“Pet Rocks” first appeared in the mid-70s as a novelty item. Just recently, digital NFT’s of “pet rocks” sold for over $100,000. To wit:

“Rarely do they create waves for investing in something as dead as a rock. Well, they do now. A digital painting of a Grey-coloured rock, part of a pet project from 2017, has sold for an outrageously high price. Its non-fungible token (NFT) version was sold for ETH 33 — equivalent to $100,000 (roughly Rs 75 lakhs). These rocks are one of the first-ever NFT collectible projects on the Ethereum blockchain. Only 100 such “pet rocks” were created.”

As I noted on my Twitter feed:

“If you don’t know what a ‘pet rock’ is, you are probably too young to have experienced a real bear market.”

Yes, people really did buy these and as Peter Atwater noted:

We have previously discussed the many similarities we see between the peak of the markets in 1999 and today. When there is too much money chasing too few assets, digital “pet rocks” are typically a sign of exuberance.

Signs Of A “Rich” Market

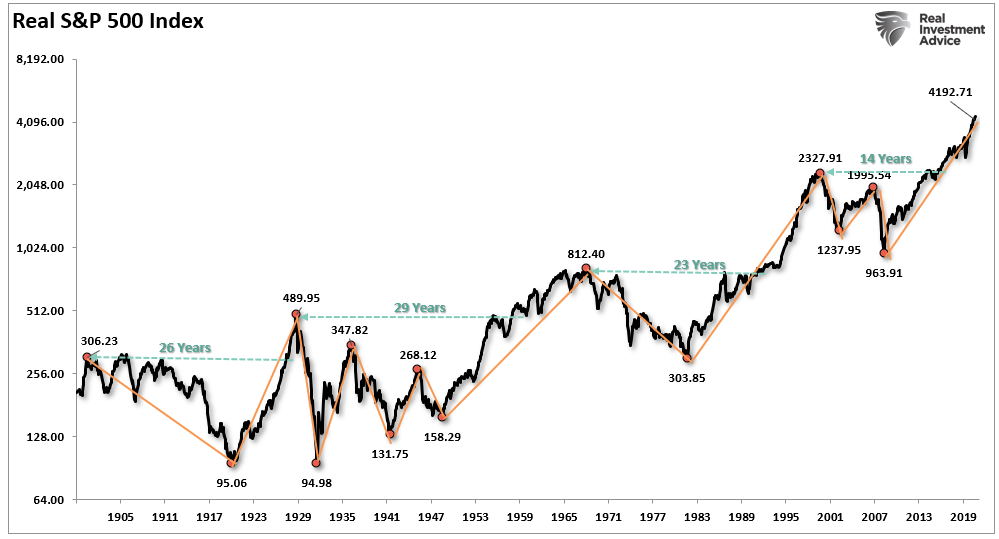

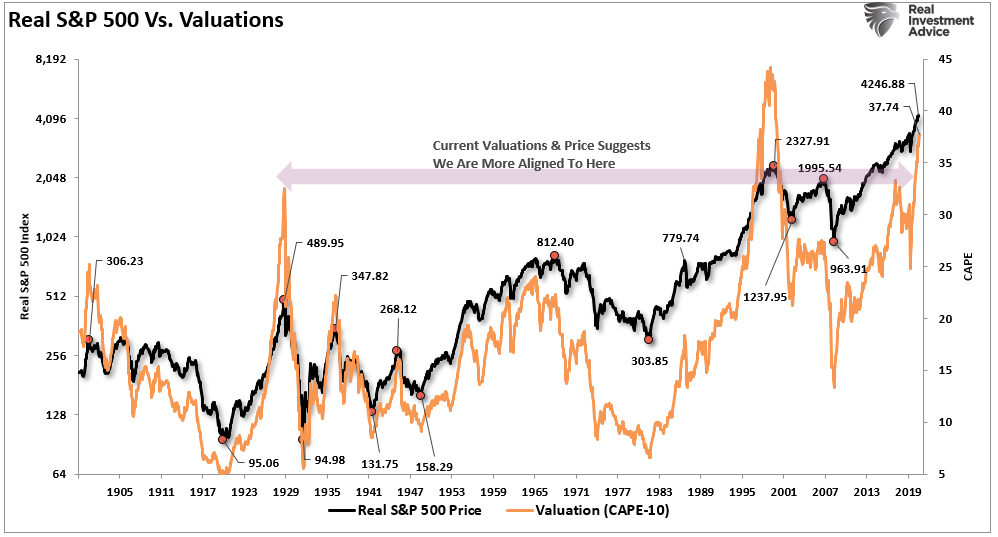

As noted previously, valuations are a terrible market timing indicator. However, in the short term valuations tell you everything about market psychology. In the long term, they tell you everything about expected returns.

Currently, every measure of valuation suggests investors have thrown all “caution to the wind.”

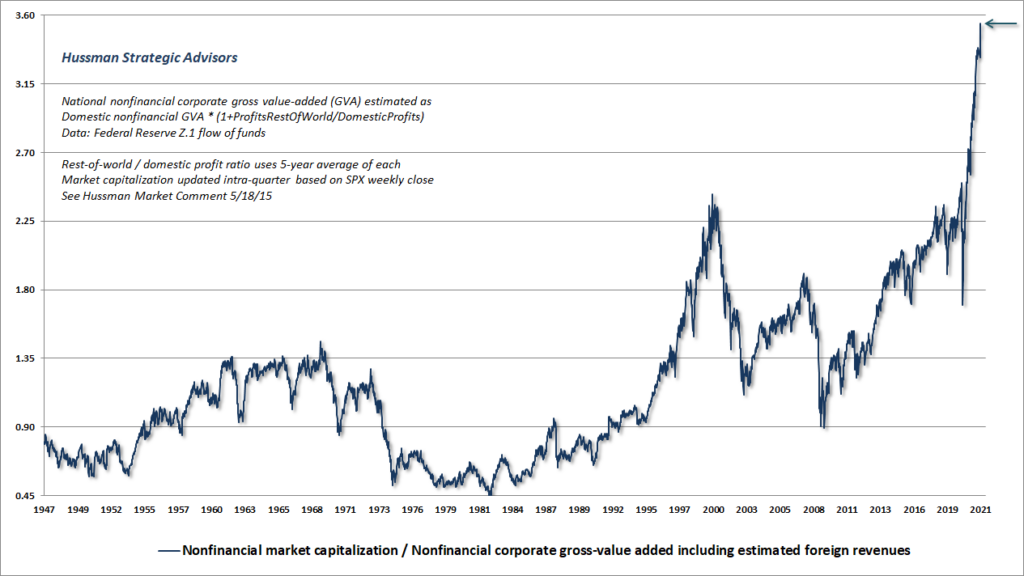

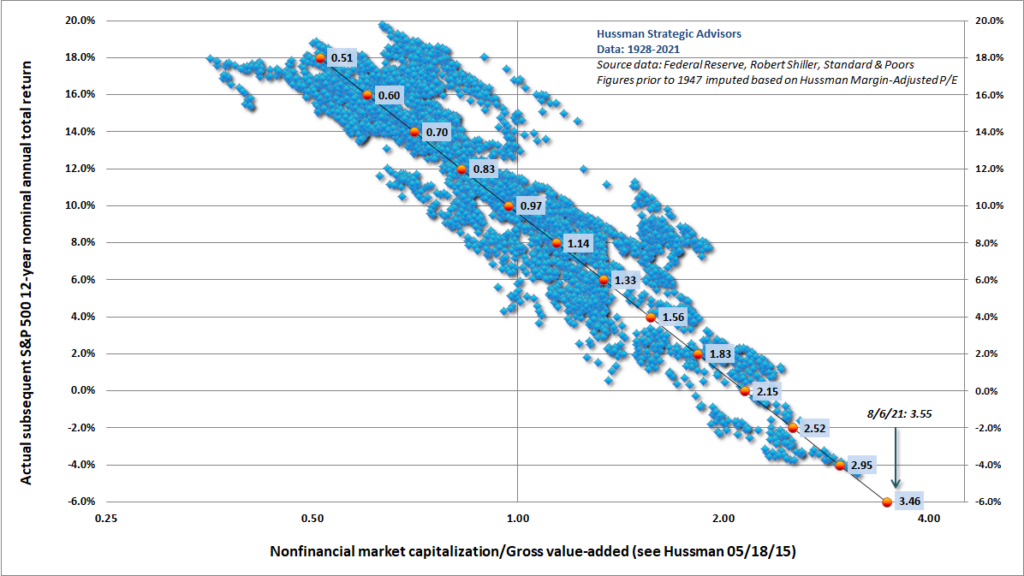

“The chart below shows the ratio of nonfinancial market capitalization to corporate gross value-added (MarketCap/GVA), which is the most reliable valuation measure based on its correlation with actual subsequent market returns across history. Notably, U.S. nonfinancial gross value-added is at a record high. The insanity you’re looking at is all numerator.” – John P. Hussman

There are many rationalizations suggesting high valuations don’t matter due to both rising inflation and low rates. However, as Hussman notes, valuations may be the first casualty of sustained inflation.

“Indeed, the S&P 500 has historically underperformed Treasury bills even when inflation is above 2% and higher than its level 6-months earlier. Valuations have never been materially above historical norms when CPI inflation was above 6%. So the “benefit” of high inflation would likely be offset by plunging valuations.“

Of course, high valuations historically precede long periods of low to negative returns.

“With MarketCap/GVA currently about 3.6 times its historical norm, it would take 22 years of 6% growth to offset that headwind.“

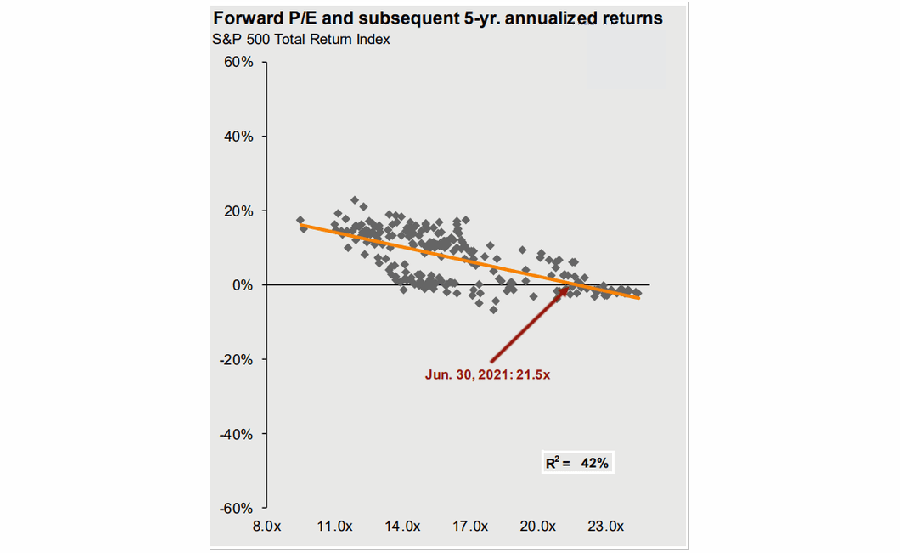

If you don’t like Dr. Hussman’s analysis, then J.P. Morgan also produced similar data based on “forward P/E” and subsequent 5-year annualized returns.

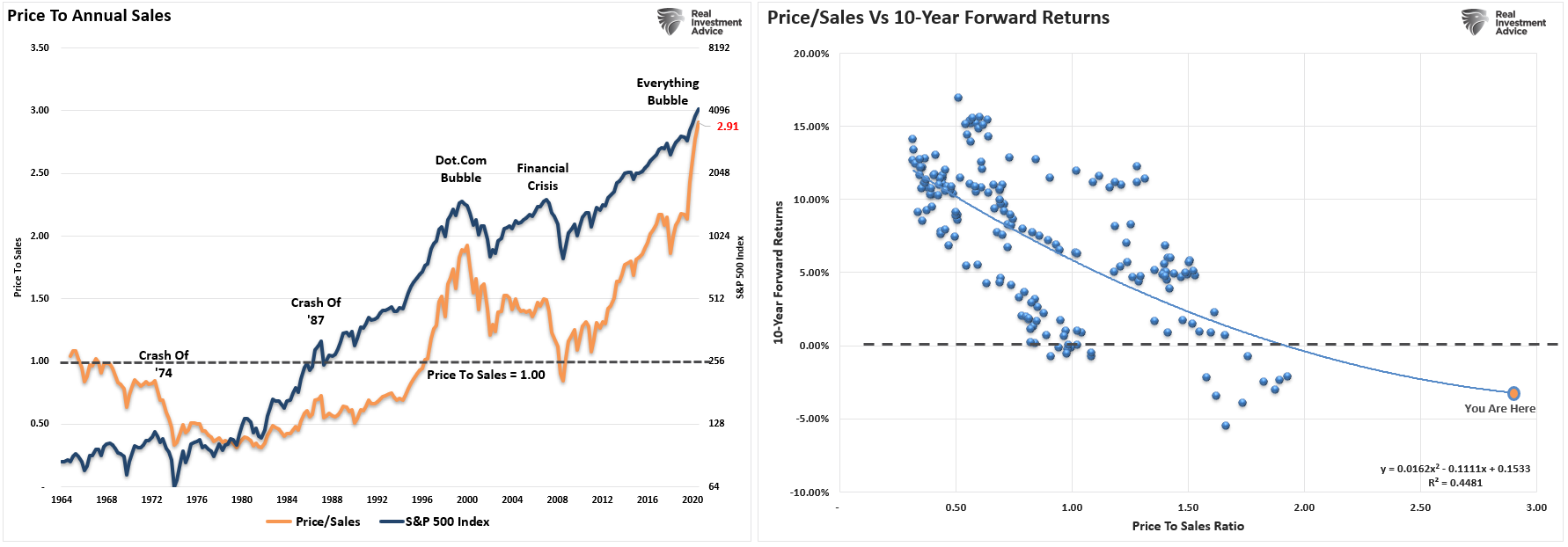

Even price-to-sales are predicting exceptionally low returns over the next decade.

“Currently, the price-to-sales (revenue) ratio is at the highest level ever. As shown, the historical correlation suggests outcomes for investors will not be kind.” – Real Investment Report

As an investor, do you bet on probabilities or possibilities?

Why You Should Choose Black

There is always a tremendous amount of bad advice put out to individual investors to promote a bullish bias. Here is a good example.

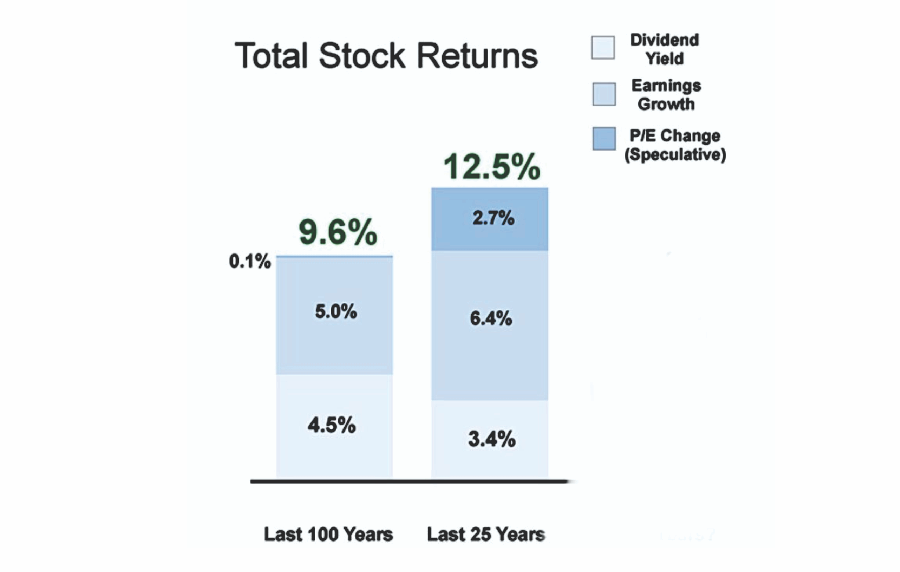

“Equity total return = DY + earnings growth + delta in P/E.

Over the last 100 years, DY has been 3-4% + earnings growth 5-6% on avg. Lower real yields support P/E. Not owning stocks long-term is like betting black for life at a roulette where most numbers are red.” – @macroalf

At first blush, such would appear to be a clear case as to why you should buy and hold an investment portfolio of stocks over the long term.

However, before you go betting on “red,” there are several considerations to be made.

- Cherry picked start dates can provide any result you want. 100-years ago was 1920. That was the beginning a major bull market cycle that lasted until 1929. However, back up 20-years to 1900, and an investor had to wait until the 1950s to breakeven.

- Starting 25-years ago was 1995. While the run from 1995-2000 was extremely strong, investors then spent the next 13-years going no where.

- Lastly, we don’t live forever. You can not invest for 100-years. Even 25-years is problematic for many as that is the bulk of their savings years before retirement.

Valuations matter over the long term. But, they matter most when it comes to “when” you start your investing journey.

In other words, with valuations at historically high levels, you may be better off betting on “black.”

Retail “Investor” Or “Speculator?”

In today’s market, the majority of investors are simply chasing performance. As stated, there is simply too much money chasing too few assets.

But, this isn’t “investing,” it’s “speculation.”

Think about it this way.

If you were playing a hand of poker and dealt a “pair of deuces,” would you go “all-in?”

Of course, not.

The reason is you intuitively understand the other factors “at play.” Even a cursory understanding of the game of poker suggests other players at the table are probably holding better hands, which will lead to a rapid reduction of your wealth.

Ultimately, investing is about managing the risks that will substantially reduce your ability to “stay in the game long enough” to “win.”

Robert Hagstrom, CFA penned a piece discussing the differences between investing and speculation:

“Philip Carret, who wrote The Art of Speculation (1930), believed “motive” was the test for determining the difference between investment and speculation. Carret connected the investor to the economics of the business and the speculator to price. ‘Speculation,’ wrote Carret, ‘may be defined as the purchase or sale of securities or commodities in expectation of profiting by fluctuations in their prices.’”

Chasing markets is the purest form of speculation. It is just a bet on prices going higher than determining if the price paid for those assets is a discount to fair value.

Graham & Dodd

Along with David Dodd, Benjamin Graham attempted a precise definition of investing and speculation in their seminal work Security Analysis (1934).

“An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

There is also an essential passage in Graham’s The Intelligent Investor:

“The distinction between investment and speculation in common stocks has always been a useful one and its disappearance is a cause for concern. We have often said that Wall Street as an institution would be well advised to reinstate this distinction and to emphasize it in all its dealings with the public. Otherwise the stock exchanges may some day be blamed for heavy speculative losses, which those who suffered them had not been properly warned against.”

Surviving The Game

Regardless of whether you believe fundamentals will ever matter again is irrelevant. What is essential is that periods of excess speculation always end the same way.

If you are one of our younger readers, who have never been through an actual “bear market,” I wouldn’t believe what I am telling you either.

However, after living through the Crash of ’87, managing money through 2000 and 2008, and navigating the “Great Crash of 2020,” I can tell you the signs are all there.

A real bear market will happen. When? I don’t have a clue.

But it will be an unexpected, exogenous event that triggers the selling.

It always appears easiest at the top. At the bottom, retail investors will not want to buy.

Historically, the environment we are living in currently has not worked out well for investors. However, in the short term, the “irrationality” will last long enough to convince you “this time is different.”

“History doesn’t always repeat itself, but it often rhymes.” – Samuel Clemens

The post Technically Speaking: “Pet Rocks” & Other Signs Of A Rich Market appeared first on RIA.