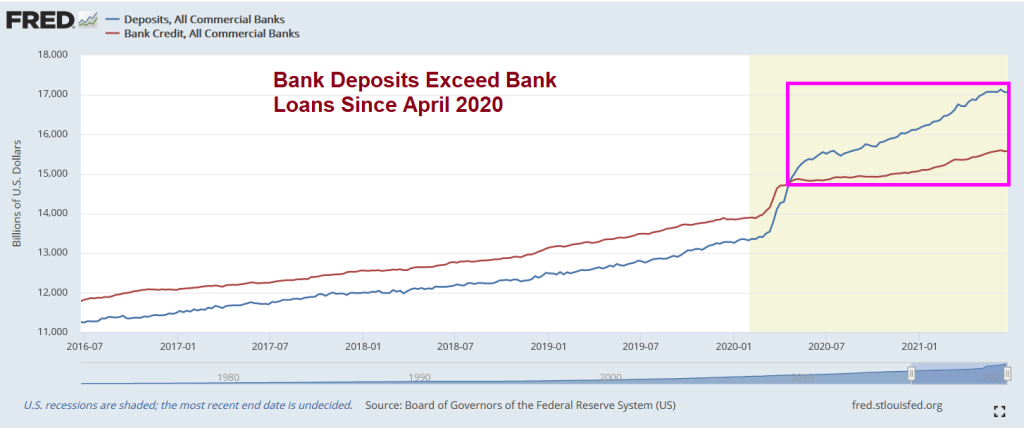

Typically, banks make money by taking deposits at low rates and lending to borrowers at higher rates (car loans, residential mortgages, business loans, etc.), earning a spread. And bank deposits are usually less than the loans that they extended. Until April 2020. Nothing has been the same since Covid.

This is really a unique time, since during the last recessions (2001 and The Great Recession) bank credit exceeded bank deposits.

Banks can turn to The Federal Reserve at times like these. The Fed’s reverse repo program lets eligible firms, like banks and money-market mutual-funds, park large amounts of cash overnight at the Fed, at a time when short-term funding rates have fallen to next to nothing, and finding a home for cash has become harder.

But we are seeing a temporary decline in overnight reverse repo agreements.

In other words, there is too much cash in the system. And Credit Suisse’s Zoltan Pozsar calculates that we’re looking at $2 TRILLION of flow into Reverse Repos by the end of August.

We shall see if The Federal Reserve ever leaves markets with the effective Fed Funds rate at 8 basis points and The Fed’s balance sheet at over $8 TRILLION. Now, THAT’S a lot of cash in the system.