“During the last year, the Federal Reserve has hinted that the period of ‘ultra-accommodative monetary policy’ was coming to an end. The Fed started that process last October by terminating the latest ‘Quantitative Easing’ program, which induced massive amounts of liquidity into the financial markets. Subsequently, the Fed has turned its focus towards the near ZERO level of the ‘Fed Funds’ rate.” – July 6, 2015

It seems like an eternity ago now, but I warned then the Fed was too late in the cycle to tighten monetary policy due to the impact higher rates have on economic growth.

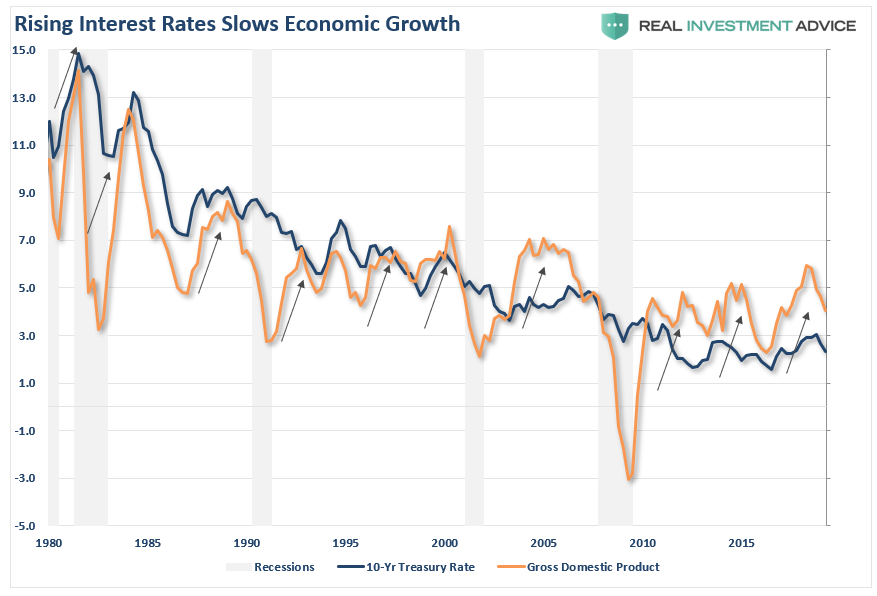

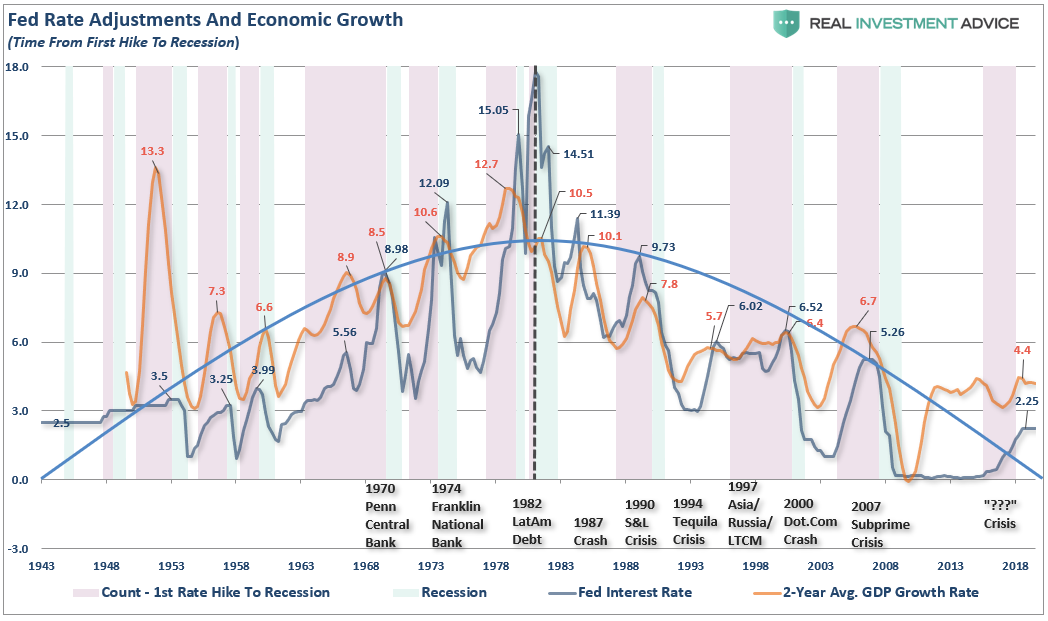

“While the Federal Reserve hopes that they can effectively raise interest rates without cratering economic growth, the problem is that the bond market may have already beaten them to the punch.

While I do not expect Treasury rates to rise very much, the increase in borrowing costs in an already weak economic environment has an almost immediate impact. The chart below shows the periods in history where Treasury rates have risen and the impact of subsequent rates of economic growth.”

As we suggested, the rise in rates to 3.25% was all the economy could withstand at the time.

I followed up that previous analysis in October 2015 suggesting the Fed had missed its window to hike rates. To wit:

“The problem for the Federal Reserve is that getting caught in a liquidity trap was not an unforeseen outcome of monetary policy, but rather an inevitable conclusion. The current low levels of inflation, interest rates, and economic growth are the result of more than 30-years of misguided monetary policies that have led to a continued misallocation of capital.”

“From our cyclical vantage point, we have long been aware of the truism that ‘recessions kill inflation.’ Therefore, when the next recession arrives, it is more likely to push inflation below zero at a time when the Fed has no obvious policy response. The resulting deflation will be the stuff of policy nightmares.”

Why am I reminding you of this?

It is becomingly increasingly clear from a variety of inputs that deflationary pressures are mounting in the economy. Recent declines in manufacturing, and production reports, along with the collapse in commodity prices, all suggest that something is amiss in the production side of the economy.

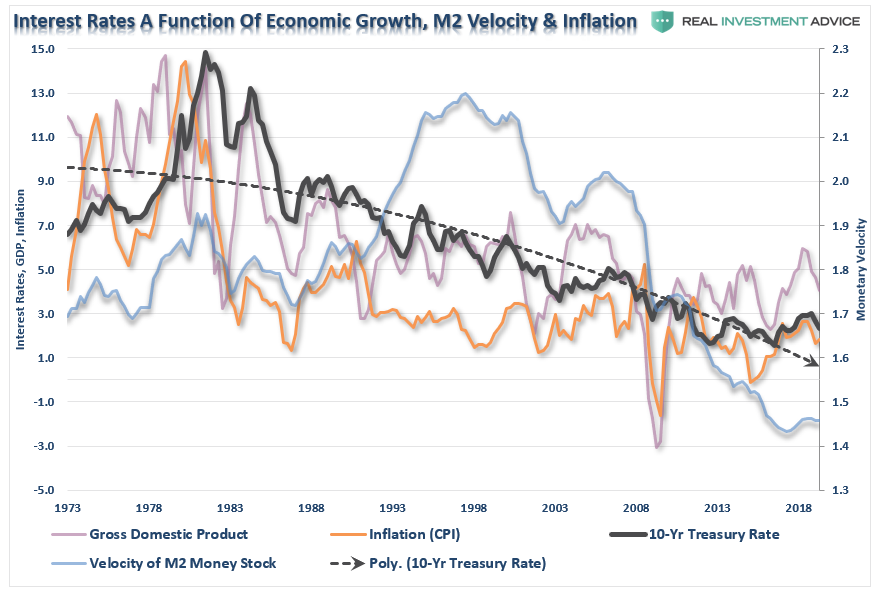

As shown in the chart below, the Fed should have started lifting rates as the spike in economic growth occurred in 2010-2011 as both the Fed and Government flooded the economy with liquidity. While hiking rates would have slowed the advance in the financial markets, the excess liquidity sloshing around the system would have offset tighter monetary policy.

If they had hiked rates sooner, interest rates on the short-end of would have risen giving the Fed a policy tool to combat economic weakness with in the future. However, assuming a historically normal response to economic recoveries, the yield curve has been negative for quite some time. This explains why “financial conditions” remain at historically low levels despite higher Fed Funds rates.

The chart above also explains the delay in the “yield curve” turning negative earlier in this cycle.

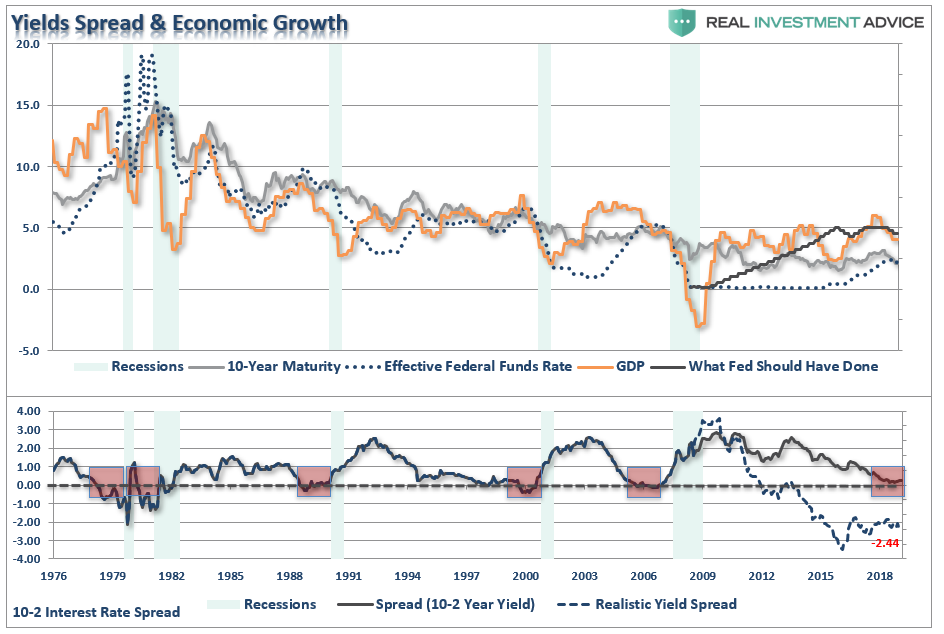

- As shown in the chart above, the 2-year Treasury has a very close relationship with the Effective Fed Funds Rate. Historically, the Federal Reserve began to lift rates shortly after economic growth turned higher. Post-2000 the Fed lagged in raising rates which led to the real estate bubble / financial crisis. Since 2009, the Fed has held rates at the lowest level in history artificially suppressing the short-end of the curve.

- The artificial suppression of shorter-term rates has skewed the effectiveness of the yield curve as a recession indicator.

- Lastly, negative yield spreads have historically occurred well before the onset of a recession. Despite their early warnings, market participants, Wall Street, and even the Fed came up with excuses each time to why “it was different.” Historically, it has never been the case.

However, the Fed is now trapped in a difficult position and is making a “policy mistake” once again.

Given the Fed waiting so long into the economic cycle to hike rates to begin with, they weren’t able to gain much of a spread before the economy was negatively impacted. There have been absolutely ZERO times in history when the Federal Reserve began an interest-rate hiking campaign that did not eventually lead to a negative outcome. To wit:

While the Federal Reserve clearly should not raise rates in the current environment, there is a possibility they will, regardless of the outcome.

The Fed understands that economic cycles do not last forever, and we are closer to the next recession than not. While raising rates would likely accelerate a potential slowdown and a significant market correction, from the Fed’s perspective, it might be the ‘lesser of two evils. Being caught at the ‘zero bound’ at the onset of a recession leaves few options for the Federal Reserve to stabilize an economic decline.”

The problem for the Fed is that the bond market was NEVER worried about inflation.

Only the Fed saw an “inflation-monster under the bed.” All the bond market needed was the Fed to come out and indicate a “shift” in their stance to worrying about “deflation” to seal the deal.

Despite the many arguments to the contrary, we have repeatedly stated that the rise in interest rates was a temporary phenomenon as “rates impact real economic activity.”

The “real economy,” due to a surge in debt-financed activity, was not nearly strong enough to withstand substantially higher rates. Of course, such has become readily apparent in the recent housing and auto sales data. Consequently, the Fed was unable to gain much clearance between the current level of rates and the “zero-bound.”

Navarro’s Naivety

On Tuesday, Peter Navarro, who is the White House trade advisor, called on the Federal Reserve to lower rates.

“The Federal Reserve before the end of the year has to lower interest rates by at least another 75 basis points or 100 basis points to bring interest rates here in America in line with the rest of the world. We have just too big a spread between our rates and that costs us jobs.’

While Peter, and President Trump, both want an “aggressive rate-cutting cycle” to sustain economic growth while he fights an unwinnable “trade war,” the reality is that rate cuts, and even additional measures of quantitative easing, or Q.E., are likely to have a muted effect. As I explained previously,the effectiveness of QE, and zero interest rates, is based upon the point at which you apply the stimulus.

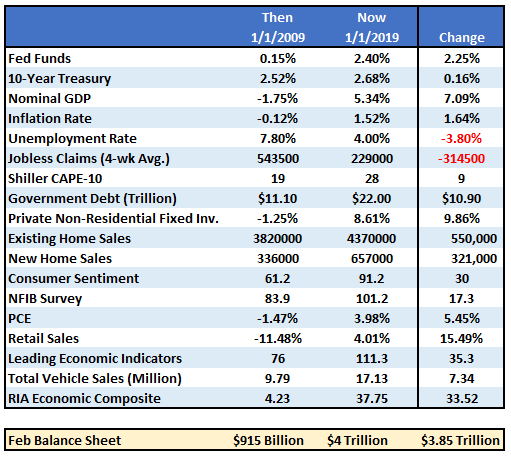

“In 2008, when the Fed launched into their “accommodative policy” emergency strategy to bail out the financial markets, the Fed’s balance sheet was only about $915 Billion. The Fed Funds rate was at 4.2%.

If the market fell into a recession tomorrow, the Fed would be starting with roughly a $4 Trillion balance sheet with interest rates 2% lower than they were in 2009. In other words, the ability of the Fed to ‘bailout’ the markets today, is much more limited than it was in 2008. But there is more to the story than just the Fed’s balance sheet and funds rate. The entire backdrop is completely reversed. The table below compares a variety of financial and economic factors from 2009 to the present.”

“The critical point here is that QE and rate reductions have the MOST effect when the economy, markets, and investors have been ‘blown out,’ deviations from the ‘norm’ are negatively extended, confidence is hugely negative.

In other words, there is nowhere to go but up.”

A simple analogy is throwing gasoline on a raging bonfire. The fire will burn for a bit longer, but it won’t burn any hotter. However, throwing gasoline on a pile of dry wood and hitting it with a match provides a better outcome.

Such was the case in 2009. Even without Federal Reserve interventions, it is highly probable the economy would have begun a recovery as the normal economic cycle took hold. No, the recovery would not have been as strong, and asset prices would be about half of where they are today, but an improvement would have happened nonetheless.

The extremely negative environment that existed, particularly in the asset markets, provided a fertile starting point for monetary interventions. Today, as shown in the table above, the economic and fundamental backdrop could not be more diametrically opposed.

This suggests that the Fed’s ability to stem the decline of the next recession, or offset a financial shock to the economy from falling asset prices, may be much more limited than the Fed, and most investors, currently believe.

The Fed has a long history of making policy mistakes which have led to negative outcomes, crisis, bear markets, and recessions.

As I showed, above, the Fed made a mistake not using the flood of liquidity to lift rates. Instead, the Fed opted to create an asset bubble instead. Or, should I say, “again.”

While another $2-4 Trillion in QE, and a return to the “zero bound,” might indeed be successful in further inflating asset prices, there is a finite ability to continue to pull forward future consumption to stimulate economic activity. In other words, there are only so many autos, houses, etc., which can be purchased within a given cycle.

Currently, there is evidence the cycle peak has been reached.

If I am correct, and the effectiveness of rate reductions and QE are diminished due to the reasons detailed herein, the subsequent destruction to the “wealth effect” will be far larger than currently imagined. There is a limit to just how many bonds the Federal Reserve can buy and a deep recession will likely find the Fed powerless to offset much of the negative effects.

If more “accommodation” works, great.

But as investors, with our retirement savings at risk, what if it doesn’t?