Flip on CNBC, pick up a financial paper, or scroll a financial website and you will find a great range of materials discussing the stock market, hot stocks, bad stocks, stock trading tips, and stock investment strategies.

Why? Because stocks are sexy, and the Wall Street casino — with all its flickering lights, screaming patrons, and carnival barkers — makes money for the purveyors of products ranging from IPOs to mutual funds and investment research.

On the other hand, you don’t hear much about bonds. Why? Because bonds are boring? Maybe so. Historically, however, discounting bonds has constituted an investment mistake, and the inevitable cooling down and possible volatility of the stock market in the next decade will make bonds a crucial part of your portfolio.

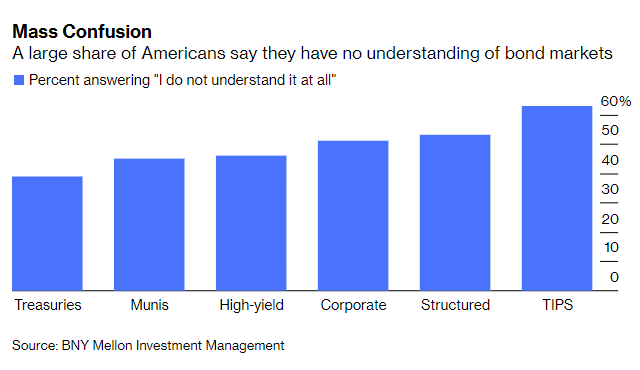

A recent BNY Mellon Investment Management survey underscored the lack of understanding about bonds and the bond market.

“A BNY Mellon Investment Management national survey on fixed-income investing was stunning: A measly 8% of Americans were able to accurately define fixed-income investments.

The 29-question online survey of just more than 2,000 adults, conducted in July, clearly shows that many Americans admit to having little knowledge about various fixed-income markets and how to invest in them. Here’s a rundown of those who answered “I do not understand it at all” with regard to the following types of bonds: Treasuries, 39%; municipal bonds, 45%; high-yield bonds, 46%; corporate bonds, 51%; structured products, 53%; Treasury Inflation Protected Securities, 63%. Of the 849 respondents who don’t own fixed income or don’t have any investment portfolio, 44% said they don’t buy bonds because they don’t understand the different types of securities.”

This is fascinating but not surprising. Since the financial media focuses only on headline-grabbing corporate news, the minute-by-minute price change of the markets, or what some investment guy with a product to sell you has to say, bonds don’t get much attention.

But, as BNY states, if you don’t understand what bonds are — and more importantly, what they can do for your portfolio — you may be missing out on something really big: And not just if you’re a retiree either.

Bonds can play a vital role for investors of any age because they reduce overall portfolio volatility. The less volatility a portfolio has, the less likely an investor will be to act emotionally during market declines and panic-sell investments to reduce losses.

Bonds also provide the third leg to the total return of a portfolio. Equities offer the first two legs, capital appreciation and dividends. Bonds offers stability by providing investors with both a safety-of-principal function (by returning the initial principal at maturity) and interest income.

Adding bonds to portfolios create better diversification and asset allocation for investors, which can lead to better returns over time, particularly during periods of increased volatility.

Is It The Right Time To Invest In Bonds?

Because interest rates are currently low, concerns about a recession in the U.S. economy have risen. This has led many media commentators to suggest the bonds are now wildly overvalued. For example:

“When evaluating the desirability of government bonds as a long-term investment, it’s imperative to compare the prevailing yields of bonds with the earnings yields for stocks.”

While this is a common comparison, it is also wrong.

Let’s compare the two:

Earnings Yield

- “Earnings yield” is the inverse of P/E ratios and tells you only what the yield is currently, not what it will be in the future.

- Investors do not “receive” an “earnings yield” from owning stocks. There is no “yield payment” paid out to shareholders; it is merely a mathematical calculation.

- There is no protection of principal.

Treasury Yield

- Investors receive a specific yield, calculable to the penny, which is paid to the holder.

- Holders also have a government-guaranteed return of principal at maturity.

As we have written previously, it is essential to align expectations and investing requirements. Stocks have liquidity, and potential return (or loss), but no safety of principal. Treasuries have a stated return and a high degree of safety. However, to guarantee the stated return, Treasuries must be held to maturity and may not be liquid, if liquidity is part of your goal.

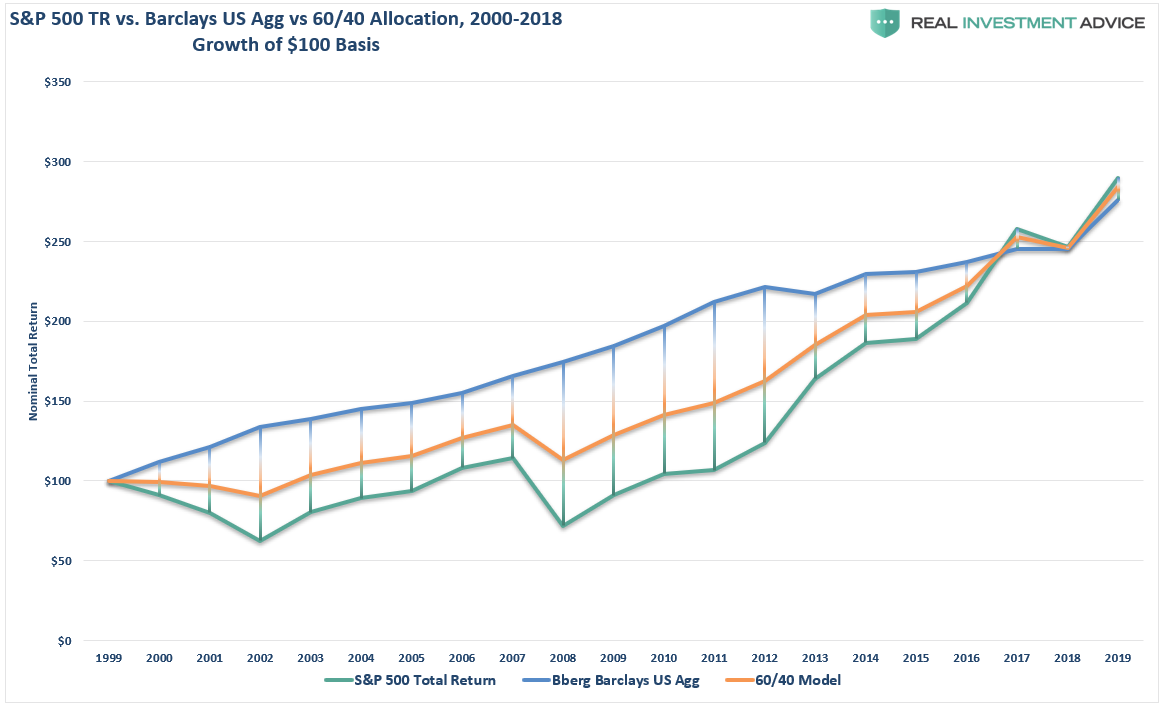

For most investors, completely discounting the advantage of owning bonds over the last 20 years has been a mistake. By reducing volatility and drawdowns, investors were better able to withstand the eventual storms that wiped out large chunks of capital.

Some may look at the graph below and see that bonds and stocks are at the same level. While this is true, bonds gave you the same amount of return as stocks with much less risk (and, needless to say, stress) during two major bear markets.

It is also worth pointing out that stocks are once again grossly overvalued, and a significant drawdown is probable in the coming years.

Over the next decade, the prospect of low stock market returns, possibly approaching zero, seems much less appealing than the positive return offered by risk-free asset.

Given that we are in the most extended bull market cycle in history, combined with high valuations and weakening fundamentals, it might be time to pay more attention to what bonds can offer you.

They could turn out to be one of the best-performing assets in your portfolio during the next cycle.