By John Mauldin

The global economy is slowing.

Germany, for instance, may already be in recession. GDP there dropped 0.1% in this year’s second quarter, with little reason to expect better from Q3 which we will learn soon.

Whatever you call it, Germany is certainly not in a good spot. It is highly dependent on exports which, for various reasons, are weakening, particularly in their auto industry.

Meanwhile, Brexit (depending on how it ends) could greatly reduce UK purchasesof German goods.

On top of that, uncertainties induced by President Trump’s trade war are deterring businesses in Europe (as well as here) from investing in future growth projects.

And overarching all of it is the technology-driven decline in globalized manufacturing.

If Germany’s “technical recession” morphs into a real recession, the rest of Europe will certainly follow. And recession in Europe—and the measures its central banks will take to fight it—won’t leave the US economy unscathed.

The Rest of the World Is Not Well

Not coincidentally, commodity-producing emerging markets are also experiencing difficulty. Ditto for some more advanced commodity exporters like Australia and Canada.

Their problem springs from lower commodity prices, but more specifically from China. My friend Sam Rines (Director and Chief Economist at Avalon Advisors) explored this in a recent note.

Much of the commodity price pressure can be blamed on slowing Chinese growth, but that is not the entire story. China is roughly 20% of global GDP on a PPP basis, and constitutes much of the incremental growth in the global economy. When China’s growth slows, the ripples are felt in many places.

Commodity prices and China’s growth rate are understandably intertwined, and that may be a difficult correlation to break down. Why? It is difficult to pinpoint the next major tailwind. And—even when speculating on the next tailwind—timing is a further difficult hurdle to overcome.

But why not try. Of the three major headwinds to commodity pricing in the post-dual stimuli world (end of China’s building spree, US dollar following QE, and slower overall global growth), the US dollar is the most likely to abate as a headwind in the near-term. Global growth is dependent largely on US and China trade policy, but there could be a marginal shift higher in growth (the worst might be over). Replacing the rapid growth of China is not easy to see. India is gaining share of global GDP. But it is not easy to see the path to a full replacement of the China commodity cycle.

We may soon see the other side of China’s growth story. Just as it had an outsized effect on global GDP on the way up, it will likely be a major drag on the way down.

Note, when my young friend Sam says “the worst may be over,” he is talking in particular about the downturn from slower Chinese growth. If you read his daily missives, as I do, he is far from predicting a US recession.

Slower growth? Yes. It sounds like he thinks we are in a slower muddle-through world for the next few quarters at least. And maybe through the next elections…

The Signs of Looming Recession

While more goods are delivered electronically and supply chains are shrinking, the movement of physical goods is still the economy’s circulatory system.

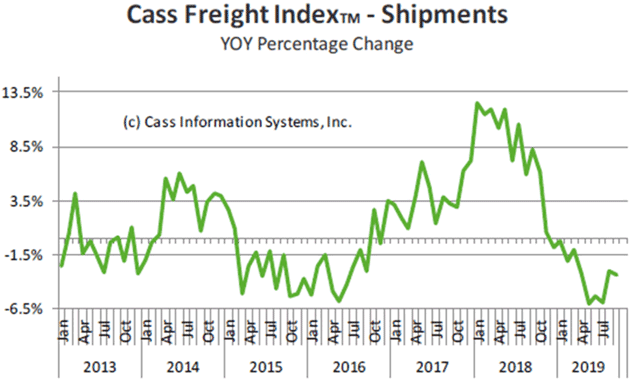

The Cass Freight Index is the most comprehensive, high-frequency indicator of this. It tends to lead the economy by a few quarters but has signaled almost every economic turning point.

So the fact its year-over-year change has been negative every single month since December 2018 is more than a little concerning.

As you can see from the chart below, there have been periods of negative growth without a recession, but the latest drop’s sheer magnitude and rapidity is eye-opening.

Freight traffic is falling, and it looks even worse when Cass digs into the specifics.

Going deeper, Cass notes that “dry van” truck volume is a fairly reliable predictor for retail sales and is still relatively healthy.

That fits what we see elsewhere about consumer spending sustaining growth. But they also note that seasonally, dry van volume should be even stronger than it is. That suggests caution as the year winds down.

Other transport modes—rail, flatbed trucks, chemical tankers—indicate real problems in the industrial economy. Manufacturers seem to have little faith consumers will keep buying at the rates they are.

And, given how much consumer spending is debt-financed, they’re probably right to be cautious. Strong retail spending is not necessarily positive. Consider this Comscore holiday spending report from November 2007.

The Friday after Thanksgiving is known for heavy spending in retail stores, but it’s clear that consumers are increasingly turning to the Internet to make their holiday purchases,” said Comscore Chairman Gian Fulgoni. “Online spending on Black Friday has historically represented an early indicator of how the rest of the season will shake out. That the 22-percent growth rate versus last year is outpacing the overall growth rate for the first three weeks of the season should be seen as a sign of positive momentum.

The Great Recession began one month after this “sign of positive momentum.” A strong holiday shopping season won’t mean we are out of the woods and could mean we are just entering them.

I predict an unprecedented crisis that will lead to the biggest wipeout of wealth in history. And most investors are completely unaware of the pressure building right now. Learn more here.