via Austrolib

Summary

- The rate of increase of bank loans has slowed to a trickle since February 2016. When bank loans shrink, a recession often follows due to prolonged low monetary growth.

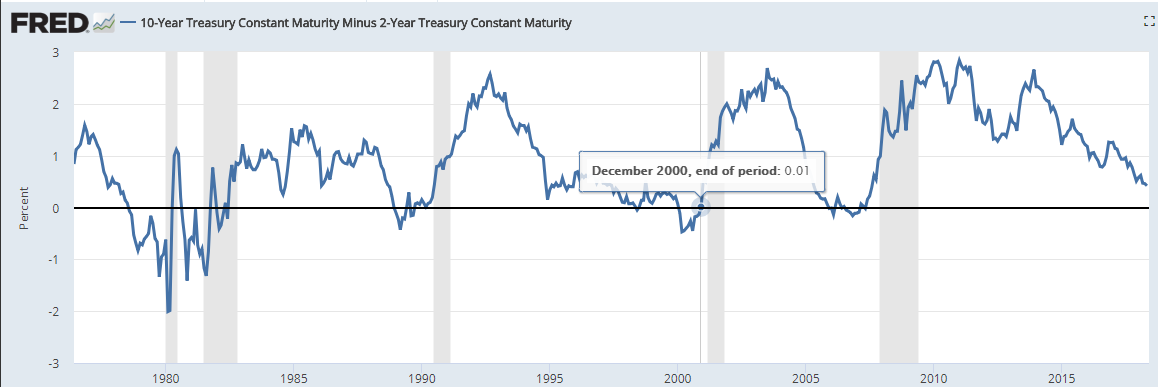

- With the 10Y-2Y yield spread falling back down to 10 year lows, banks have even less incentive to make loans, which may slow monetary growth further.

- The annual trough for monetary growth typically occurs in the last week of August or early September due to seasonal factors. The seasonal low is just ahead of us.

- Interest on excess reserves has been hiked with each Fed rate hike, so there probably won’t be any new money entering the economy from excess reserves.

- These factor suggest investment caution is advised.

When loan growth slows, it’s often a sign of imminent recession because it means less money is being created over the medium term. It’s not always the case, but it was the case in 2008, 2000, 1990, and 1974. Bank loans to the private sector have slowed to a snail’s pace since February 2016. Charts and explanation will follow below.

We are also fast approaching the annual trough in monetary growth that typically makes the next three to four months the most prone to a correction or flash crash, regardless of whether a recession is in the cards or not. Once the capital markets get used to ever larger amounts of money, it causes a boom in stocks, and that boom becomes dependent on ever increasing amounts of money in the system. If we get through the low point this year without the market breaking lower, then stocks could break through to new highs by this winter. But if we don’t, the bull market may be over, in retrospect, since January 26 th when the S&P 500 (SPY) hit its all time high of 2,872.

This year, we have more headwinds. in addition to the annual low point for monetary growth ahead of us (it typically happens in late August or early September). Theese are a worsening trade war as of yesterday when President Trump removed steel and aluminum tariff exemptions for Mexico, Canada and the EU, and a flattening yield curve. Neither of these are good for bank loan growth, which is what expands the money supply in the absence of quantitative easing. As you can see from the chart below from Trading Economics, the rate of bank loan growth has slowed significantly since around February 2016.

The slowed rate can be seen a little better zoomed out.

There was a very brief blip up in bank loans for April that shows up at the very edge of the graph, so this has to be monitored. Since February 2016 though, the annual loan growth rate has been only 6%, from $2T then to $2.162T now. Compare that to the period from February 2011 to February 2016 and it’s an extreme slowdown. Annual loan growth averaged about 14% going from $1.2T to nearly $2T. If loans shrink absolutely, monetary growth comes to a standstill and a recession usually follows. We’re not there yet, but we’re getting closer. A trade war certainly won’t help increase investment or bank loans.

YIELD SPREAD

The tariffs won’t affect loan growth directly, but they will definitely affect steel and aluminum prices very quickly. The increased prices should start showing up in the consumer price index over the next few months, which in turn will keep the Fed hiking rates. This, in turn, will continue to shrink the spread between 10Y and 2Y yields. The lower that spread is, the less banks tend to loan. The shrinking yield spread is already having an effect on bank loans, and trade barriers will only exacerbate this.

A peak in bank lending tends to closely follow the yield spread going negative, in other words 2Y yields higher than 10Y yields. When the yield curve goes negative, bank loans tend to start shrinking. Take a look at this chart from the St. Louis Fed of the yield spread.

The 2001 peak in bank loan growth occurred exactly one month after the yield spread crossed back over into positive territory. Loan growth patterns in 2008 were altered by the passage of the TARP bailouts in October 2008, so we had a sudden jump in loan growth that month due to that particular stimulus, but it didn’t hold. Loan growth had pretty much stopped by April of 2008, which can be seen clearly by zooming in to that time period.

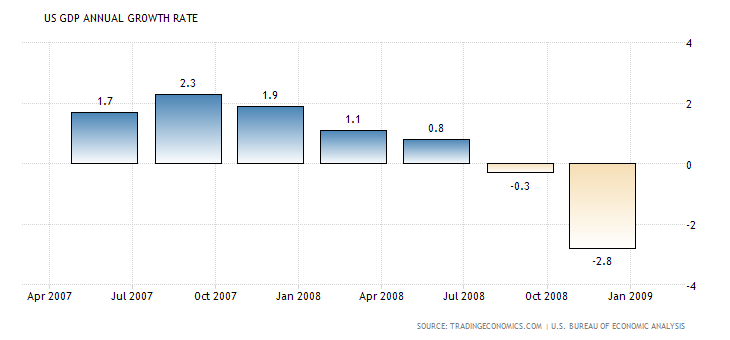

This coincided almost exactly with the beginning of the 2008 recession, two months before GDP began to officially contract.

INTEREST ON EXCESS RESERVES

There is a wild card here as well for monetary growth, and that is interest on excess reserves [IOER]. I speculated in a previous article that a higher overnight federal funds rate (the interest rate that the Fed directly influences) could cause some of the over $2 trillion in excess reserves to pour into the banking system and push monetary growth higher again after the next rate hike, which would bring the overnight rate to a higher rate than the current 1.75% the Fed currently pays member banks to keep that money out of the economy. I now see excess reserves entering the banking system and increasing the money supply as very unlikely, since the Fed has actually been hiking the IOER together with the effective federal funds rate so as to keep that excess out of the economy. (Fed funds rate in red, IOER in blue below.)

Of course the Fed doesn’t necessarily have to hike the IOER this time together with what is assumed will be a June rate hike. If it doesn’t hike the IOER, monetary growth could spurt higher very quickly. A June rate hike being baked into the cake already means that the IOER rate will be much more important come the FOMC meeting on June 13. I doubt the fed will hike rates without also hiking the IOER by an equivalent measure.

The IOER does show up in previous FOMC minutes, but only briefly. The last meeting for which we have minutes available when a rate hike was instituted says this on the IOER:

To support the Committee’s decision to raise the target range for the federal funds rate, the Board of Governors voted unanimously to raise the interest rates on required and excess reserve balances 1/4 percentage point, to 1-3/4 percent, effective March 22, 2018. The Board of Governors also voted unanimously to approve a 1/4 percentage point increase in the primary credit rate (discount rate) to 2-1/4 percent, effective March 22, 2018.

So I think we can safely assume that the IOER will be hiked as well in June. If it isn’t, it will be big news that probably won’t be covered anywhere but Zerohedge because nobody else seems to care about it.

The longer term question is, if rates keep going higher, how much is the Fed willing to literally give away to banks just to keep excess money parked out of the banking system indefinitely? If the IOER goes up to 2% with the next rate hike as expected, the Fed will be handing member banks about $42B in high powered money annually for nothing. Not a bad way to make money if I say so myself. Have your boss bail you out and pay interest on that bailout indefinitely for the service of not using it.

Bottom line, while the IOER needs to be watched, it probably won’t cause any waves just yet, until and unless it falls below the overnight rate.

Now, with slowing loan growth as a backdrop, what is the range of possibilities for monetary growth over the next 3 months? We should have a much clearer picture and tighter range of possibilities by the end of July. The trough doesn’t occur until late August at the earliest. As of now though, the picture is as follows.

I’ve calculated the quarterly average money supply possibilities out to the week of July 17 th by comparing the quarterly average for mid July to the one week average for this week of the year going back to 2010. This week’s one week average is$13.949T. The quarterly average by July 17 th has been anywhere from 0.3% higher to 1.11% higher. That would put the quarterly average at anywhere between $13.993T and $14.104T. That puts the quarterly monetary growth rate at anywhere between 1.3% and 4.5% for the end of July. That is a very big difference, so we’ll have to see what happens.

Conclusion: Very slow bank loan growth, falling yield spread, and a full blown trade war at this point do not paint a good picture. Bank weakness in the European Union and political instability in Italy and Spain don’t help much either. We’ll know more by July, but investors may want to start exercising caution here, selling rallies rather than buying dips.