Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

But deposit-taking banks have pulled back.

Lovingly known as “shadow banks,” nonbanks have come to dominate the mortgage market. And they originate the riskiest mortgages. The government — mostly the Federal Housing Administration (FHA) — is on the hook. Nonbanks do not take deposits and are not regulated by banking regulators (Federal Reserve, FDIC, and OCC). Their funding is derived mostly from selling the mortgages they originate, but also from bank loans and other sources. During the mortgage crisis, a slew of them got in trouble and, because they did not hold deposits, were allowed to collapse unceremoniously.

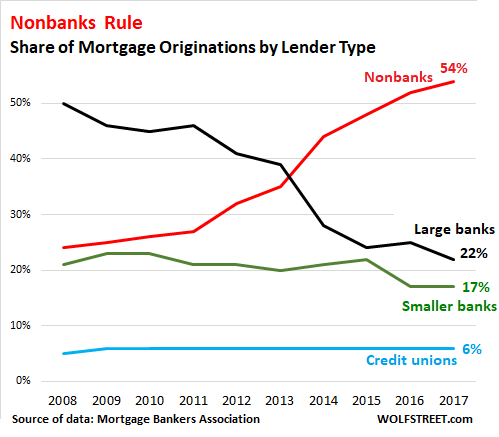

Today, there’s a new generation of shadow banks dominating mortgage lending. According to a February 2019 report by the Mortgage Bankers Association, the share of mortgage originations by nonbank lenders has surged from 24% in 2008 to 54% in 2017, while the share of large banks has plunged:

The largest nonbank mortgage lender, Quicken Loans, originated an estimated $86 billion in mortgages in 2017, according to the MBA’s February 2019 report, giving it a market share of just under 5% of all mortgages written during the year.

These shadow banks are unlikely to get bailed out in a crisis, and investors will take the loss. From that perspective, taxpayers are off the hook. But their counterparties are also at risk of losses – with the government by far the most exposed. These counterparties fall into two groups:

Large banks extending “warehouse financing” (short-term credit lines secured by mortgages) to nonbanks to fund the mortgages temporarily until they’re sold into the secondary market.

The US government, through government agencies such as the FHA which specializes in riskier mortgages that it insures and guarantees but does not buy, or Ginnie Mae which buys and guarantees mortgages; and government sponsored enterprises Fannie Mae and Freddie Mac which buy and guarantee mortgages.

In its wide-ranging report and briefing materials (February 25, 184 page PDF) on the housing market and government involvement in it, the American Enterprise Institute (AEI) outlines how surging home prices push lenders to take ever greater risks. And as deposit-taking banks have pulled back from those risks, shadow banks have plowed ever deeper into them.

I will focus on a small aspect of the report: The increasing role of shadow banks in the mortgage business and the exploding role of the FHA in insuring and guaranteeing their mortgages that are becoming riskier and riskier.

FHA insures mortgages on single-family and multifamily homes to high-risk borrowers. It operates on the revenues it receives from the mortgage insurance premiums that borrowers pay upfront and monthly. To qualify for FHA insurance, mortgages must meet certain requirements. When homeowners default on their mortgages, the FHA covers 100% of the lender’s loss. It currently insures nearly 8 million single-family mortgages and about 14,500 apartment buildings.

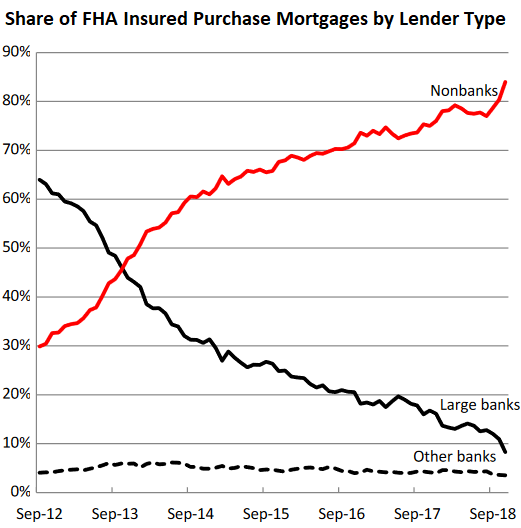

The chart below by the AEI shows how nonbanks completely dominate FHA-guaranteed “purchase mortgages” (we’ll get to “refinance mortgages” in a moment). The chart excludes mortgages by State Housing Finance Agencies and Credit Unions, accounting for 4% of the FHA purchase-mortgage market. In November, the share of originations by nonbanks of FHA-insured mortgages surged to 85%:

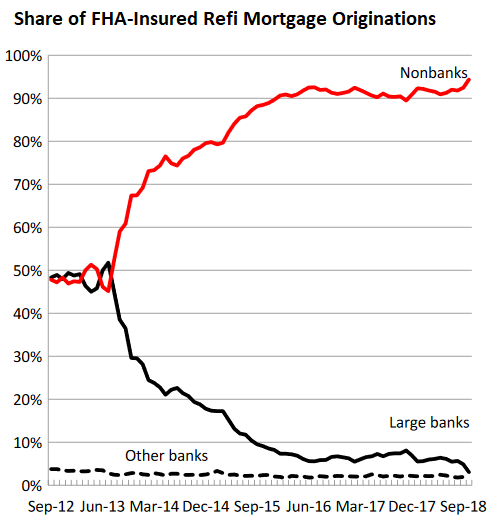

In terms of FHA-insured refinance mortgages, the shift to nonbanks is even more striking. In 2012, nonbanks and banks originated about the same volume. By November 2018, nonbanks originated 94% of all FHA-insured refi mortgages:

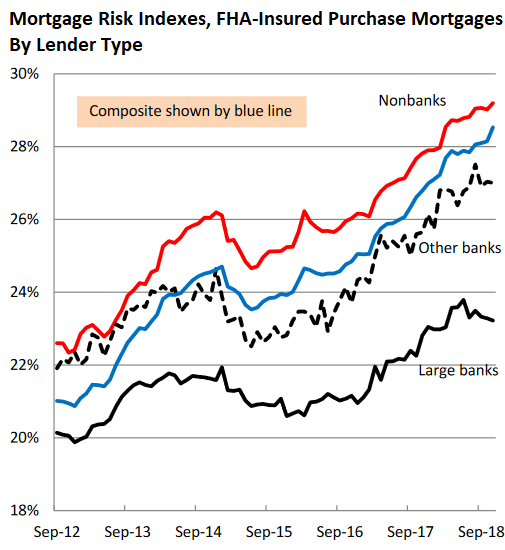

“Migration to nonbanks has boosted overall risk levels, as nonbanks are willing to originate riskier FHA loans than large banks,” the AEI says. This is shown by two risk measures.

The first is the Mortgage Risk Index (MRI), a stress test that measures how the mortgages that were originated in a given month would perform if subjected to the same stress situation as mortgages originated in 2007, which experienced the highest default rates as a result of the Great Recession.

The AEI’s chart shows how risks of FHA-insured purchase mortgages, as measured by the MRI, have risen across the board, but much less at large banks than at nonbanks:

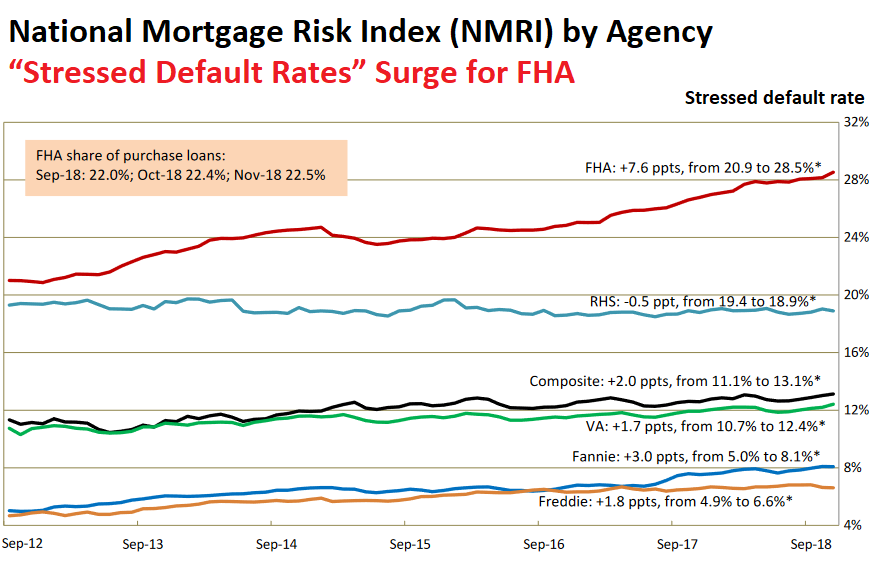

The second risk measure the AEI uses is the National Mortgage Risk Index (NMRI), a standardized quantitative index for mortgage default risk based on the performance of the 2007 vintage loans with similar characteristics. NMRI is expressed in a percentage, the “stressed default rate”:

- A higher rate means increasing leverage and looser lending standards and therefore higher risk of default;

- A lower rate means decreasing leverage and tighter lending and therefore lower risk of default.

The composite NMRI (black line in the chart below) has been trending up since mid-2013, with all agencies except the RHS drifting higher. While Fannie and Freddie guaranteed mortgages are at the bottom with stressed default rates of 8% and 6%, the stressed default rate for FHA-insured mortgages have surged, including a 7.6-percentage-point jump over the past 12 months, to 28.5% (click to enlarge):

Since nonbanks originated most of the FHA-insured mortgages over the past few years – in November, 94% of all FHA refi mortgages and 85% of all FHA purchase mortgages – the “stressed default rate” for the FHA reflects mostly the risks of mortgages originated by nonbanks.

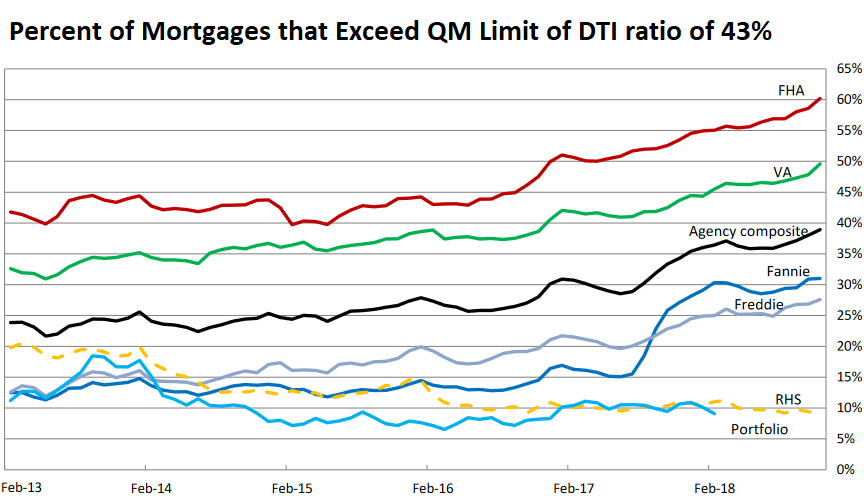

The debt-to-income (DTI) ratio shows a similar scenario. It gauges the ability of a borrower to repay a mortgage by measuring the income consumed by servicing all outstanding debts of that borrower.

The upper limit of the DTI ratio for “qualified mortgages” (QM) under the Dodd-Frank Act is 43%. A mortgage that meets the QM requirements provides legal protection for lenders against a claim that the mortgage was made without due consideration of the borrower’s ability to repay. But Fannie Mae, Freddie Mac, FHA, VA, and RHS are exempt mostly from the QM requirements, and so here we go:

- In November, a record 60% of FHA-insured purchase mortgages exceeded the QM limit for DTI.

- 50% of VA mortgages exceeded the QM limit.

- But Fannie and Freddie mortgages are well below the limit at around 30% (click to enlarge):

So there are two dynamics that would be needed for future support of the housing market, according to the AEI:

- Accelerating household incomes

- “Further increases in leverage from an already high level.”

The first has been arriving too slowly and has been outpaced by home price inflation; and the second – increased leverage – would have to happen at the low end of the household-income scale where the FHA and shadow banks are most active, and where the risks are already the highest, and the borrowers the most vulnerable.

The San Francisco Bay Area and Seattle lead with biggest multi-month drops in home prices since 2012; San Diego, Denver, Portland, Los Angeles also show declines according to the Case-Shiller Index. Others have stalled. A few eked out records. Read… The Most Splendid Housing Bubbles in America Get Pricked