“We’re paddling against the current in trying to sustain public faith in the Fed.”

–Federal Reserve Chairman JEROME (JAY) POWELL

“The FOMC (Federal Open Market Committee, the Fed’s key rate-setting entity) is in panic mode now, facing the Frankenstein monster balance sheet it has created. The FOMC has come to the realization that it cannot unwind it.”

–Jones Trading’s chief strategist MIKE O’ROURKE

“The Fed today is as much a prisoner of the market as the market today is a prisoner of the Fed.”

–Epsilon Theory’s BEN HUNT

______________________________________________________________________________________________________________

INTRODUCTION

At the beginning of 2018, we initiated a new EVA series titled “Bubble 3.0” with excerpts from David Hay’s upcoming book titled “Bubble 3.0: How Central Banks Created the Next Financial Crisis”.

If you are just joining us in the middle of this ongoing series, which will eventually culminate in a full-length publication, please take a few moments to review the prior installments in the series:

- Bubble Watch: A New Series Dedicated to Investors Interested in Preserving Their Wealth(December 22, 2017)

- Biggest Bubble Ever Quarterly Webinar (February 9, 2018)

- Bubble 3.0: How Central Banks Created the Next Financial Crisis (April 27, 2018)

- Bubble 3.0: How Did We Get Here? (Part I) (June 1, 2018)

- Bubble 3.0: How Did We Get Here? (Part II) (June 8, 2018)

- Bubble 3.0: A Fast and Furious Challenge (July 6, 2018)

- Bubble 3.0: Up from the Ashes (August 24, 2018)

- Bubble 3.0: The Biggest Bubble Inside the Biggest Bubble Ever (September 21, 2018)

- Bubble 3.0: What Could Go Right (October 12, 2018)

- Bubble 3.0: The Upside of Downside (November 30, 2018)

- Special Edition EVA: The Stealth Bear Market (December 14, 2018)

- Bubble 3.0: What Price Prosperity? (Part I) (January 11, 2019)

- Bubble 3.0: What Price Prosperity? (Part II) (January 18, 2019)

In this month’s edition, David looks at how a recent policy pivot from the Fed could create a longer-term crisis with no way out for the US economy or stock market.

______________________________________________________________________________________________________________

BUBBLE 3.0, CHAPTER 10: NO WAY OUT

“Big hat, no cattle”. “All sizzle, no steak”. “Talks a good game”. Those and other popular sound-bites are meant to refer to someone who is, to use another colloquialism, “all bark and no bite”. When it comes to most of the world’s central banks, all of those quips apply.

If you think I’m being excessively judgmental, consider recent developments: The European Central Bank (ECB) has been adamant about its desire to both begin raising interest rates and shrinking its bloated-like-a-Sumo-wrestler-on-steroids balance sheet.

Adamant, that is, until recently. Thanks to weakening inflation and continuing anemic growth on the Continent, rate hikes are off the table. Soon-to-be-outgoing ECB emperor chief Mario Draghi is already making noises about restarting its quantitative easing (QE) program rather than reversing it as its American counterpart, the Fed, has done. This is despite the fact that the ECB’s balance sheet—or stash of European bonds bought with pseudo-euros—is an outrageous 40% of GDP versus “only” about 20% in the case of the Fed (GDP represents a country’s total economic output).

It’s true that Europe’s chronically flaccid economic pulse has faded one more time (European economic “liveliness” almost makes a corpse look animated). As a result, the number of negative-yielding bonds (the ultimate Alice In Wonderland financial condition where borrowers charge lenders to use the latter’s money) is once again swelling. The total value of these legalized investor extortion instruments is now $11 trillion, most of them from European issuers. This is up from the trough of $6 trillion last year when it seemed as though the ECB was serious about at least a feeble attempt at returning to normal monetary conditions (like where lenders get paid to extend credit).

Accordingly, it looks like the rumors of the demise of negative yields have been greatly exaggerated. Per the below, from the Wall Street Journal, almost a quarter of all global bonds outstanding produce, so to speak, negative interest rates.

In Japan, the land of the sinking yen and ever-rising debt, conditions have also flagged lately despite decades of zero interest rates and stupendous deficit spending. One of its most influential business conditions surveys recently noted: “Domestic economic weakness compounded with slowing global growth coincided with the lowest level of business confidence for over six years.”

As the no-nonsense financial commentator Danielle DiMartino Booth, former adviser to ex-Dallas Fed president Dick Fisher, recently wrote: “Not to beat a very dead horse but negative interest rates in Japan and Europe were supposed to have generated virtuous outcomes.” (Emphasis hers.) In other words, these radical policies, that were designed to stave off the ravages of the Great Recession and stimulate healthy economic growth, continue to fail to bring home the mail.

Then there’s America and its relatively new Fed chairman, Jerome Powell (Jerome sounds much more forceful than Jay, the handle he seems to prefer, doesn’t it?). Jerome came in with both guns blazing, raising rates and shrinking the Fed’s balance sheet, what we and others (like Danielle) have called a double-tightening. (As a reminder, increasing the Fed’s balance sheet was popularly known as quantitative easing or QE, which was where it essentially created $3.8 trillion of fake money to buy government debt. Other central banks, such as the ECB, the Bank of Japan, the Bank of England, and the Swiss National Bank also engaged in this monumental monetary fabrication.)

As recently as last fall, Mr. Powell “talked a good game” of ignoring market volatility (meaning sell-offs). He even hiked rates in mid-December despite a reeling stock market. He additionally seemed intent on continuing the double-tightening, also announcing in December that the balance sheet shrinkage—or quantitative tightening (QT)—was on “autopilot”. Based on the press conference he gave at the end of January, apparently that autopilot has already been switched off.

Many pundits have reacted to this about-face angrily and are accusing Jay (not Jerome) of caving into political pressure from the meddler- (and Tweeter-)-in-chief. Others have screamed that he has done exactly what he said he wouldn’t do by trying to sooth the stock market with dovish utterances once it was down about 20% from its September peak.

Conversely, the preternaturally bullish crowd on CNBC, especially Jim Cramer, have been delighted with Powell’s almost overnight conversion from hawk to dove. (On that topic, I was interested, but not surprised, to read that when the long-bearish John Hussman appeared on CNBC a few weeks ago, he was told to put a positive spin on his views. Talk about fake news! But to his credit, John didn’t dilute his message.)

Certainly, the stock market has loved the Jerome to Jay metamorphosis. From a selfish standpoint, Evergreen is in the pleased camp since it has been the bombed-out strata of what we’ve been calling the two-tier US stock market that has been in the vanguard of this powerful rally since the late December lows. In fact, energy in general and mid-stream energy assets (pipelines, et al) in particular, have been at the head of the charge, as we had hoped and anticipated, per our early January special message.

But from a non-selfish vantage, I have serious misgivings about how even the most timid attempts at so-called monetary policy normalization (read: getting interest back up to a point where savers care about saving) caused things to fall apart. Also from a self-centered view, that’s a vindication. Whenever I was asked (and often even when I wasn’t) how long the Fed would tighten, my simple answer was: “until something breaks”. It’s fair to say that a lot of things broke—make that shattered–in the financial markets in last year’s fourth quarter and we now believe the Fed is done with actual rate increases. (The continuing balance sheet shrinkage, effectively representing further rate hikes, is a different story.)

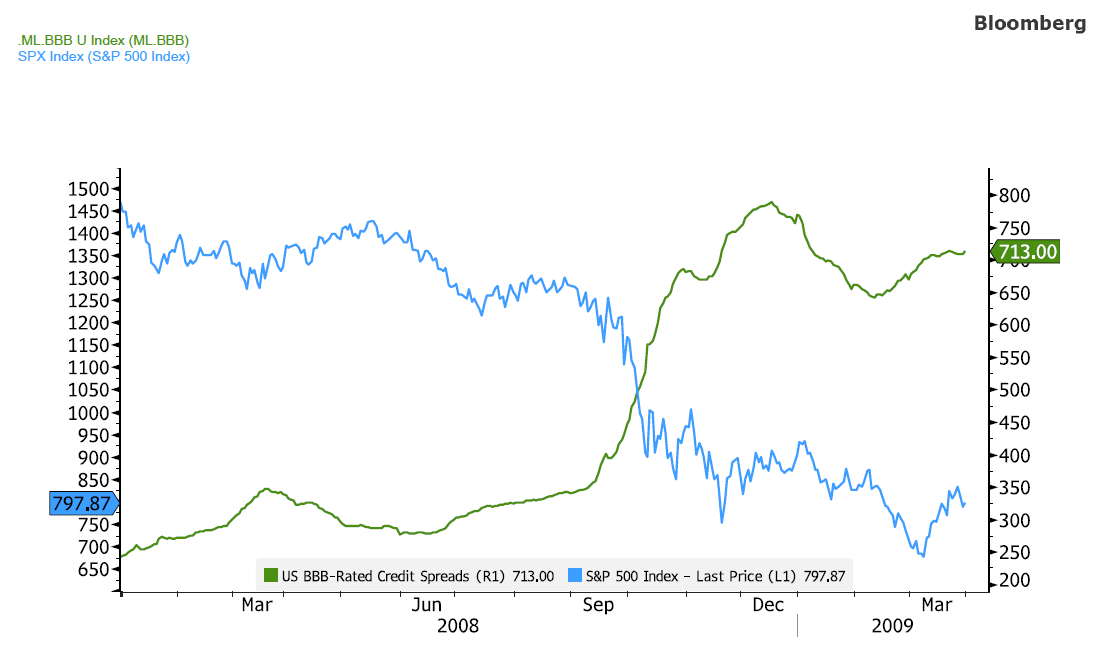

As usual, stocks hogged all the press during last quarter’s crashette but I’d argue another development alarmed the Fed just as much…if not more. EVAs ad nauseum (no doubt nauseating many of our readers in the process) have conveyed the vital role of credit spreads. Also, ad nauseum, we’ve explained that these represent the gap between the government’s borrowing costs and those of Corporate America. We’ve also repeatedly noted that when those contract it’s very good news and when they widen, especially “bigly”, it’s head-for-the-hills time.

The above chart shows what’s been going on with spreads over the last five years. You can easily see that when they’ve been narrowing, or are stable, the stock market does just fine. However, when they zoom higher, red ink tends to flow down the canyons of Wall Street.

What was a bit different this time is that stocks seemed to lead credit spreads rather than the other way around, as is more common. To illustrate the typical sequence, witness what happened to spreads and stocks in 2007 to early 2009, as well as in 2011 and 2012.

But it is probably fair to say that the spike by spreads late last year elevated what was a mere correction into a near bear market for the S&P. Moreover, there was no “near” about it for most overseas stock markets, US small- and mid-cap stocks, and, frankly, most US issues save a few monster-cap names like Amazon, Netflix, Google, and Microsoft (i.e. the majority of the famous FANGM). Said differently, what was an already very painful dive of almost 20% by the S&P was far worse for a wide range of asset classes and individual stocks.

Thus, it’s likely that this darker backdrop was a key reason for the Jerome to Jay, monetary muscleman to monetary milquetoast, changeover – kind of like Superman reverse-morphing back to Clark Kent. As we noted at the end of December, it was becoming an out-and-out panic. Just as we saw at almost the exact same time of the year in 2008, those type of events can get out of hand very quickly. Once they’ve done so, it can be extremely challenging to convince terrified investors to get a grip.

If it sounds like I’m asking for some slack to be cut for old Jay (who’s actually just about my age, so, naturally, I don’t think he’s THAT old), I guess I am, emphasis on “guess”. The fact of the matter is I simply feel resigned to the ugly reality of current conditions. As I noted in the “What Price Prosperity” chapter, the reigning King of Bonds, Jeff Gundlach, summed it up best, in my view, when he said: “The Fed is damned if they do and damned if they don’t.” Ergo, they’re doomed if they keep tightening and they’re doomed if they stop.

Maybe you think doomed is too harsh a word, and perhaps it is. But I think what’s becoming increasingly clear is that the leading global economies are doomed destined to occupy a twilight zone of chronically deficient growth, rapidly rising debt levels, and a constant absence of interest rates. Frankly, I think the Jim Cramer’s of the world salivate over this scenario because they feel it means the US bull market isn’t dead after all. With the Fed on hold, it’s a greenlight for investors to go back into full risk-on mode, as they have most enthusiastically done this year. Or at least that’s how the current market narrative is shaping up.

To repeat, my personal portfolio and those of Evergreen clients are loving this revival of animal spirits. Even our most conservative strategy is off to a very fast start thus far in 2019. But down deep, and not really that deep, it seems to me the market is making a monstrous mistake. It’s not asking another one of those nagging questions—like what price (pseudo) prosperity?—such as, “What’s the ultimate end-game?”

With profuse apologies to all those who put their lives on the line in Iraq and Afghanistan, it feels to me like the financial equivalent of those quagmires. The US and its allies put enormous military force to work in both countries and, in fairly short order, were able to “win” both wars. But it seemed to me at the time, and it still does, that we never thought about an exit strategy. (It was illuminating in this regard to watch the PBS American Experience tribute to the life of George H. W. Bush. In it, several of his top advisers from the first Gulf War were interviewed and they recounted how much heat they took after it was over for not marching into Baghdad and deposing Saddam Hussein. Each of them pointed out they don’t hear those criticisms any longer after the world has had a chance to witness the near-impossibility of fully exiting either Iraq or Afghanistan.)

Basically, the US high command employed a massive military intervention. It had a brilliant plan to win the wars but, apparently, almost no plan to win the peace. Similarly, the planet’s central banks never seemed to have a sound strategy for withdrawing from their decade-long, multi-trillion experiment, one that has never been tried before—perhaps for good reason.

As noted earlier in this series, and we will see again at the end of this chapter, our forecast has long been that it will shock most people how little tolerance even the US has for higher interest rates. The market tumult of last quarter was one vivid illustration. But there’s more at work here and I think this is what the market is missing right now in its “O, Be Joyful” reaction to Jay Powell’s flip-flop. To quote Bill Clinton’s former top political strategist, James Carville: “It’s the economy, stupid.”

Lost in all the anxiety, followed by euphoria, over the Fed’s stance and the market’s response to same – not to mention the confusion of the government shutdown – is what is happening to economies both in the US and the rest of the world. Unquestionably, Germany is the lead sled-dog for the European economy and the industrial production numbers it’s been reporting in recent months have been shockingly weak, now down 4% year-over-year. Even German retail sales have recently done a cliff-dive. This is quite a letdown given the supposed health of the Deutschland consumer. Much less surprising is that Italy is sliding back into recession for what seems like the tenth time in the last ten years.

Spinning the globe roughly 180 degrees, China is experiencing what passes for a recession in that country. So far, it’s a growth version–if official numbers can be believed (and that’s a big leap of faith); if not, then you can remove the “growth” part of the description. Even so, China has been reporting the weakest economic data in 30 years. Naturally, stagnation in China ripples throughout the entire Asian region.

Even the “Lucky Country”, Australia, which has been fortunate enough not to have endured a recession in twenty-five years, looks like its luck is running out. Over that time, it has experienced one of the most outrageous housing bubbles ever recorded. Thus, its economy is at grave risk should housing prices decline precipitously. As Sydney-based Gerard Minack pointed out in his February 8th Down Under Daily, “The risk of an Australian recession is rising.” To back up his view, note a few of the charts he ran in that issue.

…