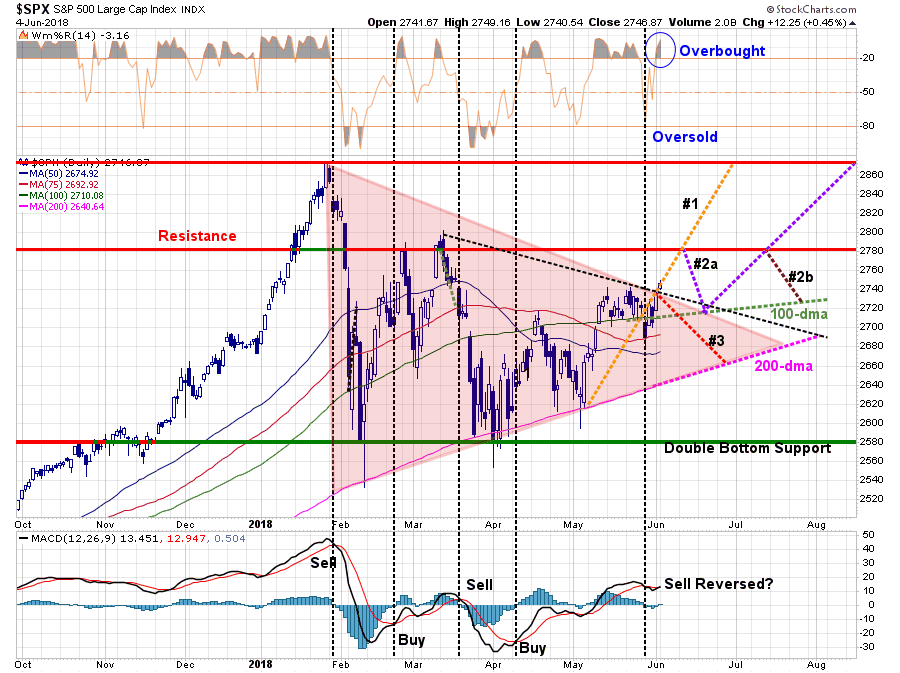

On Monday, stocks opened higher as the bulls pushed the market above overhead resistance. In this past weekend’s missive, I updated our ongoing “pathway” analysis which continues to drive our overall portfolio positioning currently. To wit:

“As shown by the reddish triangle, the ongoing consolidation process continues. Eventually, this will end with either a bullish or bearish conclusion. There is no ‘middle ground’ to be had here.

- Pathway #1 – a breakout to the upside on heavy volume that pushes the market through resistance at 2780 and back to old highs. (Probability 20%)

- Pathway #2a and #2b – a breakout to the upside which fails resistance at 2780. The market then either a) retests the 100-dma and then is able to push to old highs, or, b) fails at 2780 a second time and continues the consolidation process through the summer. (Probability 50%)

- Pathway #3 – the market breaks down next week on continued geopolitical worries, economic data or some unexpected catalyst and retests the 200-dma. (Probability 30%)

I have increased the more “bearish” probability from 20% last week to 30% this week given the triggering of a short-term ‘sell-signal.’ (Lower panel)”

With the higher open on Monday, the market broke above the downtrend resistance and is set up to test resistance at 2780. With the market back to overbought currently, it is likely that 2780 may well be a challenge to the bulls in the near term. Pathway #2a and #2b continue to be the highest probability outcomes currently.

However, a “one-day” move is not necessarily the start of a new trend.

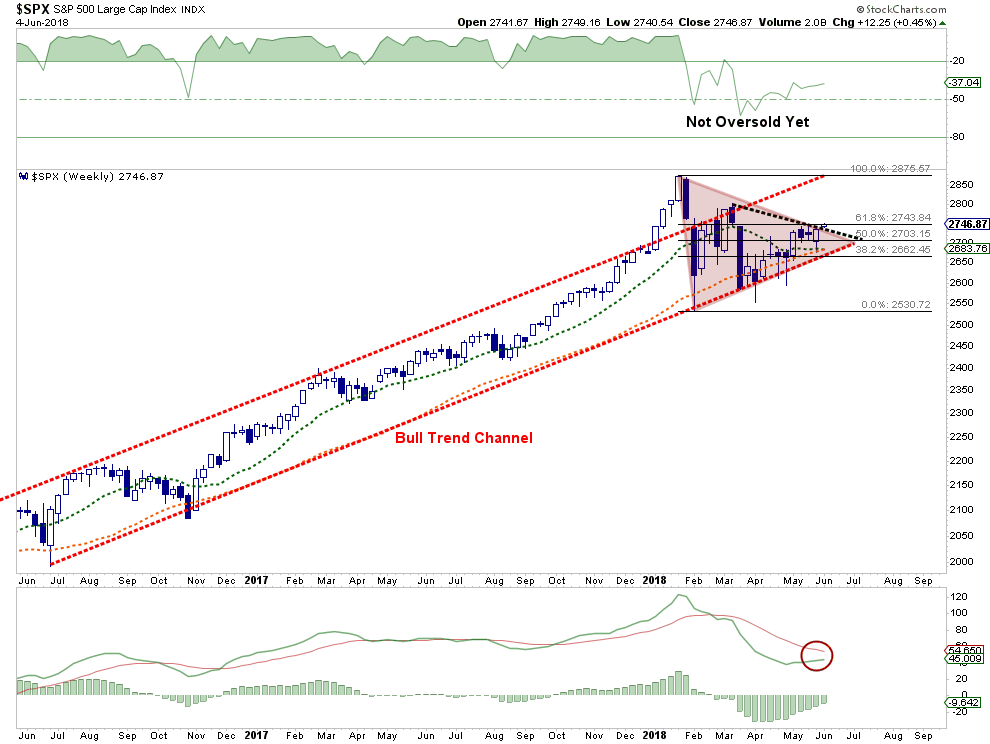

As we discussed previously, from a portfolio management perspective we rely much more heavily on “weekly” data as it smooths out the “volatility” of daily price movements. Given that we are “longer-term” investors, seeking to deploy capital for extended periods of time, using weekly data helps reduce the issues of “head fakes” or “false breaks” which lead to a variety of bad investing outcomes and behaviors. Also, weekly data reduces the emotional “wear and tear” on investors over time by keeping the primary focus on the “trend” of the data.

If we take a look at the weekly chart, a slightly clearer picture emerges.

As shown in the chart above, the consolidation process continues as in the daily chart above. While the market is appearing to bullishly “break out” of the current consolidation pattern, such will not be “confirmed” until the end of the trading week. On Friday, if prices have reversed, then the “break out” will NOT have occurred and portfolio allocations will remain flat.

Furthermore, on a “weekly basis,” the intermediate-term “sell signal” remains which suggests continued pressure on stock prices in the short-term. While the signal is improving, it has not confirmed an increase in equity allocations just yet. The market is also wrestling with a 61.8% Fibonacci retracement from the February lows which is providing some resistance.

We want to give the “benefit of the doubt” to the “bulls” currently. The action on Monday was indeed bullish, and sets us up to add further equity exposure to portfolios, but we will wait for confirmation of the weekly data.

Our worry is the “bulls” seem to charging directly into a potential “trade war.”

A “Trade War” Cometh

As discussed this past weekend, there are a litany of issues which currently concern us particularly has we meander further into the “seasonally weak” period of the year.

- Italian “debt” is a problem. While it was quickly dismissed by the markets, the potential impact to the global financial system is magnitudes larger than Greece was.

- The elected officials in both Spain and Italy are not particularly “EU” friendly with both recent appointments primarily anti-establishment officials.

- Deutsche Bank is a major issue of concern.

- The Fed is raising interest rates and reducing their balance sheet.

- Short-term interest rates are rising rapidly.

- The yield curve continues to flatten and risks inverting.

- Credit growth continues to slow suggesting weaker consumption and leads recessions

- The ECB has started tapering its QE program.

- Global growth, especially in Europe, is showing signs of stalling.

- Domestic growth has weakened.

- While EPS growth has been strong, year-over-year comparisons will become challenging.

- Rising interest rates are beginning to challenge the equity valuation story.

However, the biggest immediate concern is the implementation by the current Administration of “tariffs” not only on China but the EU, Mexico, and Canada.

On June 1st, the Administration announced tariffs on steel and aluminum products. On June 15th, the Administration will announce further tariffs on roughly $50 billion of imported products from China.

While “tariffs” sounds like a rather benign issue, it is simply another word for “tax.” In this case, it is a 25% tax increase on the goods and services being penalized. But it is not just those specific goods and services that rise in price, but all related and affected goods and services.

When tariffs are applied, the cost of steel, aluminum, and everything comprised of those commodities, will rise in price. Products, like automobiles, which use imported parts will also rise in price if the imported component increases in cost. As Doug Kass noted previously:

“What I believe they don’t understand is how interconnected the global economy is today compared to the past. As each year progresses, the role of world trade increases and the role of non-US operations in our largest multinationals multiply. Just look at the ever-expanding role of exports (and non-US sales) in the S&P Index – it’s increased as a percentage of total revenues by 2.5x in the last few decades.”

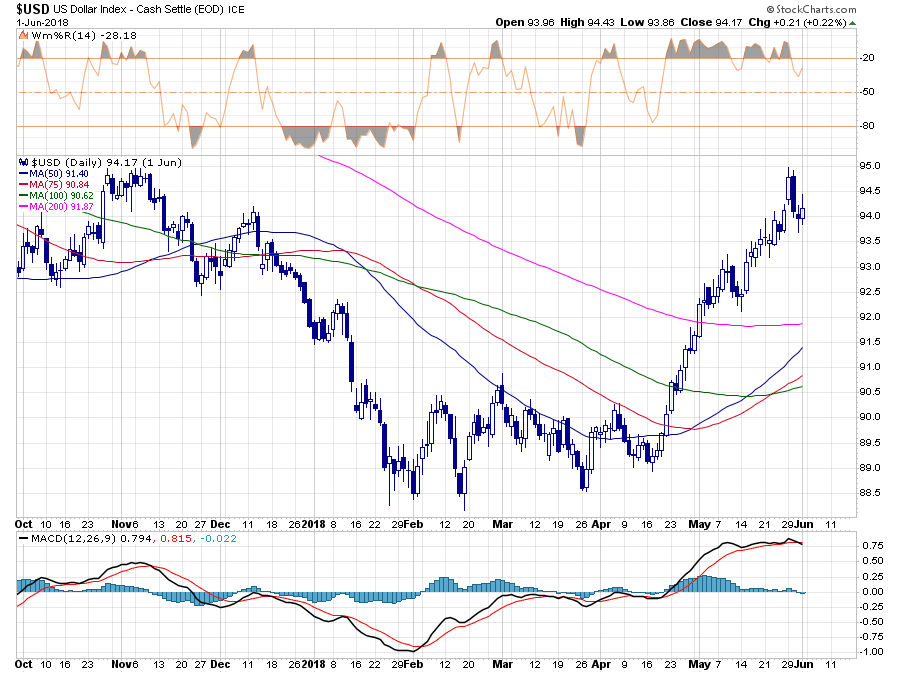

Throw into the mix a stronger dollar, and the risks increase further. As Garfield Reynolds blogged for Bloomberg:

“The law of unintended consequences is striking again. This time it’s the surge in the U.S. dollar that’s being fueled by decisions from President Donald Trump -who seems to prefer a weaker currency – to intensify his attacks on the current ‘unfair’ global trade regime.

The U.S.’s insistence on using tariffs as a weapon came as the White House dropped any effort to seek trade rebalancing through a weaker USD and decided against naming any nations as FX manipulators.

As Trump’s trade stance became more truculent, the dollar just kept climbing. That was puzzling because classic havens such as JPY, CHF, and gold were seeing little benefit as market fears heightened.

It’s become clear that the dollar gained because the impact of Trump’s stance was seen benefiting U.S. assets on a relative basis.”

“Yes, a major trade war is likely to cause damage to the U.S. economy, but a lot of that will be in the longer term. It’s going to cause significantly more pain, especially in the short term, to all those exporters Trump is targeting; and the U.S. is far and away the world’s largest net importer.

This issue is helping to leach investment out of EM in particular, with major developing economies among those most at risk from a U.S.-initiated trade war. Developing Asia, for example, sends 18% of its exports to the U.S., almost three times what it sends to Japan, the next- biggest single-country destination.“

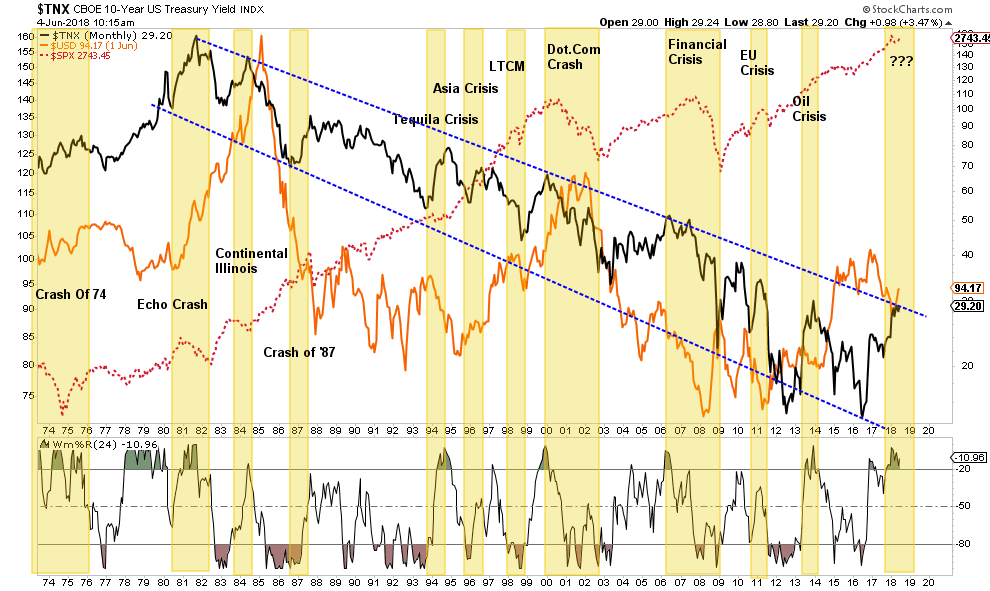

With the 10-year treasury rate now extremely overbought on a monthly basis, combined with a stronger dollar, the impact historically has not been kind to stock market investors. While it doesn’t mean the market will “crash” today, or even next week, historically rising interest rates combined with a rising dollar has previously led to unexpected and unintended consequences previously.

As I have stated previously:

“We remain keenly aware of the intermediate-term “risks” and we continue to take actions to hedge risks and protect capital until those signals are reversed.”

We also remain acutely aware of the longer-term capital risks due to elevated valuation levels, the length of the economic cycle, and weakening annualized comparisons going forward. While it is not yet time to be exceedingly “bearish” on equities, it is no longer advantageous to be exceedingly “bullish” either.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In