although the term has become nearly synonymous with “price increase,” its original meaning—a rise in the general price level caused by an imbalance between the quantity of money and trade needs—is the definition driving many of those who advocate an anti-inflation policy for the Federal Reserve.

Michael F. Bryan, On the Origin and Evolution of the Word Inflation

All is not “on average”

Monetary debasement is a ubiquitous condition that applies to all goods, services, and actions. Nothing is spared since the standard unit of value itself is altered. It is also an instantaneous event occurring on the date of the (political) decree. Imagine doubling the definition of an inch one day. Everything would instantly measure smaller in these new inch terms no matter what you measured; all that was four inches would now measure two. This is inflation’s historical use.

“Price increases”, on the other hand, are completely different. Prices routinely fluctuate with commercial conditions—as supply and demand dynamically shift. They are an economic phenomenon unique to each good and service that garners a price. Some go up and some go down, but all do not move together, even if they appear to do so on average.

In other words, all is not the same as “on average.”

Money defines value and requires a standard

Recognize that inflation today means growth in the consumer price index (CPI). It bears no resemblance to its former definition of monetary (standard) debasement. Yet, we still treat inflation the same. While inappropriate, I nonetheless sympathize with the usage. Economies require an independently observable measure for money, just as they do for length and time.

Grasping money’s meaning is simple when its units are defined. Under a gold standard, for example, a dollar was equivalent to a fixed weight of gold. While it may seem arbitrary, it’s anything but. A fixed weight of gold requires a certain amount of effort to produce. It’s a value that anyone can wrap his/her head around, irrespective of one’s familiarity with gold mining. Thus, a dollar’s meaning was relatable to all and objective.

Remember, money is an abstraction. It’s a placeholder for real-world value in the fungible form. Money represents goods and services that we already produced and those that we will come to purchase in the future. It’s not arbitrary nor a subjective social contract. It’s a literal measurement of the fruits of our labor.

However, there is no monetary standard for value in a fiat currency regime, by definition (i.e. fiat)! A dollar, to continue with our example, is simply worth whatever it will fetch in trade. Thus, it has different values to different people. It is subjective. While innocent-sounding in theory, it’s a disaster in practice.

Simple example

Imagine remodeling your kitchen using vendors that each had their own measurement standard. Coordination becomes impossible. How could you know which oven to order, or how many tiles you need, or if the cabinets fit together? Each item would come in sizes that bear no resemblance to the other. Ultimately, you’d need to guess with your orders and then modify and/or rebuild each item yourself once they arrived to fit the spaces; assuming you even could. The remodel would be highly inefficient and a complete disaster by today’s standards.

The same standard requirements apply to value, and thus to money. Money is abstract so it’s harder to see, but it’s nonetheless real. To be sure, we get this. The inherent need to relate money’s denominations to our actual lives has led people to CPI (as fiat regimes lack any). While we don’t actually define a dollar’s economic value, we do try to track its relative fluctuations. When CPI grows, we call that inflation; when it falls, we say there’s deflation. It’s a valiant attempt, really. Nonetheless, it’s problematic. The result is doom: either for inflation or prosperity.

Inflation is shortages

Today, inflation can only result in doom. Either CPI continues to decline—wiping inflation from the face of the planet—or the arc of human prosperity reverses course. They cannot coexist.

Just think for a moment: How can deflation—falling prices and improving the quality of goods and services —be bad? They are literally the calling cards of prosperity. Consider that, according to one study, “an unskilled laborer saw his or her purchasing power double every 34 years” over the last hundred years when scaling food prices to wages. That’s some serious deflation! Yet, is there any doubt that life is better now?

Humans being humans—and companies being collections of us—are driven to improve our circumstances. We are profit maximizers in a deeply profound and inspiring way. Businesses do this by lowering prices while increasing operational efficiencies that result in higher volumes, margins, and profits—the ultimate goal. So long as economies stay free, companies will work to debottleneck supply chains, increase production, and grow profits. This means lower prices to come. Inflation should go extinct.

Yet, today we find ourselves with rising prices and growing CPI. Why? Did the central bankers finally get monetary policy “right” and achieve their inflation goals? Did legislatures perfect their fiscal spending budgets? No, not lowering interest rates to zero (and below), nor endlessly buying bonds, nor spending trillions on stimulus had any impact on CPI growth.

Rather, today’s intensifying inflation was caused by the global lockdowns. Inflation only came from severe economic disruptions, mass unemployment, and bankruptcy. Inflation resulted from shortages.

Just let that sink in for a moment.

There’s opportunity in transitory

Thus, I believe today’s inflation is transitory. Forced lockdowns and abrupt economic restarts created widespread shortages that should prove to be temporary. Companies and people will get back to work and solve these supply chain bottlenecks in order to meet the unyielding demand. It’s what we do: seek to improve our lives.

However, these actions will take time to implement. Price changes filter slowly throughout the economy, both increases and decreases. How long a lag—weeks, months, years—will be specific to each good and service as companies react with varying abilities and speeds. Remember, inflation today is the average price change. By definition, it will transition, not leap like a debasement.

Thus, CPI growth could continue to trend up before it ultimately falls. This may have important implications for various assets like bonds and commodities that correlate to these moves. Trading opportunities may be created—in both directions—if people mistake “on average” for all.

No better cure for high prices than high prices

The recent rise in inflation has understandably captured the market’s attention. It’s an important valuation component for many asset classes and thus has significant investment implications. Furthermore, runaway inflation is a popular doomsday scenario. People are naturally concerned that Fed will be late to act.

However, inflation’s link to monetary policy is a relic. Inflation’s definition changed over the years. It no longer means the debasement of a monetary standard. There simply is no monetary standard to debase in a fiat currency regime. The Fed plays no role.

Today, inflation simply means “price increases”—on average—of some defined basket of goods and services. Prices are determined by supply and demand dynamics throughout the entire economy, not monetary policy. People and corporations seek to lower prices in order to maximize profits and prosperity. Inflation is caused by shortages. Hence, it’s rising in the post-COVID-lockdown economy as demand returns to a shrunken supply base.

Today’s rise in prices is nothing to fret about. It bears no resemblance to the hyperinflation experienced by the Weimar Republic, Zimbabwe, or Venezuela. While certainly unpleasant, the CPI growth is simply the market doing what it’s supposed to do. Soon enough, enterprising people will debottleneck supply chains to meet demand and lower prices. Deflation will surely return so long as people are free, though it will take some time.

To be sure, trading opportunities may be created if people conflate inflation’s historical and contemporary definitions. Remember though, there’s no better cure for inflation than inflation.