via Zerohedge:

As far back as 2013, China’s macro-economic data has been ‘questionably’ smoothed at best, and outright fake at worst.

Whether it is trade data (“never been faker” than in 2016) or aggregate production (2018’s massive GDP distortions), as economist Nouriel Roubini once asserted, China just makes its numbers up.

This month was no exception…

Following China GDP’s dramatic slowing to just 6.2% YoY – the slowest since record began – there was a delightful surprise to appease those who are wondering whether record credit injections and more easing measures than during the financial crisis had any effect at all.

China retail sales and industrial production rebounded handsomely with the former spiking 9.8% YoY – the most since March 2018.

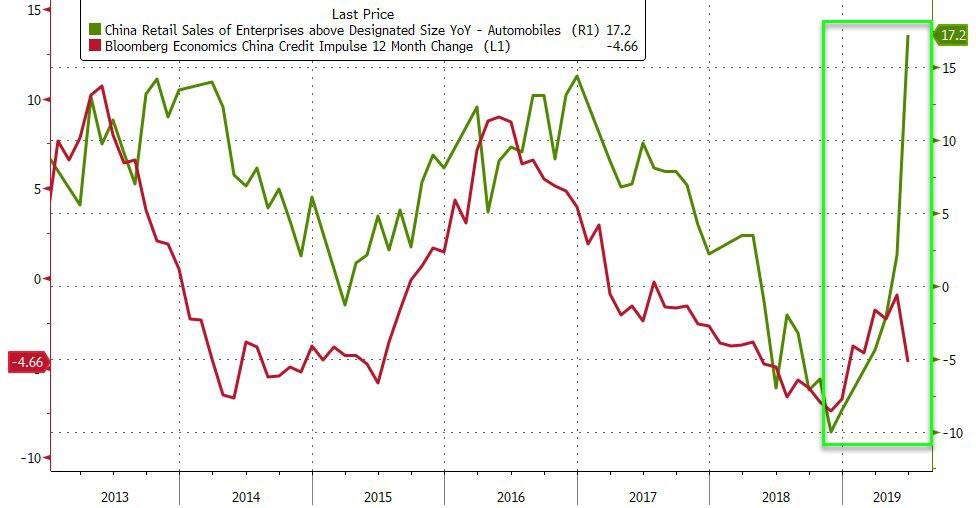

There’s just one thing though – the entire surge in retail sales (and industrial production) seems to have been triggered by an almost unprecedented sudden surge in auto sales to large (state-owned) enterprises…

A 17.2% YoY explosion in sales to SEOs (up from just 2.1% in May) – the most since August 2011 – is almost too good to be believed (ok forget almost, it is too good to believe and seems like pure top-down manipulation of the data – whether sales were effectuated or not), echoing the kind of forced buying rush that occurred in 2009.

And that did not end well.

However, absent considerably more liquidity, forced credit injections, or a miracle, Auto sales are about to hit a wall as China’s credit impulse begins to slow…

Finally, no matter what China does to ‘flatter’ its data and project economic might in the face of Trump tariffs and a collapsing ponzi scheme, the single stat that is hardest to fake (and easiest to see reality) is the dramatic decline in the marginal productivity of debt. As John Rubino recently noted, China, like the US, is getting progressively less bang for each newly-borrowed buck. There’s a point at which new borrowing doesn’t just product less wealth but actually destroys it. The US and China are heading that way fast, while Europe might be there already.

As Evans-Pritchard, notes, the result is “maximum vulnerability.”