OK, let’s look at the Tesla magic briefly.

By Wolf Richter for WOLF STREET.

Tesla’s profit was all about Tesla’s pollution credits, or “regulatory credits,” as it calls them. These are tax credits that Tesla gets from governments and sells to other companies. There is no cost associated with them; they’re booked as revenues and flow through to profit. Tesla reported this evening that these regulatory credits jumped 40% in Q4 compared to the same period a year earlier, to $133 million.

Despite the surge in regulatory credits, net income fell 25% to $105 million. Without those credits Tesla would have lost $28 million.

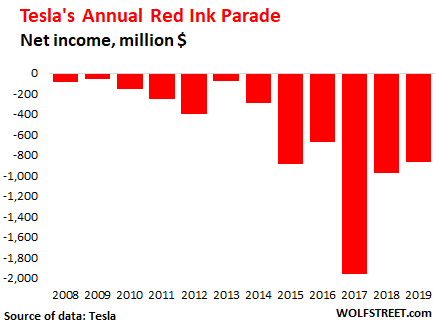

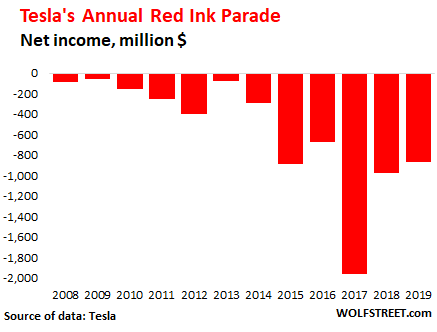

For the year 2019, Tesla reported a net loss of $862 million. This includes $594 million in regulatory credits. Without those credits, Tesla would have lost $1.5 billion. Tesla has been producing vast quantities of red ink since it started disclosing its financials in preparation for its IPO in 2010. From 2008 through 2019, Tesla lost money every single year with relentless insistence, and those net losses over those 12 years combined now amount to $6.7 billion:

And Tesla has a revenue problem.

Revenues inched up 2.2% to $7.38 billion in Q4. Automotive revenues alone edged up just 0.7% to $6.37 billion. And gross profit fell 3.6% to $1.39 billion. This is not the hallmark of a growth company. This is the hallmark of stagnation.

But here is why this is happening: Tesla is going downscale, going from luxury to high-end mass-market, while everyone else in the industry is trying to do the opposite, go upscale.

Global deliveries in Q4 of its less expensive Model 3 have surged 47% year-over-year to 62,620 vehicles. But deliveries of its high-dollar models (which sell for twice as much or more than the Model 3) have collapsed by 29% to 19,475 vehicles.

In other words, just to stay even, Tesla has to sell three $35,000-Model 3s for each $105,000-Model S or X that it doesn’t sell.

After waves of layoffs, operating expenses under control

In 2019, Tesla went through waves of layoffs, particularly in the US, and it has scaled back in other areas. The result is that operating expenses have remained flat in Q4 at $1.03 billion.

Constant need to raise cash: $4.3 billion in 2019

In May 2019, Tesla raised $2.7 billion in a sale of shares and convertible bonds.

In addition, in December 2019, it entered into a loan agreement with a consortium of state-owned Chinese lenders for loans totaling $1.63 billion to fund the construction of its factory in Shanghai, the purchase and installation of equipment in the factory, and working capital to run the factory and pay the workers. Part of this loan package replaced a bridge-loan from those state-owned lenders that Tesla had obtained earlier in 2019.

This $4.3 billion in new cash came in handy on its balance sheet where its cash balance rose by $2.5 billion over the 12-month period to $6.2 billion. So it won’t run short on cash for a while.

Tesla’s debt has now swollen to $13.4 billion ($11.6 billion long-term and $1.8 billion short-term debt)

How much should Tesla be worth, if it ever makes a big profit?

In terms of earnings per share, Tesla’s annual net loss translates into EPS of -$4.92. So if Tesla is ever able to make an annual net income of $862 million – a swing of $1.7 billion – it would have EPS of about +$4.92. Now, this assumes that Tesla doesn’t sell any shares or hand out any shares to executives in their compensation packages, which would dilute EPS. So let’s assume the share-count stays the same for once.

In that glorious future year where Tesla makes $4.92 a share, instead of losing $4.92 a share, what would it be worth, as an automaker in a stagnant saturated industry? At a PE ratio of 20 (giving Tesla the benefit of all doubts), its shares on that glorious day in the future when it finally has an annual EPS of $4.92, the stock would still be richly priced at 20 x $4.92, giving it a share price of $98.40.

Just to point out how crazy this has gotten: This evening – upon the announcement of 2% revenue growth and a 25% plunge in quarterly net income despite $133 million in regulatory credits, and of an annual loss of $862 million – Tesla’s shares spiked nearly 12% to $648.