Since the shock-and-awe surprise rate cut, the S&P 500 has dropped 3.8%.

By Wolf Richter for WOLF STREET.

The whiplash-inducing volatility in the stock market has been quite something. Today, after a last-minute push that fizzled in the last five minutes of trading, the S&P 500 ended the day down 1.7%. By the size of recent moves, that was mild.

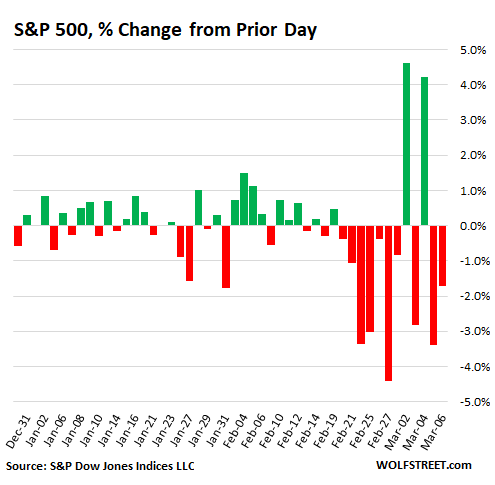

Over the prior four days through Thursday, the S&P 500 rose or fell over 2% each day, with two moves over 4% and two moves around 3%. These four sessions in a row of moves over 2%, up or down, had been the longest such stretch since 2011 (August 8,9,10, and 11), during the euro debt crisis. And before then, four days in a row of 2%-moves, up or down, occurred in October and November 2008, after Lehman had collapsed. Over the past 10 trading days, the S&P 500 moved over 2% in seven of them – two up, five down — and it moved by 3% or more in six of the past 10 trading days:

In the 12 years since 2008, there has not been a series of five days in a row with 2%-moves. Today almost made it to become that fifth day of 2%-moves (until the last 20 minutes), but no cigar.

And this very week, on Tuesday morning, the Fed came out with its surprise shock-and-awe 50-basis point rate cut that has triggered a huge rally in Treasury securities, with the 10-year and 30-year yields plunging to record lows. A rate cut of this type was hoped to boost stocks into the stratosphere, but the opposite happened.

On March 3, the day of that infamous cut, the S&P 500 dropped 2.8% [Stocks Sag as Fed Cures Coronavirus by Cutting Rates ½ Percentage Point]. The next day, it spiked 4.2%, but Thursday and Friday, markets came unglued again. Over the four days since the shock-and-awe rate cut, the S&P 500 has dropped 3.8%.

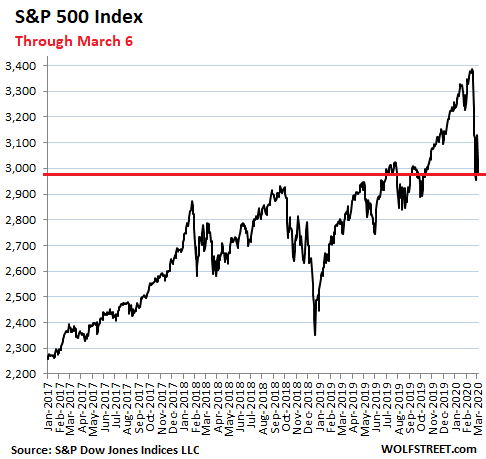

The S&P 500 has now declined 12.2% from its closing high 12 trading days ago. Year-to-date, the S&P 500 is down 8.0%. So that’s not a whole lot, but the way it got there, with huge drops and jumps, was a little rough. Despite the five days this week of market turmoil, up and down, in total, the S&P 500 ticked up 0.6% from the close last Friday. Those five days are the fat part in the straight line down:

A similar scenario played out in the other indices:

- The Nasdaq dropped 1.9% today, is down 4.4% year-to-date, and down 12.6% from its closing high on February 19.

- The Dow Jones Industrial Average fell 1% today, and is down 12.4% from its closing high on February 12.

- The Russell 2000 index for small capitalization stocks dropped 2% today, is down 15% from its closing high on January 16.

So just looking at the numbers, with indices down 12% to 15% from their closing highs, this selloff is nothing special. But the volatility of it, the huge moves up and down over the past two weeks have jangled some nerves.

The coronavirus-containment efforts have seriously impacted some sectors, including the entire travel sector. And the stocks of cruise ship operators and airlines have gotten totally crushed over the past two weeks.

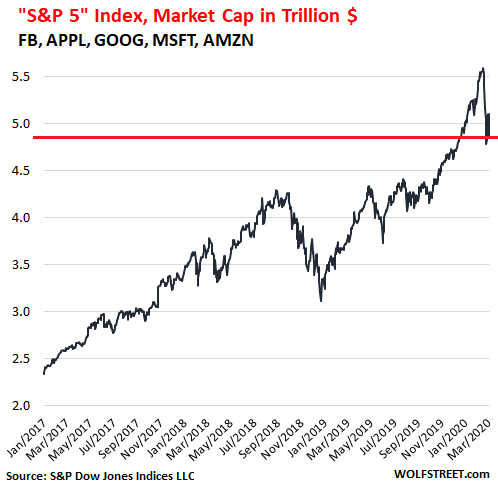

But in terms of size – and weight in stock market indices – they pale compared to Apple, Alphabet, Microsoft, Amazon, and Facebook. The combined market capitalization of those five companies reached $5.59 trillion at the peak on February 19. The market cap of the S&P 500 is $24.4 trillion. Without these five companies, the remaining 495 or so of the S&P 500 companies had a combined market cap of around $19.5 billion at current prices. So now I have a new index, the “S&P 5” – and it has dropped 13.3% from the peak on February 19:

In terms of the overall stock market, the standout hasn’t been the decline over the past two weeks – it’s rather mild – but the brutal volatility of it, the huge back-to-back up-and-down moves that indicate that there is more afoot than just a regular stock market correction.

The fact that this type of volatility occurred most recently during the euro debt crisis (2011) and during the US Financial Crisis (October and November 2008) is not a propitious sign.

And in terms of the Fed bailing out the stock market with further rate cuts, well, there is not all that much left to cut. Two more shock-and-awe cuts, and it’s over. The Fed has moved negative interest rates off the table, for a big reason: In countries where negative interest rates are the policy, bank stocks have gotten totally crushed and have been reduced to a tiny fraction of their pre-financial crisis peaks.

The ECB is trying to keep the Eurozone glued together, and it doesn’t care much about bank stocks. But the Fed works for the banks. The banks own the 12 regional Federal Reserve Banks, and their governors sit on the FOMC, which creates a different relationship. So the Fed isn’t going to do NIRP, because it would crush bank stocks. It might use other “tools,” but not NIRP.