Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Instead of “bubble” or “collapse,” it uses “valuation pressures” and “broad adjustment in prices.” Business debt, not consumer debt, is the bogeyman this time.

Preventing another financial crisis – or “promoting financial stability,” as the Federal Reserve Board of Governors calls it – isn’t the new third mandate of the Fed, but a “key element” in meeting its dual mandate of full employment and price stability, according to the Fed’s first Financial Stability Report.

“As we saw in the 2007–09 financial crisis, in an unstable financial system, adverse events are more likely to result in severe financial stress and disrupt the flow of credit, leading to high unemployment and great financial hardship.”

Financial firms are OK-ish, except for hedge funds.

The largest banks are “strongly capitalized” and are better able to withstand “shocks” than they were before the Financial Crisis; and “credit quality of bank loans appears strong, although there are some signs of more aggressive risk-taking by banks,” the Financial Stability Report says.

Also, leverage at broker-dealers is “substantially below pre-crisis levels.” And “insurance companies have also strengthened their financial position since the crisis.”

A greater worry are hedge funds that are now being leveraged up to the hilt. “A comprehensive measure that incorporates margin loans, repurchase agreements (repos), and derivatives – but is only available with a significant time lag – suggests that average hedge fund leverage has risen by about one-third over the course of 2016 and 2017.”

“The increased use of leverage by hedge funds exposes their counterparties to risks [that would include banks and broker-dealers] and raises the possibility that adverse shocks would result in forced asset sales by hedge funds that could exacerbate price declines.”

But here is why they won’t get bailed out: “That said, hedge funds do not play the same central role in the financial system as banks or other institutions.”

Consumers are in pretty good shape, except…

In terms of their mortgage debt to GDP and income levels, consumers are in pretty good shape, the report said, but student loans – 90% of which are guaranteed by the government – and auto loans are out of whack, and there are some problems in the subprime segment.

But business debt, oh my!

The Fed finds that asset valuations are “generally elevated” as investors “exhibit a high tolerance for risk-taking, particularly with respect to assets linked to business debt.”

“Asset valuations appear high relative to their historical ranges in several major markets, suggesting that investor appetite for risk is elevated.” In this category of overvalued assets waiting for sharp price declines, it lists:

- Commercial real estate ($21.2 trillion in assets) – it has a lot to say about CRE valuations and risks – see below.

- Junk bonds and leveraged loans ($2.4 trillion combined) exhibit yield-spreads to Treasury securities that “are near the lower end of their historical range.”

- Investment-grade corporate bonds and commercial paper ($6.2 trillion) – see below.

- Stocks ($33.8 trillion in market capitalization) have seen rising P/E ratios since 2012 that are now “above their median values over the past 30 years despite recent price declines.”

- Farmland prices ($2.2 trillion total), though down from their 2016 peak, “remain very high by historical standards.”

Commercial real estate ($21.2 trillion in assets):

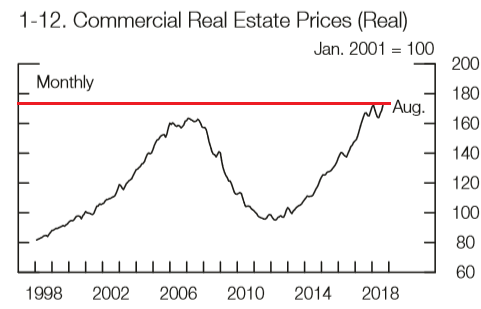

Though prices of commercial real estate (CRE) have been about flat compared to a year ago, they had been growing faster than rents for years. The chart below shows the index of CRE prices adjusted for inflation (via core CPI). These “real” CRE Prices are now higher than they were before it all blew up (I added the special effect in red):

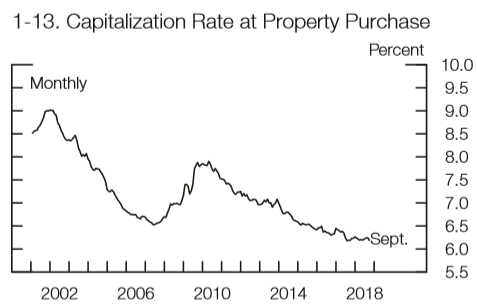

These high prices have led to capitalization rates at the time of purchase that are, compared to 10-year Treasury securities, very low. In other words, “returns to CRE property investors thus reflect a relatively low premium over very safe alternative investments.” And this cannot last.

The chart below shows the three-months moving average of cap rates across the US on a square-footage basis for industrial (warehouses and the like), retail, office, and multifamily sectors:

Given the CRE-bubble of historic proportions, banks should tighten lending to curtail their risks. Instead they “have eased a bit over the past year.”

Borrowing by nonfinancial businesses ($17.1 trillion, excluding banks)

“Business-sector debt relative to GDP is historically high and there are signs of deteriorating credit standards,” the report warns – with debt “growing fastest at firms with weaker earnings and higher leverage.”

This $17.1 trillion in business debt includes:

- Corporate business credit: $9.4 trillion

- Noncorporate business debt: $5.4 trillion

- Commercial real estate debt: $2.4 trillion

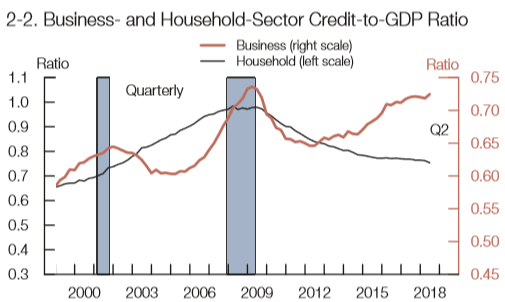

The chart below (the original chart goes back to 1980) shows non-financial business debt and household debt in relationship to GDP. Due to the decline in mortgage debt in relationship to GDP, household debt overall is in pretty good shape, with a declining credit-to-GDP ratio. Before the Financial Crisis, it was household debt that was out of whack and that contributed to the Financial Crisis; now it is business debt:

Business debt has grown “faster than GDP through most of the current expansion.” This debt is “historically high,” and “total business-sector debt relative to GDP stands at a historically high level.” Even so, “risky debt issuance has picked up recently,” and “credit standards for some business loans appear to have deteriorated further.”

The Fed had a special word for leveraged loans:

“Credit standards for new leveraged loans appear to have deteriorated over the past six months.

“The share of newly issued large loans to corporations with high leverage – defined as those with ratios of debt to EBITDA (earnings before interest, taxes, depreciation, and amortization) above 6 – has increased in recent quarters and now exceeds previous peak levels observed in 2007 and 2014 when underwriting quality was notably poor.

“Moreover, there has been a recent rise in ‘EBITDA add backs,’ which add back nonrecurring expenses and future cost savings to historical earnings and could inflate the projected capacity of the borrowers to repay their loans.”

The Fed has been warning about leveraged loans for years. Most recently it pointed at specific practices, such as EBITDA add-backs, collateral stripping, incremental facilities, and cov-lite [The Fed Broadsides $1.3-Trillion “Leveraged Loan” Market].

And it warns about investment-grade bonds.

“The distribution of ratings among investment-grade corporate bonds has deteriorated. The share of bonds rated at the lowest investment-grade level (for example, an S&P rating of triple-B) has reached near-record levels. As of the second quarter of 2018, around 35 percent of corporate bonds outstanding were at the lowest end of the investment-grade segment, amounting to about $2¼ trillion.

“In an economic downturn, widespread downgrades of these bonds to speculative-grade ratings [to junk] could induce some investors to sell them rapidly, because, for example, they face restrictions on holding bonds with ratings below investment grade. Such sales could increase the liquidity and price pressures in this segment of the corporate bond market.”

These investors that might be forced to sell a large amount of bonds as they get downgraded to junk include investment-grade bond mutual funds.

Alas, bond and loan mutual funds “have more than doubled in the past decade to over $2 trillion.” But “the mismatch between the ability of investors in open-end bond or loan mutual funds to redeem shares daily and the longer time often required to sell corporate bonds or loans creates, in principle, conditions that can lead to runs [on the bond funds]….”

“If corporate debt prices were to move sharply lower, a rush to redeem shares by investors in open-end mutual funds could lead to large sales of relatively illiquid corporate bond or loan holdings, further exacerbating price declines and run incentives.”

“Moreover, as noted in earlier sections, business borrowing is at historically high levels, and valuations of high-yield bonds and leveraged loans appear high. Such valuation pressures may make large price adjustments more likely, potentially motivating investors to quickly redeem their shares.”

And here is what this would do to conservative-sounding investment-grade bond funds, which pack special risks & surprises that can entail a catastrophic loss for investors when there is a run on the fund.

This is further exacerbated as “leverage of some firms is near its highest level seen over the past two decades,” the Fed mused:

“An analysis of detailed balance sheet information of these firms indicates that, over the past year, firms with high leverage, high interest expense ratios, and low earnings and cash holdings have been increasing their debt loads the most.”

“High leverage has historically been linked to elevated financial distress and retrenchment by businesses in economic downturns. Given the valuation pressures associated with business debt noted in the previous section, such an increase in financial distress, should it transpire, could trigger a broad adjustment in prices of business debt.”

For now, risky credit for the riskiest companies is still cheap and plentiful, allowing them to refinance their debts, and so “corporate credit performance remains generally favorable.”

But this is precisely what the Fed has set out to change by raising rates and unwinding QE to bring up interest costs for junk-rated companies after the decade long binge. So good luck, the report is essentially saying.

It is also significant that the Fed is now communicating these issues with its first Financial Stability Report. It could have done this years ago, but it didn’t. I see it as an effort to justify rate hikes publicly and in one document: asset prices are inflated, business leverage is at historical levels, and if the Fed doesn’t try to tamp down on it now, it might preside over another financial crisis – and this one would be totally the Fed’s own creation.

Shedding light on Fed Chairman Jerome Powell’s “just below neutral” and the hullabaloo about the Fed suddenly turning “dovish.” Read… My “Fed Hawk-O-Meter” Speaks