by GoldCore

The fed’s inflation gamble continues…

Are central banks trapped?

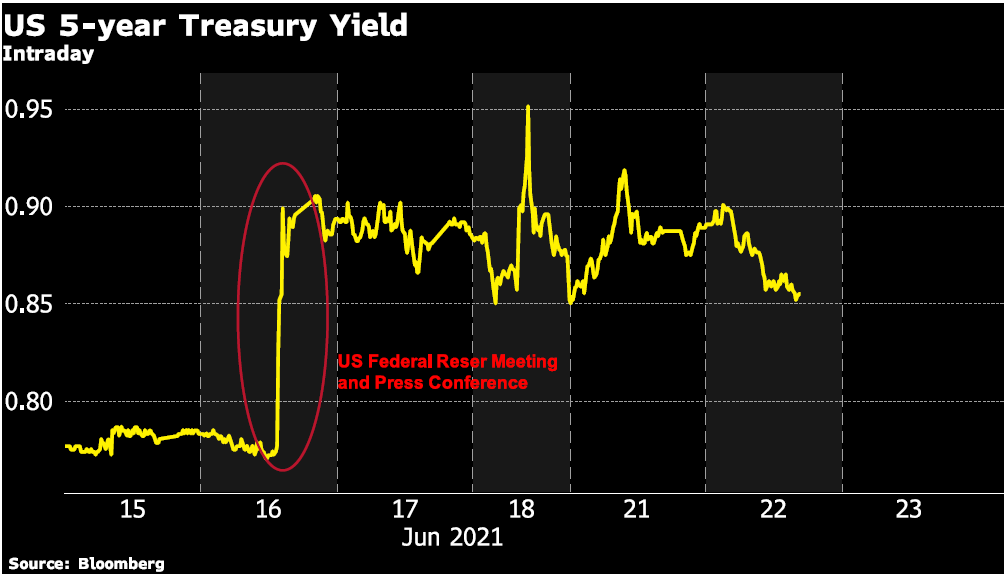

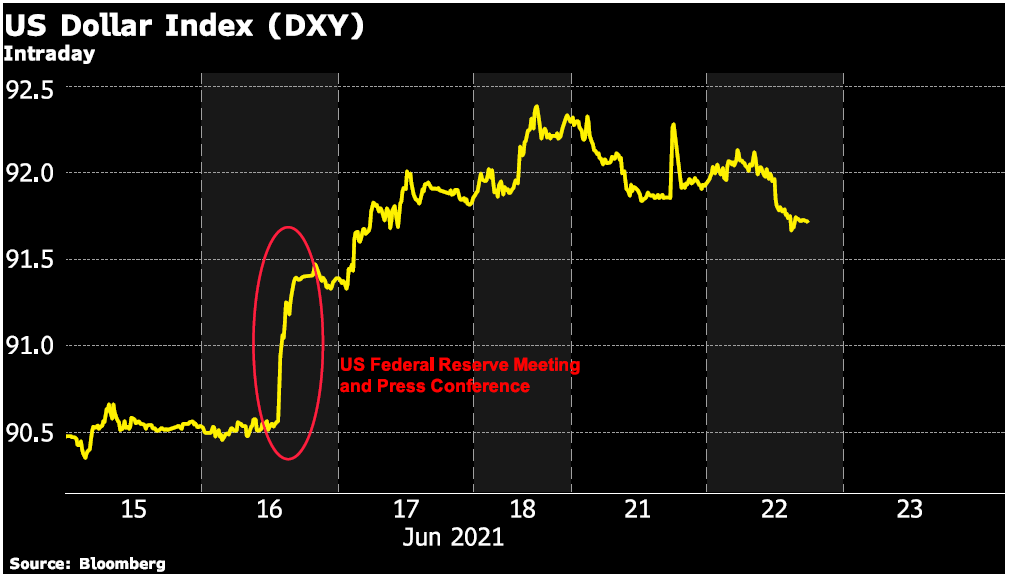

Last week’s Fed statement and the press conference that followed proved to be the start of a US$90 (4.8%) decline in the gold price.

Fed on Economic Recovery

The Summary of Economic Projections (known as the dot-plots) released with the statement showed that committee members changed their median projection for the Fed Funds rate from its current rate of 0.1% to 0.6% by 2023 year-end – an increase of 0.5% or two rate increases more than two years from now.

And these forecasted rate increases will only happen if inflation is well anchored above the 2% target and the Fed feels it has met its maximum employment part of the mandate. In response to a question in the press conference Chair Powell said:

… the main message I would take away from the SEP is that many [FOMC] participants are more comfortable that the economic conditions in the Committee’s forward guidance will be met somewhat sooner than previously anticipated [i.e., labor market conditions consistent with maximum employment, inflation at 2 percent and on track to exceed 2 percent]. And that [is] a welcome development. If such outcomes materialize, it means the economy will have made faster progress toward our goals. …

… the other thing I’ll say is rate increases are really not at all the focus of the Committee. The focus of the Committee is the current state of the economy. … we’re [still] very far from maximum employment, for example. … the near-term discussion that will begin is about the path of asset purchases … we [discussed] that today, and expect to continue in future meetings to think about our progress … Lift-off [a hike in the FF-rate] is well into the future …

Gold to Go $3,000 and Silver $100

Watch David Garofalo on GoldCore TV

The Fed has reason to be optimistic about the economy, as economic data, both anecdotal and official data releases have been stronger than expected.

The housing market in many parts of the country is red hot, employers are scrambling to find workers, retail sales have been strong, and inflation, even taking out the drop from last year has been somewhat elevated.

And remember the Fed is adding US$80 billion in US Treasuries, and US$40 billion in mortgage-backed securities to its balance sheet each month – that’s $120 billion in extra liquidity flowing straight into already drunk markets.

Assets on the Fed’s balance sheet hit over US$8 trillion last week – that is 36% of US GDP.

So here is the trap – not only did gold prices decline by almost 5% last week, but interest rates shot up and the US dollar gained strength – all on the Fed talking about tapering and a forecast of a possible increase more than two years from now. Back to Powell’s press conference for his comments on tapering:

… [As to when we might consider starting to reduce our asset purchases] you can think of this meeting that we had as the talking about [tapering] meeting …

… We don’t think that we’re in a situation [where we need to raise rates to control inflation]. We think that the economy is recovering from a deep hole, an unusual hole actually, because it’s to do with shutting down the economy. It turns out it’s a heck of a lot easier to create demand than it is to bring supply back up to snuff …

Threat of soaring debts

If the market reaction is this strong when the Fed only starts mentioning that it is talking about a plan to cut back on asset purchases. Moreover, that there might be an eventual interest rate increase more than two years from now. How do they actually get a plan implemented that doesn’t send the US economy into a downturn?

The US government added more than US$5 trillion in debt since the onset of the Covid-19 Pandemic in March of 2020. Also, the baseline projection from the Congressional Budget Office is that the US federal budget deficit will average US$1.2 trillion per year over the next decade.

That’s right this is the baseline projection! It does not include any extra spending that the Biden Administration and Congress may pass (such as the currently debated infrastructure bill). US debt is now more than 100% of GDP. For every 1 percent increase in interest rates, more of the US government revenues are sucked up servicing its debt, which leaves less for other programs, which no politicians want!

And if the US leads the way with interest rate increases this puts more upward pressure on the US dollar. Which is good for US consumers of imported goods, but not good for US exporting companies or their employees.

Bottom line is that the Fed is going to stay behind the inflation curve and lower for longer is still the motto of the day. Higher inflation, low real-rates, and a lower dollar are all good for gold in the long-run!

We turn back to Chair Powell’s comments in the press conference for the last word:

… the last thing to say is, the dots are not a great forecaster of future rate moves. And that’s because it’s so highly uncertain …