By Wolf Richter for WOLF STREET.

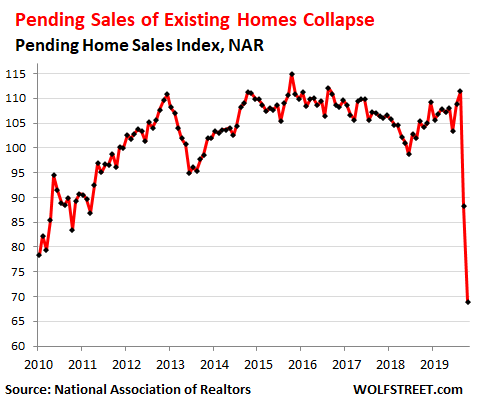

Pending sales of existing homes of all types in April – contracts on houses, condos, etc., that were signed in April but that haven’t closed yet – collapsed by 33.8% from April last year, after having plunged 16.3% year-over-year in March, with the index plunging to 69, according to the National Association of Realtors today. An index value of 100 represents the pending sales level of January 2001.

Pending sales are an indication of what closed sales will look like a month or two down the road. So this is an indication of the direction that May’s closed sales are heading into.

We already know how pending sales in March translated into closed sales in April. Pending home sales for March had plunged 16.3% year-over-year. And on May 21, the NAR reported that closed sales in April plunged 17.2%, the sharpest year-over-year drop since August 2010, during the Housing Bust.

Based on this relationship, closed sales of existing homes in May might be down by 30% or more, year-over-year. This will be reported in June.

The plunge of the pending home sale index differed by region, ranging from a breath-taking collapse of -52.6% in the Northeast to a plunge of “only” -26.0% in the Midwest:

- Northeast: -52.6% year-over-year to an index level 42.6.

- Midwest: -26.0% year-over-year to an index level of 72.0.

- South: -29.6% year-over-year to an index level of 87.6.

- West: -37.2% year-over-year to an index level of 57.1.

When sales volume collapses to this extent – no matter what the market is – it changes everything. It represents a market that has essentially frozen, with few buyers and few sellers, and lots of uncertainty. This is what happened in many other markets in the US, including otherwise very liquid markets, such as the wholesale market for used vehicles.

In May those markets have begun to unfreeze. Market participants have figured out how to deal with the requirements of social distancing. Keeping everyone reasonably safe during a pandemic that has already killed over 100,000 Americans in less than three months is a primary objective.

In the housing market, this has led to a change in the way business is conducted, including forays into accepting technologies, such as virtual open houses. This technology has been around for long time, but the pandemic pushed it into the foreground – like so many other technologies in so many other industries. And people are finding out that it sort of works.

But the market is facing ferocious headwinds, including 31 million people now collecting state and federal unemployment insurance.

More mass layoffs by big companies are announced every day, such as American Airlines’ message to its employees late Wednesday that it would cut its management staff by 30%. Delta came out with plans today to shed staff via early retirements and buyouts, along with Chevron that said it would cut up to 15% of its global workforce of 45,000 people, and Boeing which said it would cut 7,000 workers. Just one days’ worth of work, so to speak.

These are not restaurant jobs. These are jobs that come with good paychecks and benefits.

And this constant flow of announcements does two things: It creates uncertainty among potential home buyers that kept their jobs; and it removed potential home buyers from the market that have lost their jobs. This is a gigantic unemployment crisis, interspersed with a tsunami of bankruptcy filings, of even large companies such as Hertz, each accompanied by more layoffs.

Eventually – next week or next month or whenever – the job losses will end as more workers will return to work, and employment will start to rise, but from abysmally low levels, and even after rising for a while, employment will still be abysmally low – just less abysmally low.

So the housing market – in terms of sales volume – has two separate things to deal with:

One, the issues around keeping buyers, sellers, brokers, and others safe. The industry is addressing these issues in multiple ways, and is harnessing technologies to overcome the issues, and there is progress, and more deals are happening.

Two, the employment crisis that has already taken millions of potential buyers off the market. Even people who return to work after a stint on unemployment cannot instantly turn into homebuyers because it’s hard to get a mortgage, right after having been unemployed.

So volume will pick up some because the immediate issues of the pandemic are being dealt with successfully by the industry; but volume will not return to normal levels until employment has returned to normal levels – and having lost over 30 million jobs so far, this is just going to take a while.