by Michael Lebowitz and Jack Scott

Tesla’s Moonshot, How High Can It Go?

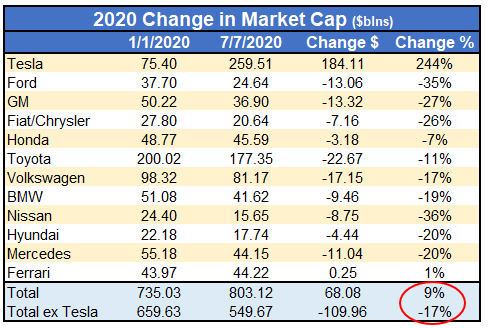

Since the beginning of 2020, the aggregate market cap of the twelve largest automakers is up 9.30% to $803 billion. Quite an increase considering the COVID pandemic is causing a global recession and weak auto sales.

The obvious question is, why is the auto sector doing so well amid such uncertainty?

It’s not!

The optics are “driven” by one stock, Tesla (TSLA). TSLA’s stock price continues its moonshot while other automakers languish. The gross divergence of fortunes in the industry is worth exploring.

As has always been the mandate of our articles, we look at data on auto sales, industry trends, and demographics to help you come to your conclusion about Tesla and the auto industry. This, in turn, allows you to assess Tesla better independently.

Auto Industry

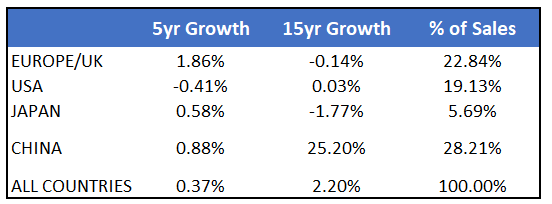

According to the International Organization of Motor Vehicle Manufacturers, global vehicle sales have grown annually at 0.37% over the last five years. Sales over the previous 15 years are quite a bit stronger at 2.20%.

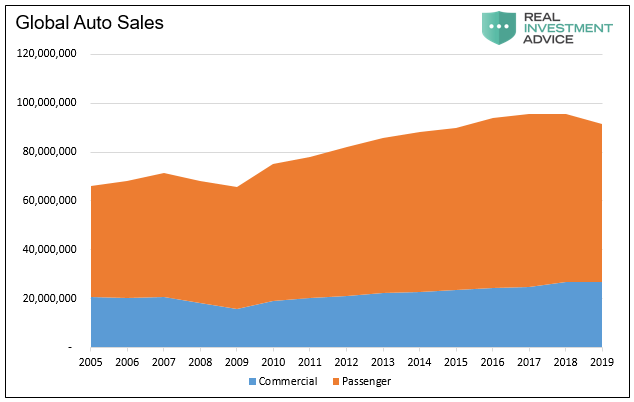

The graph below highlights total global auto sales broken down by passenger and commercial vehicles.

The following table shows growth rates and the percentage of global sales for the four largest auto markets.

Bottom line: auto sales over the last five years are tepid at best.

To put sales into a different context, it’s worth comparing them to economic activity. Over the last 15 years and five years, global GDP has grown annually 4.17% and 3.14%, respectively. Auto sales are not keeping up with global growth.

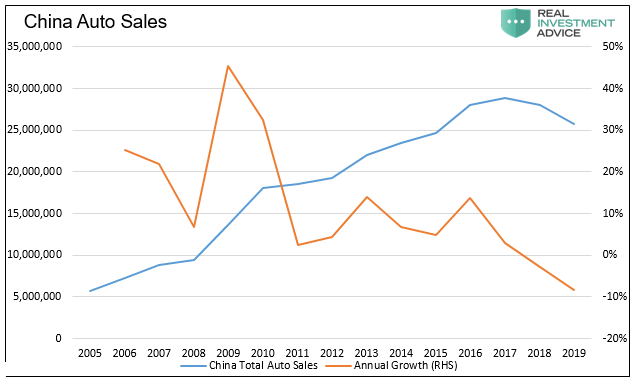

China has increased car ownership significantly and is the bright light for the industry. However, as shown below, sales of vehicles in China are leveling off. With China’s economic growth slowing considerably, and auto ownership more saturated, China’s appetite for autos will remain weak.

Without an obvious geographic region to replace China, the industry must rely on changes in consumer behaviors and preferences.

Demographics

Baby Boomers are retiring in droves and need fewer automobiles. Can the newest drivers, Millennials and Generation Z pick up the slack?

The Atlantic wrote an article in March 2012 entitled Why Don’t Young Americans Buy Cars? While the article is dated is still rings true. Here are some key quotes about the Millennial generation’s desire to buy cars:

Kids these days. They don’t get married. They don’t buy homes. And, much to the dismay of the world’s auto makers, they apparently don’t feel a deep and abiding urge to own a car.

The Times notes that less than half of potential drivers age 19 or younger had a license in 2008, down from nearly two-thirds in 1998. The fraction of 20-to-24-year-olds with a license has also dropped. And according to CNW research, adults between the ages of 21 and 34 buy just 27 percent of all new vehicles sold in America, a far cry from the peak of 38 percent in 1985.

At a major conference last year, Toyota USA President Jim Lentz offered up a fairly doleful summary of the industry’s challenge.

“We have to face the growing reality that today young people don’t seem to be as interested in cars as previous generations,” Lentz said. “Many young people care more about buying the latest smart phone or gaming console than getting their driver’s license.”

The next generation, Gen Z, currently aged 5-25 are starting to buy cars. As such, it is early to define Generation Z’s car buying preferences. However, they are being shown to be frugal with big-ticket items. Data shows that their buying habits are similar to the millennial generation. This seems to make sense given their existing student debt obligations and relatively low wages.

For an in-depth discussion of generational tendencies we highly recommend Generations and The Fourth Turning by Howe and Strauss (LINK).

Ridesharing

As if generational shifts are not enough trouble for the industry, ridesharing companies may be worse. Uber and Lyft make it easy to avoid car ownership.

What taxis did for car ownership in New York City, ride-sharing services are doing in many urban and suburban regions. (In Manhattan, less than a quarter of households own a car. That compares to an average of 1.88 vehicles per U.S. household.)

The cost/benefit analysis of owning a car has changed, and it’s not to the benefit of the auto manufacturers. Autonomous ridesharing services in the future will only make this problem more acute.

Why Are Valuations Rising?

The recent pace of car sales is weak and below economic trends. Global economics argues there is no clear replacement for China’s growth of years past. Demographics do not favor the industry. So, why is the aggregate value of auto companies rising during a recession?

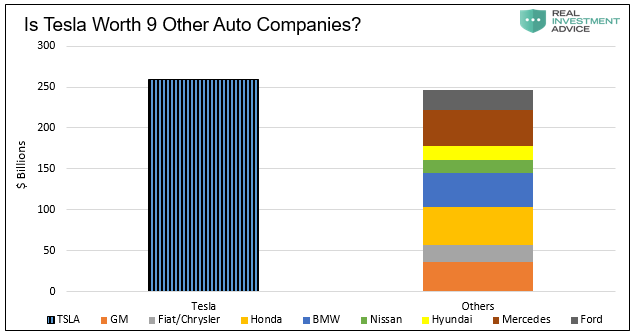

As shown below, Tesla’s market cap has risen 244% this year. The market cap of the industry, excluding Tesla, is down 17%.

The table leads to a straightforward question. Is Tesla becoming an automotive behemoth and leaving its competition in the dust?

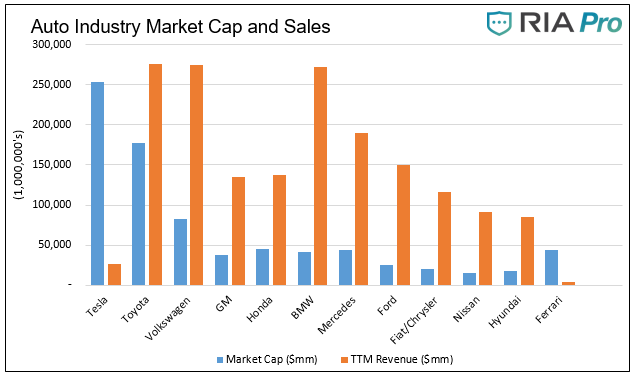

The graph below comparing sales and market cap puts context around that question.

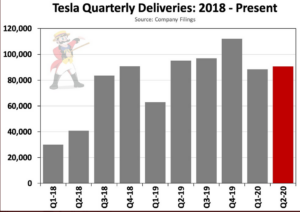

As shown, Tesla’s sales are a fraction of every other major manufacturer. By default, investors must think their future sales trajectory is enormous. Meanwhile, deliveries have been flat since the third quarter of 2018.

As shown, Tesla’s sales are a fraction of every other major manufacturer. By default, investors must think their future sales trajectory is enormous. Meanwhile, deliveries have been flat since the third quarter of 2018.

Courtesy @teslacharts

If Tesla shareholders are correct, Tesla must garner at least 25-30% of the market share.

Can TSLA justify the combined market cap of GM, Fiat/Chrysler, Honda, BMW, Nissan, Hyundai, Mercedes, and Ford? Before you answer, understand they currently make only about 2% of the cars as those other manufacturers.

Tesla’s Advantage… For Now

Tesla certainly has a valuable first starter advantage in the electric vehicle (EV) category. Notably, however, they do not have patents.

Its advantage exists because other manufacturers have been slow to release EV cars. The technology is easy to replicate. Whether they are waiting for costs to decline, longer battery life, persistently higher gas prices, or more robust demand, we don’t know. Nonetheless, the wait will not be much longer.

Most auto manufacturers have lines of EVs due out this year and next. Many will come at prices cheaper than those Tesla offers. Unlike Tesla, they offer their clients service shops and trade ins. Tesla’s first mover advantage is slipping away quickly.

For Tesla’s market cap to be correct, the following must be true:

- They must continue to dominate the EV space

- EVs must gain significantly in popularity

- Other manufacturers must be incapable of producing competitive EVs

That a tall order!

Summary – Momentum Rules

TSLA’s stock may run higher. We believe its stock price is in the grips of speculative fervor and passive investing momentum. These conditions may last longer.

We do not know when Tesla’s moonshot will end. However, as we learned in 2001, the end is unusually swift and vicious. Afterward, it can take years and even decades before an investor breaks even. Just consider it took Microsoft 15 years to regain the record highs of 2000. At that time, Microsoft had strong fundamentals and a dominant market position.

Tesla?

Not so much.