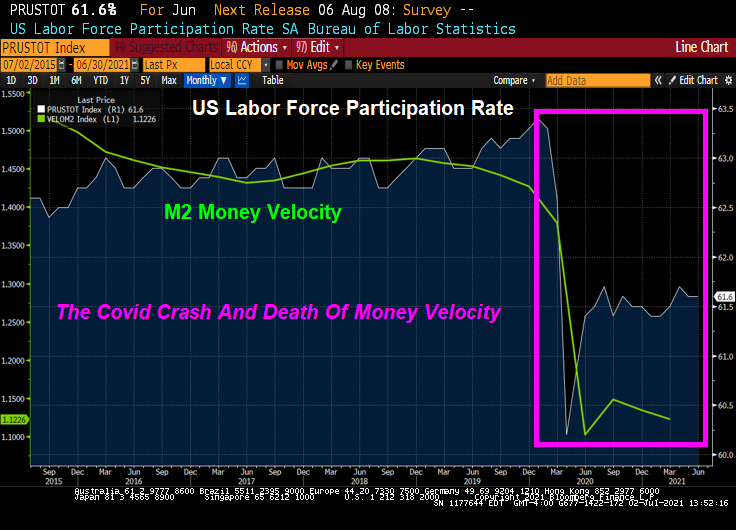

Today’s jobs reports showed that labor force participation did not improve since May and remain substantially below pre-Covid levels.

Over the longer term, we can see that M2 Money Velocity peaked around the same time that US labor force participant peaked (1997). And it has been downhill since 1997 with Covid accelerating the decline.

So, it is not just Covid that is killing money velocity and labor force participation. I wonder if The Gramm–Leach–Bliley Act (GLBA), also known as the Financial Services Modernization Act of 1999, had anything to do with M2 Velocity getting crushed?

Nothing has been the same since The Clinton Administration and 1997.