On Monday, stocks took a beating from rising trade tensions as China put the brakes on imports of agricultural products following Trumps latest tariff threat. As noted by the WSJ:

“So much for a trade deal any time soon.

Monday’s pain for U.S. investors was foretold late Sunday evening. The Chinese yuan sank below 7 per dollar and hit an all-time low in offshore trading Monday with local officials blaming the depreciation on President Trump’s decision last week to extend tariffs to almost all Chinese imports. Mr. Trump responded on Twitter, accusing China of engaging in currency manipulation.

The result was a mess across global markets. The Dow Jones Industrial Average fell 766 points while the S&P 500 and Nasdaq Composite fell about 3% and 3.5%, respectively.”

Before we get into the charts, let me just remind you what we have been saying about Trump’s “trade war” for more than year now:

“China has a long history of repeatedly reneging on promises it has made to past administrations.

By agreeing to a reduction of the “deficit” in exchange for “no tariffs,” China removed the most important threat to their economy as it will take 18-24 months before the current Administration realizes the problem.”

“The U.S.- China confrontation will be a war of attrition: while China has shown a willingness to make a deal on shrinking its trade surplus with the U.S., it has made clear it won’t bow to demands to abandon its industrial policy aimed at dominating the technology of the future.”

- China is playing a very long game. Short-term economic pain can be met with ever-increasing levels of government stimulus. The U.S. has no such mechanism currently, but explains why both Trump and Vice-President Pence have been suggesting the Fed restarts QE and cuts rates by 1%.

- The pressure is on the Trump Administration to conclude a “deal,” not on China. Trump needs a deal done before the 2020 election cycle AND he needs the markets and economy to be strong. If the markets and economy weaken because of tariffs, which are a tax on domestic consumers and corporate profits, as they did in 2018, the risk off electoral losses rise. China knows this and are willing to “wait it out” to get a better deal.

- China is not going to jeopardize its 50 to 100-year economic growth plan on a current President who will be out of office within the next 5-years at most. It is unlikely as the next President will take the same hard-line approach on China that President Trump has, so agreeing to something that won’t be supported in the future is doubtful.”

“China has been attacking the “rust-belt” states, which are crucial to Trump’s 2020 re-election, states with specifically targeted tariffs. (Now accelerated with the decision to stop imports altogether.)

While Trump is operating from a view that was a ghost-written, former best-seller, in the U.S. popular press, XI is operating from a centuries-old blueprint for victory in battle.”

There were many more articles in between, but you get the idea.

This has always been a war Trump can’t win. China’s ability to take a tremendous amount of short-term pain for a long-term gain will be more than President Trump counted on when he thought “trade wars are easy to win.” They aren’t, and the economic pain will likely be more than he bargained for.

The markets are beginning to sense this as well, particularly as the White House escalates the situation by labeling China a “currency manipulator.”

In the short-term, traders are now turning their focus back to the Federal Reserve for help. More rate cuts, however, are not likely going to be enough to solve the pressure to corporate profits, which will accelerate as the trade war escalates.

Technical Update

Over the past couple of week’s, we have been talking about a potential correction. While the media was quick to jump on Trump’s “China threats” as the reason for the selloff, those actions were just the “catalyst that lit the fuse.”

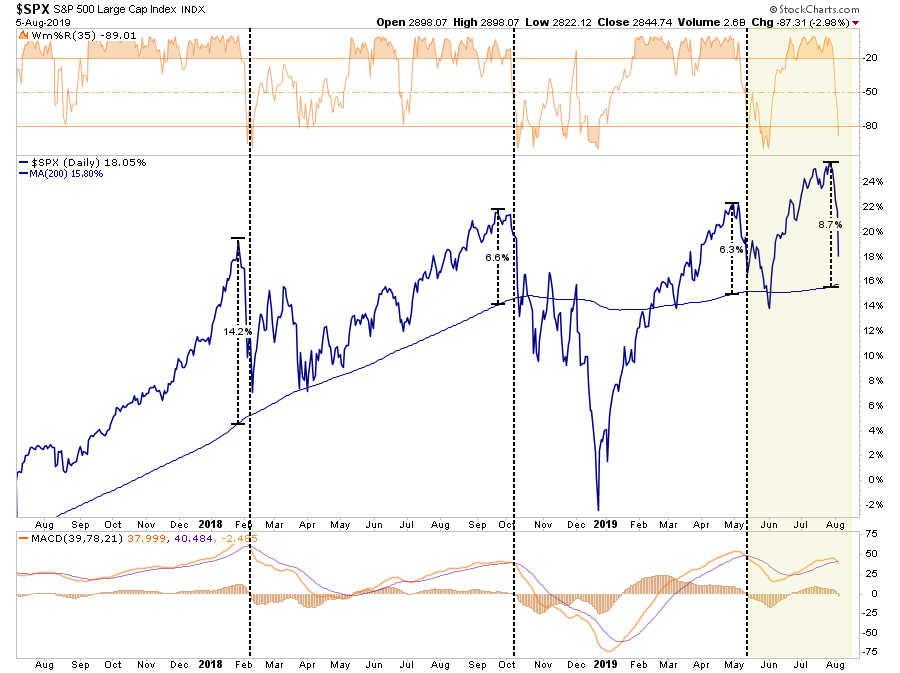

“[Over the last two weeks] the market is rallying in anticipation of more Central Bank easing. The markets are momentarily detached from weaker earnings growth, weaker economic growth, and a variety of other market-related risks.

In the very short-term, the market is grossly extended and in need of some correction action to return the market to a more normal state. As shown below, while the market is on a near-term “buy signal” (lower panel) the overbought condition, and near 9% extension above the 200-dma, suggests a pullback is in order.”

Chart Updated Through Monday

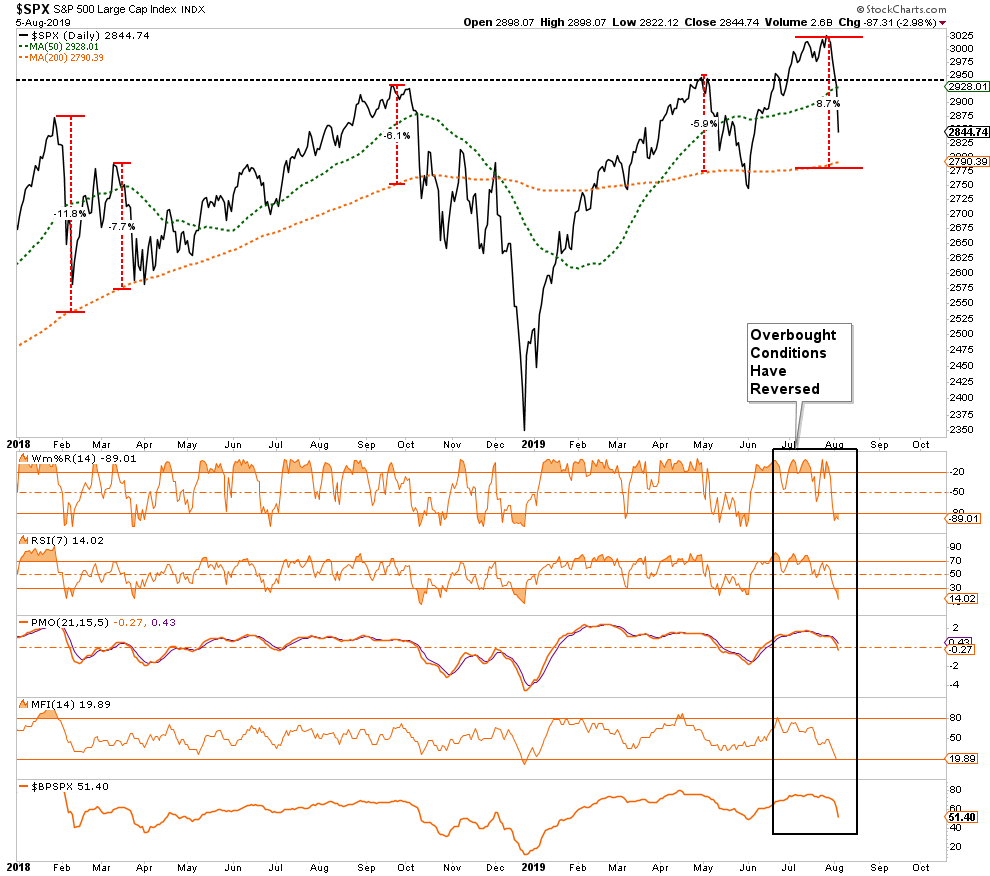

We had also warned previously the current extension of the market, combined with overbought conditions, was due for a reversal.

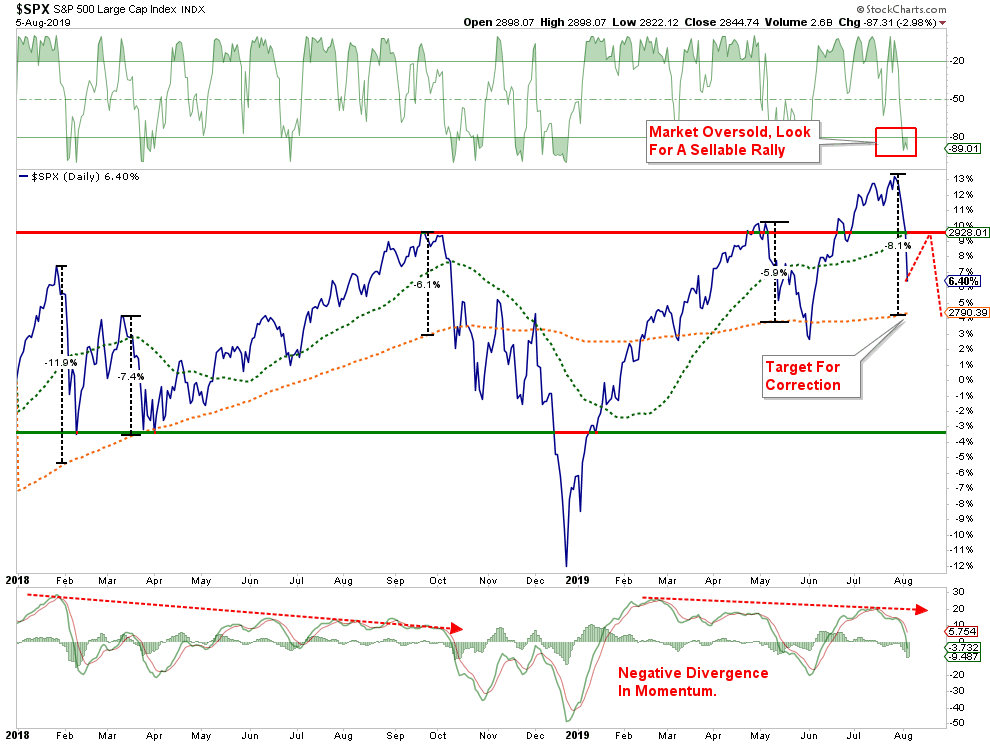

On a very short-term basis the market has reversed the previously overbought condition to oversold. This could very well provide a short-term “sellable bounce” in the market back to the 50-dma. As shown in the chart below, any rally should be used to reduce portfolio risk in the short-term as the test of the 200-dma is highly probable.

(We are not ruling out the possibility the market could decline directly to the 200-dma. However, the spike in volatility and surge in negative sentiment suggests a bounce is likely first.)

As I noted in this past weekend’s newsletter, we have been taking actions within our portfolios to prepare for this correction and sharing those actions with our RIAPRO subscribers (30-Day Free Trial).

July 22nd Portfolio Update: This morning action was taken and we took profits on 10% of 11 of our equity holdings. All of these positions had gains in excess of 20% since January 1st.

Those actions played well with the S&P declining by roughly -3.00% on Monday as our Equity and ETF portfolios only declined by –0.93% and –1.04% respectively.

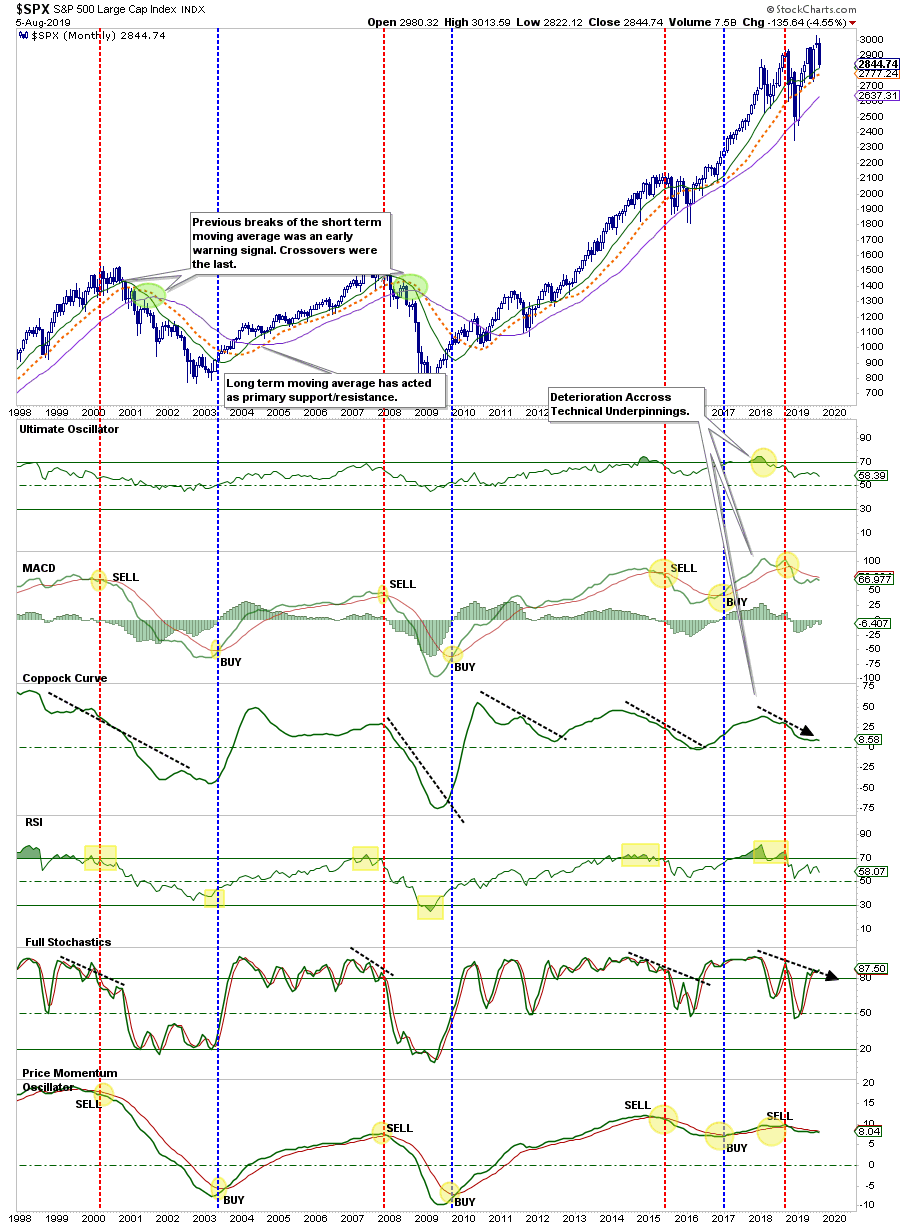

Monthly Signals Remain Bearish

Given that monthly data is very slow-moving, longer-term signals can uncover changes to the trend which short-term market rallies tend to obfuscate.

Interestingly, despite recent “all-time” highs in the S&P 500, the monthly signal have all aligned to “confirm” a “sell signal.” Since 1950, such an alignment has been somewhat of a rarity. The risk of ignoring the longer-term signal currently is that it may be signaling a more important topping process remains intact.

The technical signals, which do indeed lag short-term turns in the market, have not confirmed the bullish attitude. Rather, and as shown in the chart above, the negative divergence of the indicators from the market should actually raise some concerns over longer-term capital preservation.

What This Means And Doesn’t Mean

What this analysis DOES NOT mean is that you should “sell everything” and “hide in cash.”

As always, long-term portfolio management is about “tweaking” things over time.

At a poker table, if you have a “so so” hand, you bet less or fold. It doesn’t mean you get up and leave the table altogether.

What this analysis DOES MEAN is that we need to use any short-term rally over the next few days to take some actions to rebalance “risks.”

1) Trim Winning Positions back to their original portfolio weightings. (ie. Take profits)

2) Sell Those Positions That Aren’t Working. If they don’t rally with the market during a bounce, they are going to decline more when the market sells off again.

3) Move Trailing Stop Losses Up to new levels.

4) Review Your Portfolio Allocation Relative To Your Risk Tolerance. If you are aggressively weighted in equities at this point of the market cycle, you may want to try and recall how you felt during 2008. Raise cash levels and increase fixed income accordingly to reduce relative market exposure.

While I certainly expect the White House to “tweet” out a statement confirming “trade talks are still ongoing,” or comments from Fed Reserve officials that “more rate cuts are likely,” the damage to the economy from tariffs are already in the works. With both earnings and corporate profits under pressure, this may be the start of a bigger corrective process like we witnessed in 2018.

But, there is always the possibility that I am wrong and the markets turn around and rally back to all-time highs.

If that happens, and the bullish trend resumes, then we will adjust our allocation models up and take on more equity risk.

But as I have asked before, what is more important to you as an individual?

- Missing out temporarily on the initial stages of a longer-term advance, or;

- Spending time getting back to even, which is not the same as making money.

For the majority of investors, the recent rally has simply been just recovery of previous losses from 2018.

Currently, there is not a great deal of evidence supportive of a longer-term bull market cycle. The Fed cutting rates is “NOT” bullish, it actually correlates to much more negative long-term outcomes in the market.

If I am right, however, the preservation of capital during an ensuing market decline will provide a permanent portfolio advantage going forward. The true power of compounding is not found in “the winning,” but in the “not losing.”

This is a good time to review those trading rules:

“Opportunities are made up far easier than lost capital.” – Todd Harrison