Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

The rate cuts for 2019 are a pipe-dream: Goldman Sachs and Deutsche Bank.

It now makes two: The chief economists at investment banks Goldman Sachs and Deutsche Bank have warned their clients that the already priced-in rate hikes this year that markets are so excited about may not materialize.

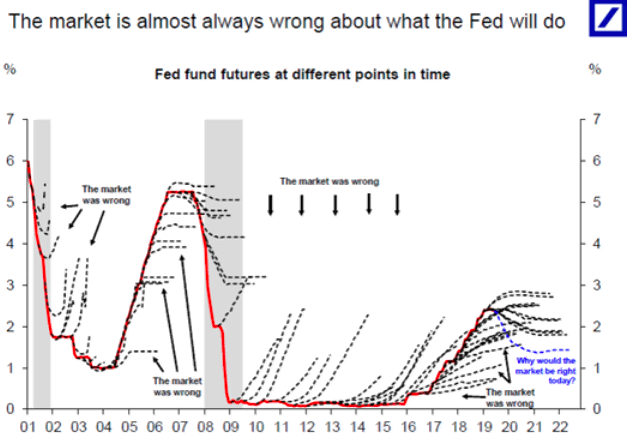

To proof their point, Deutsche Bank chief economist Torsten Slok and his team dug through the data going back to 2001, comparing the path of the federal funds rate – which reflects the Fed’s rate hikes and cuts – to the futures markets for the federal funds rate. They concluded: “The market is almost always wrong about what the Fed will do.”

And they asked: “Why would the market be right today?” That was a rhetorical question.

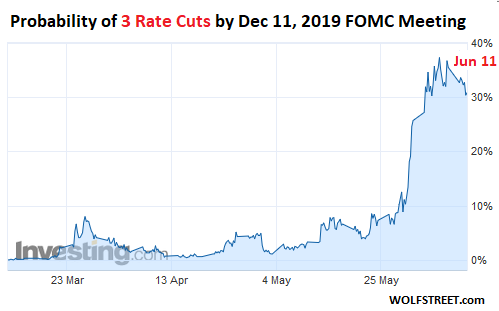

Yet, these bets – that are “almost always wrong” about the Fed’s rate decisions – are now being incessantly cited to show that the Fed will cut its target range for the federal funds rate. At the moment, these traders see an 80% probability that the Fed will cut its target range at least twice by the December 11 meeting, including a 31% probability of three cuts by then, and a 10% probability of four cuts, as implied by trading of 30-day Fed Fund futures.

This chart shows how three rate cuts suddenly gained momentum among Fed Funds futures traders on the CME, though tapering a tad over the past two days (chart via Investing.com):

Anytime the rate-cut mongers on Wall Street can twist something a Fed governor says into a rate-cut projection, they will. For example, Fed chair Jerome Powell gave a speech on June 4 about long-term questions the Fed has been mulling over. The speech was unrelated to what the Fed will do over the next few meetings. Out of context, he shoehorned this line – “we will act as appropriate to sustain the expansion” – into the beginning.

The rate-cut mongers took this line as affirmation of the three-rate-cut expectations. Yet there was not a single word about any impending rate cuts in this speech. That the Fed will “act as appropriate” is standard Fed lingo to describe that the Fed is awake. It can go both directions, hike or cut.

And so the team at Deutsche Bank came out with this chart (via Bloomberg), titled, “The market is almost always wrong about what the Fed will do,” where they compare what the federal funds rate (red line) actually did, and what trading of Fed Fund futures said it would do (dotted black lines):

From 2001 to 2004, federal funds futures projected that the Fed would hike rates. But the Fed kept cutting rates. Then, when the Fed finally started hiking rates, federal funds futures projected all the way along that it would stop hiking rates at any time now. Wrong, wrong, wrong. And so on.

During the years of ZIRP, federal funds futures projected rate hikes, and were wrong about it until 2016, when the Fed finally started hiking rates, federal funds futures nailed it briefly, and then wrongly and consistently projected far fewer rate hikes than the Fed actually undertook.

The sagging dotted blue line from 2019 into the future shows where the market projects the Fed is going. And the Deutsche Bank team observes (in blue): “Why would the market be right today?”

In other words, the market is clueless about the Fed’s rate decisions in the future. It has its own reasons for betting the way it does, but accurately projecting where the Fed is moving with its interest rate target is not one of them.

And yesterday, it was Goldman Sachs chief economist Jan Hatzius in a note, cited by CNBC. He homed in on the market’s interpretation of Powell’s act-as-appropriate line.

Without this line, the speech that was “focused exclusively on longer-term issues at a time of sharply increased worries about trade policy, might otherwise have come across as ‘out of touch’ to some market participants,” he writes.

“In our view, this was not a strong hint of an upcoming cut but was simply meant to provide reassurance that the FOMC is well aware of the risks from the trade war.”

Goldman Sachs expected Fed governors “to be very careful not to deliver an unconditional hawkish message, but to continue emphasizing that they will respond to shocks as needed to attain their mandate.”

Given that the FOMC meeting in June will take place right before the G-20 summit where Trump is hoping to meet with China’s President Xi Jinping on the sidelines, and the uncertainties around it, “the right course of action is to retain optionality,” Hatzius writes.

He expects the FOMC to downgrade the economic outlook a tad at the June meeting, with a few participants signaling that they might favor rate cuts, but that the dot plot’s median forecast for the target range for the federal funds rate will remain unchanged, and that there will be “no signal from Powell that a cut is in fact imminent.”

In terms of the rest of 2019, Hatzius writes: “Although it is a close call, we still expect the FOMC to keep the funds rate unchanged in the remainder of the year.”

But if there are no rate cuts, though the stock market and the Treasury market have surged on the expectations of two or three rate cuts, someone will have to talk down the markets gradually — or else. And maybe Goldman Sachs is trying to lay the groundwork.