“Borrowing our way out of debt” generates the three Ds of Doom: debt leads to default which ushers in Depression.

Let’s start by defining Economic Depression: a Depression is a Recession that isn’t fixed by conventional fiscal and monetary stimulus. In other words, when a recession drags on despite massive fiscal and monetary stimulus being thrown into the economy, then the stimulus-resistant stagnation is called a Depression.

Here’s why we’re heading into a Depression: debt exhaustion. As the charts below illustrate, the U.S. (and global) economy has only “grown” in the 21st century by expanding debt roughly four times faster than GDP or earned income.

Costs for big-ticket essentials such as housing, healthcare and government services are soaring while wages stagnate or decline in purchasing power.What’s purchasing power? Rather than get caught in the endless thicket of defining inflation, ask yourself this: how much of X does one hour of labor buy now compared to 20 years ago? For example, how much healthcare does an hour of labor buy now? How many days of rent does an hour of labor buy now compared to 1999? How many hours of labor are required to pay a parking ticket now compared to 1999?

Our earnings are buying less of every big-ticket expense that’s essential, and we’ve covered the gigantic hole in our budget with debt. The only way the status quo could continue conjuring an illusion of “prosperity” is by borrowing fantastic sums of money, all to be paid with future earnings and taxes.

At some point, the borrower is unable to borrow more. Even at 0.1% rate of interest, borrowers can’t borrow more because they can’t even manage the principal payment, never mind the interest. That’s debt exhaustion: borrowers can’t borrow more without ramping up the risk of default.

When wages are stagnant and big-ticket items are soaring in cost, that leaves less available to service more debt. We can cover expenses by borrowing more for a while, but there’s an endgame to this trick: even at zero interest, servicing the debt exceeds income.

Marginal borrowers default, and the resulting losses collapse marginal lenders.Recall that every debt is somebody else’s asset and income stream. When a student defaults on a student loan, that erases the asset and income stream of a mutual fund, pension fund, etc.

In other words, defaults are not cost free. They wipe out assets and income streams, never to return.

For the past 20 years, the trick to escaping recessions has been to lower interest rates and flood the financial system with new credit. If everyone would just borrow more and spend every cent of the new money, the economy will start “growing” again.

But we’ve reached the point where most wage earners can’t borrow more, corporations shouldn’t borrow more and the top tier of earners no longer want to borrow more. Governments can always borrow more, but eventually servicing the ballooning debt starts crowding out other spending, and the solution–borrowing more to cover the interest payments–spirals out of control.

Lowering interest rates and giving banks and financiers “free money” doesn’t increase wages or household incomes or corporate profits. Nor do these monetary tricks magically turn marginal borrowers into creditworthy risks.

Borrowing more to fill the hole left by declining purchasing power only works in the short-term. We’ve burned the 20 years that this trickery can work, and now we face the endgame: borrowing more only increases defaults, which trigger losses in wealth and income that will be measured in the trillions.

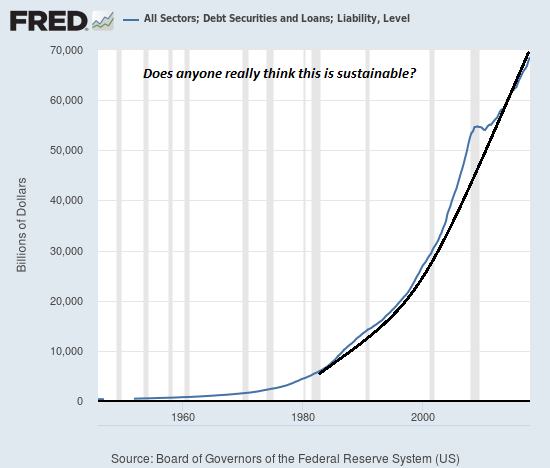

Take a look at systemwide debt in the U.S. Does this look remotely sustainable? If the answer is yes, you might want to dial back your Ibogaine consumption.

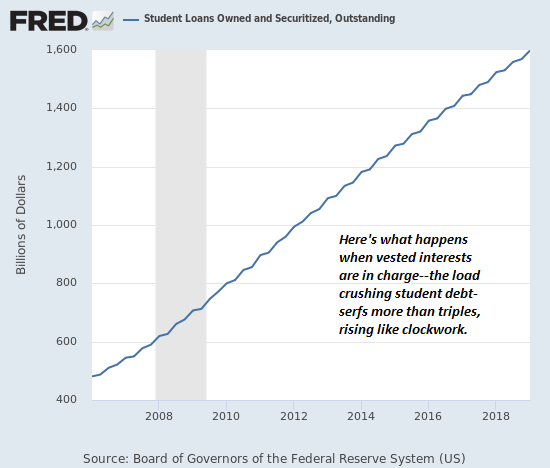

Here’s student loans. One trillion here and one trillion there, and pretty soon you’re talking about entire generations of debt-serfs and a bunch of pension funds that are going to suffer catastrophic losses when the student borrowers default.

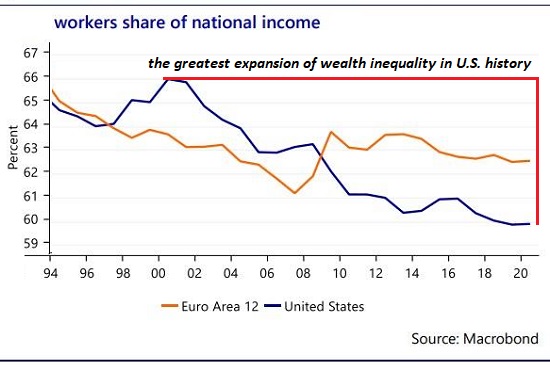

Meanwhile, labor’s share of the economy (wages and salaries) has been in structural decline the entire 21st century. Lowering interest rates to zero doesn’t mean it’s free to borrow more; the principal payments loom large in every student loan, auto loan, mortgage, etc.

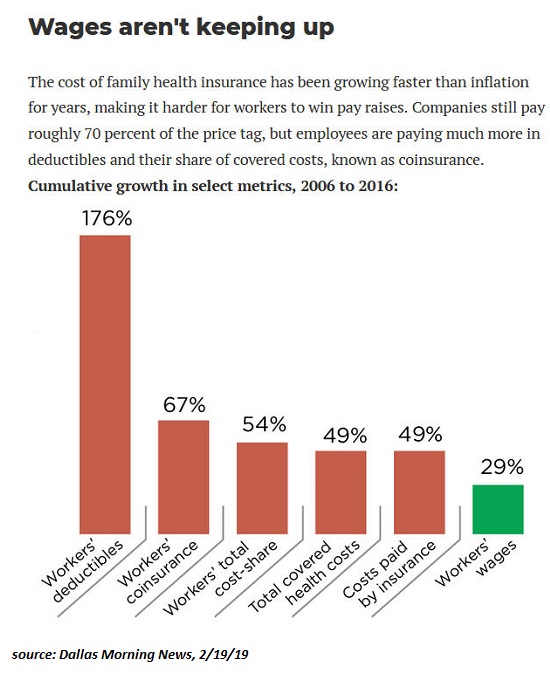

There’s less–a lot less–available to fund more borrowing after those stagnating wages pay for rent or a mortgage/property taxes, healthcare, childcare, student loans, etc. This chart depicts healthcare costs, but rent, childcare, higher education, etc. all mirror similar increases.

“Borrowing our way out of debt” generates the three Ds of Doom: debt leads to default which ushers in Depression.