My concerns about the U.S. automobile bubble are being confirmed. As Bloomberg reports:

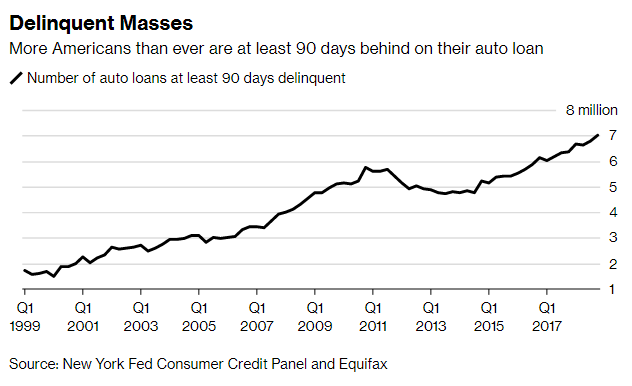

More Americans than ever are at least three months behind on their auto loans, a sign that the U.S. economy may have little growth left in the tank.

The number of loans at least 90 days late exceeded 7 million at the end of last year, the highest total in the two decades the Federal Reserve Bank of New York has kept track. Expressed as a percentage of total debt, the delinquency rate is the highest since 2012, as overall borrowing has also increased.

The data show not all Americans are benefiting from the strong labor market, New York Fed economists say. Consumers with the weakest credit have driven deteriorating performance of auto debt: The share of subprime borrowers who fell well behind on car payments the last three months of the year was the highest since the second quarter of 2010.

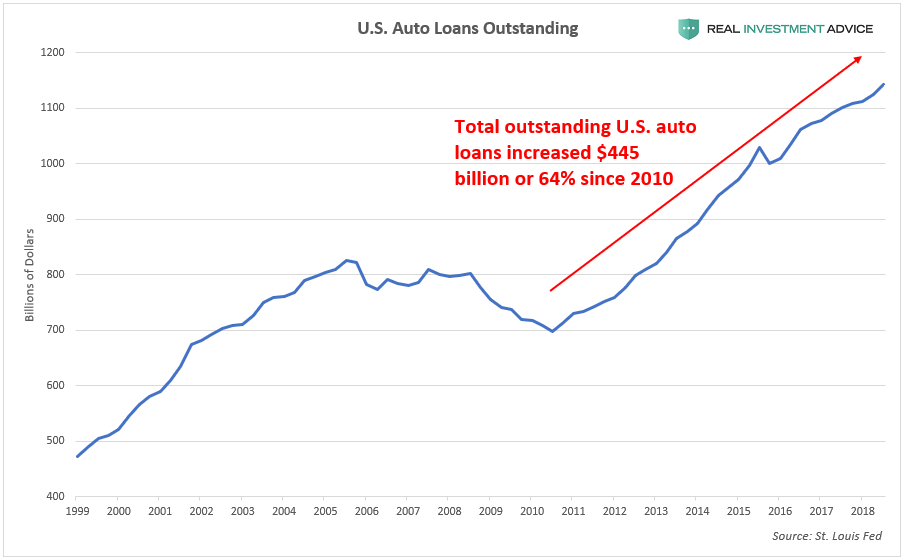

As I’ve been warning for the past couple years, the U.S. automobile sales boom is a byproduct of a bubble in auto loans:

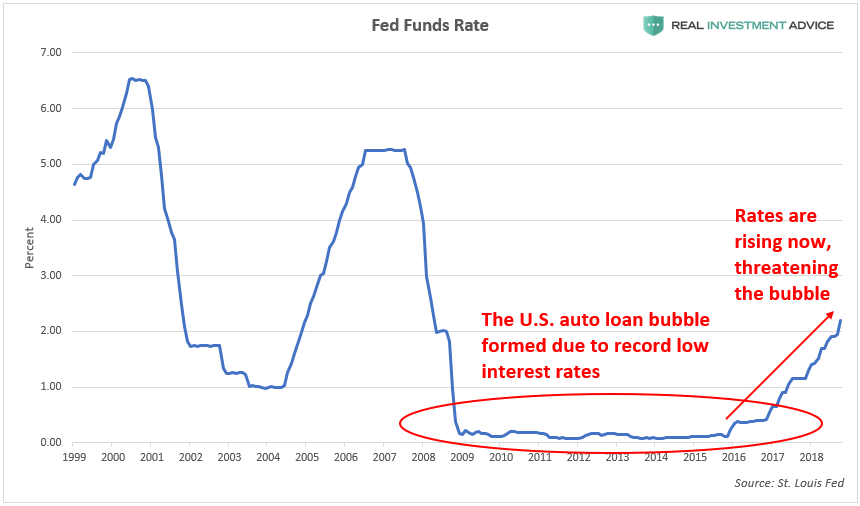

The auto sales and auto loan bubble is a byproduct of ultra-cheap credit conditions in the past decade since the Great Recession. Interest rates are now rising, which threatens the auto bubble:

It’s only a matter of time before the U.S. auto sales and loan bubble experiences a serious bust. Rising delinquencies are just the start, I’m afraid. Booms fueled by cheap credit always end the same way – in a terrible bust. Ignore the voices that say “this time will be different!”