by FS

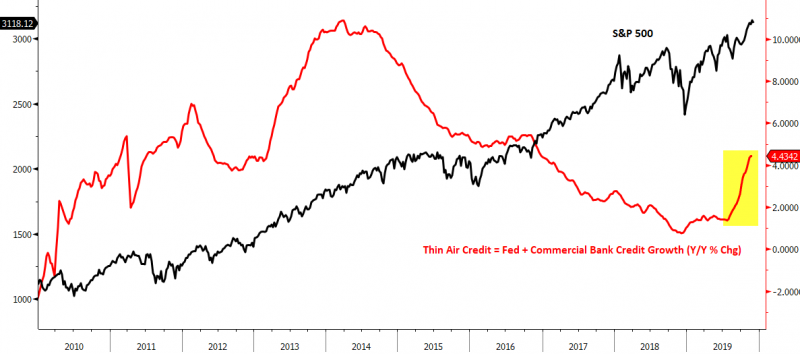

As discussed with Macro Watch’s Richard Duncan on our podcast this week (see The Most Extraordinary Monetary Policy U-Turn In History), credit growth has moved sharply higher following the repo crisis in September. The Fed is now injecting hundreds of billions of dollars into the financial system and expanding their balance sheet at the fastest monthly pace since the 2008 financial crisis, which some—like Duncan—are calling a resumption of quantitative easing.

Here is a chart of “Thin-Air Credit” growth (hat tip to Paul Kasriel) showing the quadrupling of Federal Reserve and commercial bank credit growth just this quarter.

The ISM US Manufacturing PMI gauge came out for November and remained in contractionary territory for the 4th consecutive month. Contrast this to the improving Markit US Manufacturing PMI which showed three consecutive increases and has remained in expansion territory. We believe the Markit survey provides a better gauge of the US manufacturing sector since it gives greater weight to more forward-looking components (and tends to turn ahead of the ISM survey for that reason) and also because Markit has a much larger sample size of companies as part of its survey.

Our Financial Sense Leading Economic Indicator mirrors the Markit PMI data and suggests an inflection in global growth has been seen while a bottom in US growth is likely a few months out (see Building Signs of a Global Recovery).

Global interest rates bottomed in August and tend to coincide with global economic growth. A further move higher in developed yields (Japan, Germany, etc.) will solidify that a bottom has been seen.

Investment conclusions:

Our model regime remains between Neutral and Max Risk on equity exposure. We remain bullish as global LEIs show signs of either bottoming or improvement. Currently, our cash levels are higher than model weight to take advantage of a potential economic turnaround.

To find out more about Financial Sense® Wealth Management or for a complimentary risk assessment of your portfolio, click here to contact us.

Advisory services offered through Financial Sense® Advisors, Inc., a registered investment adviser. Securities offered through Financial Sense® Securities, Inc., Member FINRA/SIPC. DBA Financial Sense® Wealth Management.