One of the lessons of the past few decades’ boom/bust cycles is that each financial bubble emerges in a different asset class. In the 1970s it was precious metals, in the 1980s junk bonds, in the 1990s tech stocks and in the 2000s mortgage-backed bonds.

Today the only one of these with a reasonable chance of blowing up the economy is Big Tech, which is wildly overvalued by any historical measure.

But a better candidate for the title of most dangerous bubble is emerging: Corporate debt, specifically the “almost junk” portion of that market.

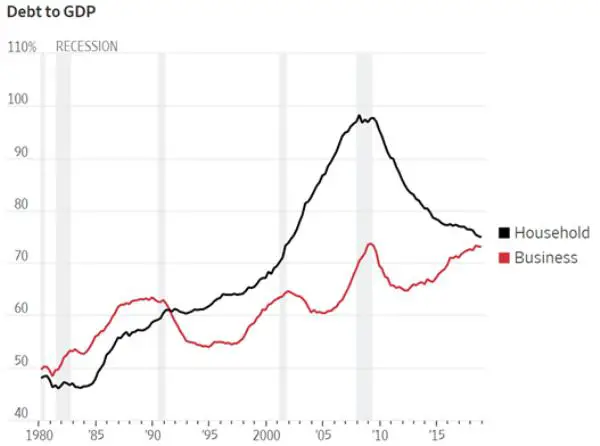

Let’s start with the ongoing surge in overall corporate borrowing, which as a percentage of GDP is now back to the high achieved during the Great Recession, and higher than before the previous two recessions:

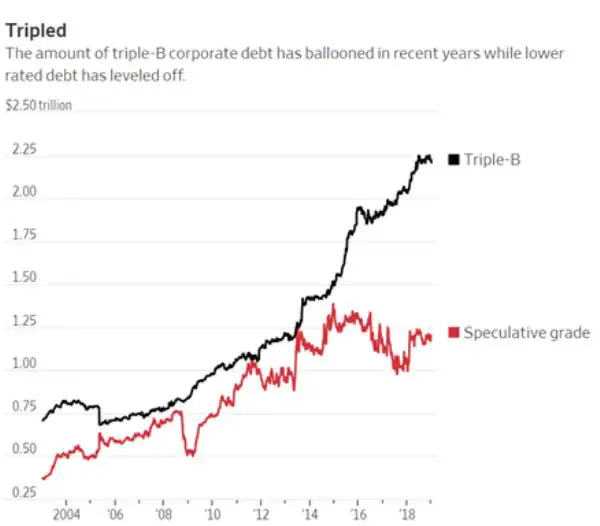

But not all corporations are misbehaving. The clear and present danger is coming from BBB rated debt, which means low-rated borrowers that aren’t quite as dicey as actual junk borrowers. This category was less than $1 trillion in the 2000s housing bubble and has since about tripled.

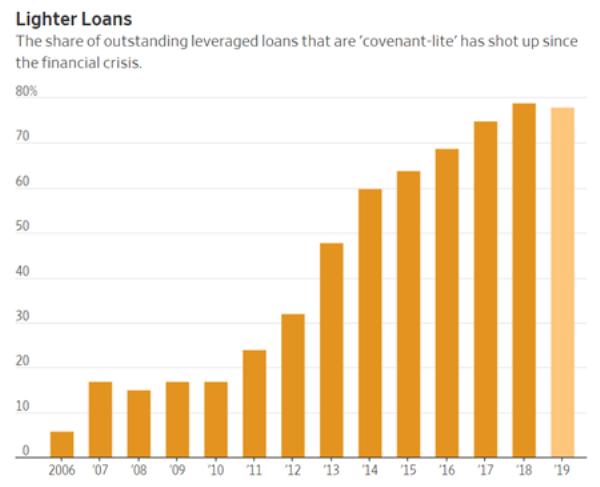

Meanwhile, the terms of these loans are increasingly of the “covenant-lite” variety that don’t require companies to keep their finances within reasonable boundaries. This kind of bond is now 80% of the speculative-grade, or leveraged, loan market, up from just 6% in 2006.

Here’s how this probably plays out. As low-quality borrowers’ interest costs soak up an ever-larger share of their earnings, they’ll start dropping into junk status. This will lead investors to demand higher yields for the remaining BBB bond issuers. Higher borrowing costs will then push more iffy companies into junk, and so on, until lenders stampede for the exits, shutting off access to capital for all but the top corporate borrowers.

Credit-starved companies will start dying, spooking the stock market, and that will be that for this expansion.

The new problem this time around is that potentially bad debts are everywhere, from emerging market dollar-denominated bonds to Italian sovereign debt, Chinese shadow banks, US subprime auto loans, and US student loans. All are teetering on the edge, just waiting to be nudged into the abyss by some external crisis.

So trouble in one sector can metastasize in ways that the global financial system hasn’t seen since the 1930s, forcing central banks to do some truly extraordinary things. Which is the real story here: Not the coming crisis but the monetary authorities’ reaction to the crisis.