by jessefelder

A couple of weeks ago Berkshire Hathaway held its annual shareholders meeting known to many as the “Woodstock for Capitalists.” I have never attended (I don’t like crowds) but I’m always curious to know what Warren Buffett and Charlie Munger have to say at the event. The two tweets below struck me as especially poignant right now.

BUFFETT SAYS LONG-TERM BONDS ARE A TERRIBLE INVESTMENT AT ANYTHING CLOSE TO CURRENT RATES cc @TruthGundlach

— Jennifer Ablan (@jennablan) May 5, 2018

“If I had to bet my life on higher or lower inflation, I’d bet a lot higher.”

Via @WarrenBuffett #brk2018 #Berkshire2018

— Lawrence McDonald (@Convertbond) May 5, 2018

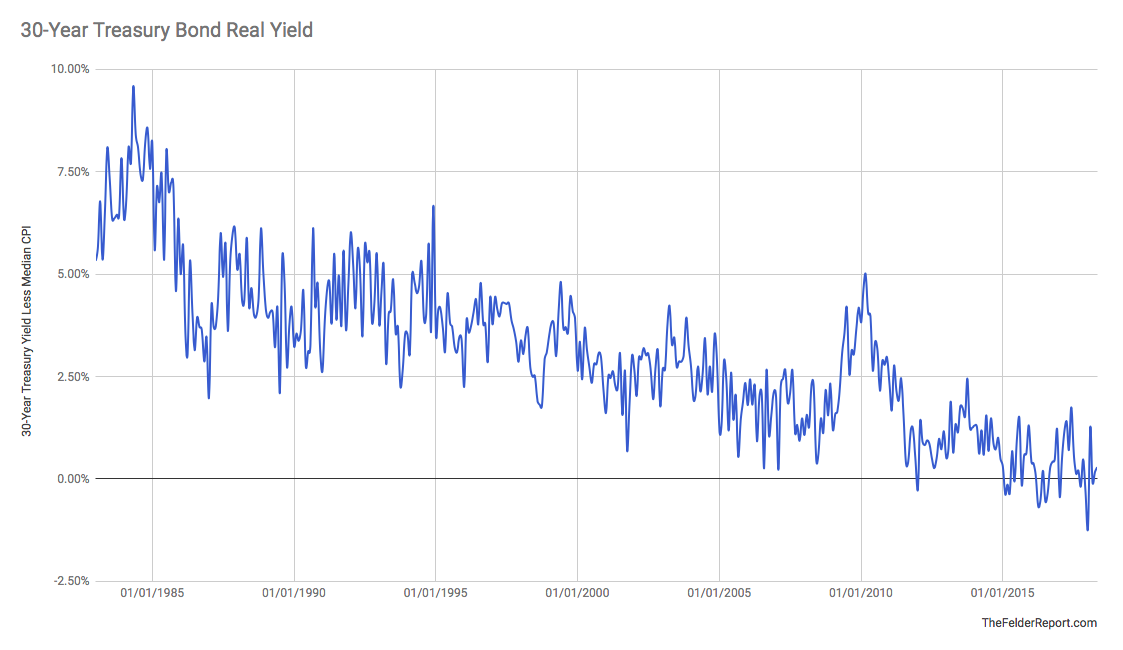

Apparently, the Oracle of Omaha was quoted as saying, “long-term bonds are a terrible investment at anything close to current rates.” I can’t say that I disagree. The real yield on the long bond is essentially zero right now and if inflation picks up over the next three decades, as Buffett expects it to, it will quickly go negative.

But there’s another pair of observations Mr. Buffett has made in the past that should also be considered here. The first concerns comparing the value of bonds to that offered by the stock market: “Though the value equation has usually shown equities to be cheaper than bonds, that result is not inevitable: When bonds are calculated to be the more attractive investment, they should be bought.” -Warren Buffett, 1992 Berkshire Hathaway Chairman’s Letter

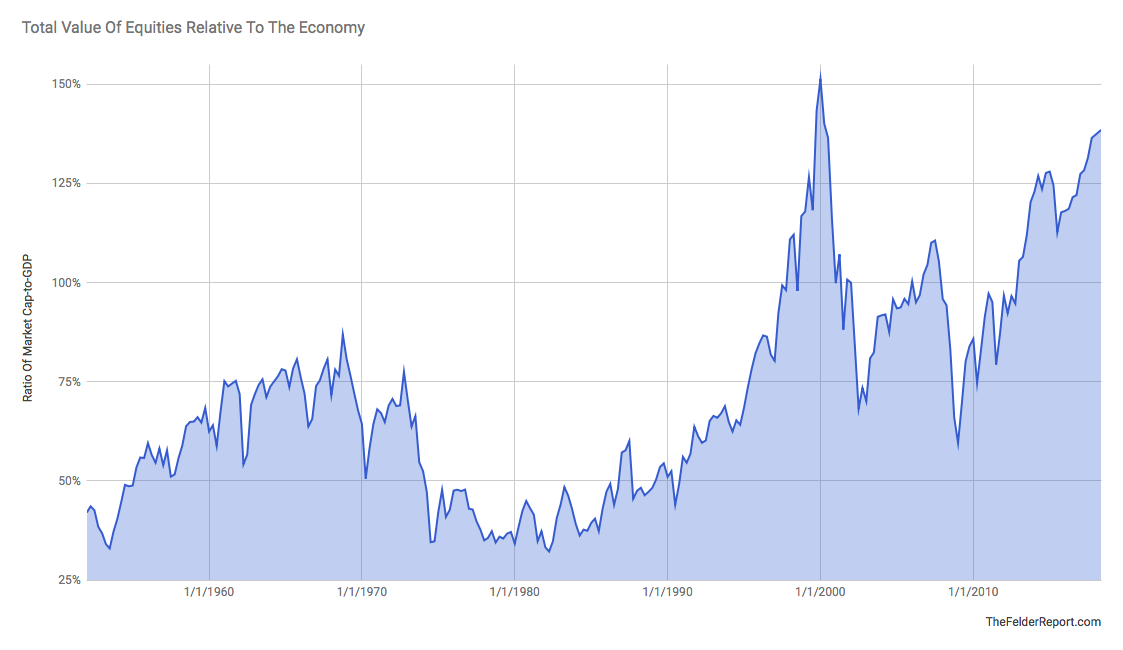

Bonds offer a static yield so their forward return, at least in nominal terms, is known but how do we determine what stocks offer over a specific period? Here is where his second observation comes in. A while back Buffett suggested the ratio of the total value of equities relative to the size of the economy as, “the single measure of where valuations stand at any given moment.”

What makes this measure most valuable is the fact that it is so highly (negatively) correlated with future 10-year returns in the stock market. There is no better visual representation of my favorite Buffett quote of all: “the price you pay determines your rate of return.” Pay a low price, get a high return and vice versa. Investors today are paying very close to the highest prices in history thus will inevitably receive some of the lowest returns on record.

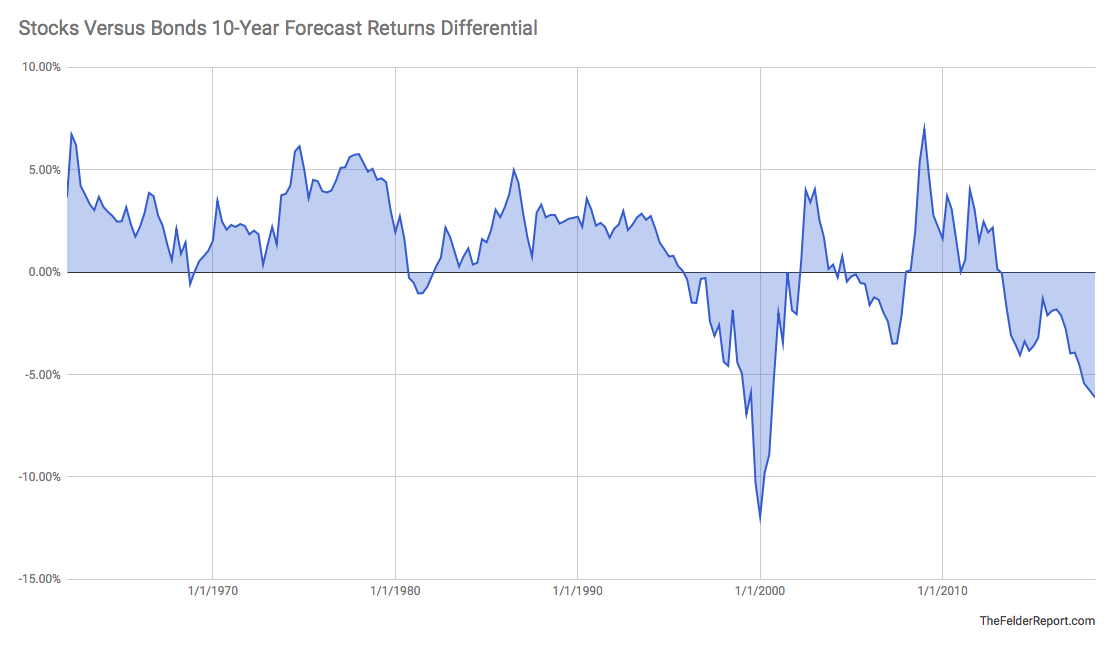

How low? According to the Buffett yardstick, stocks are currently priced to deliver an annualized return of -3% over the next decade including dividends. Compare this to the 3% yield on the 10-year Treasury note and you’re looking at a -6% differential.

Look at that chart above and you’ll immediately see what Buffett meant when he said, “Though the value equation has usually shown equities to be cheaper than bonds, that result is not inevitable.” For the 30 years prior to his writing this in 1992 stocks consistently were priced to deliver higher returns than bonds.

Today, that’s clearly not the case. In fact, since then it’s been more common than not to see the relative value equation lean towards bonds. Even considering this change stocks are now priced such that they are extraordinarily unattractive relative to bonds. In other words, if bonds are a “terrible investment” stocks are at least as bad at today’s prices.

And inflation is, indeed going to make a comeback, as Buffett suggests, investors will want to make sure they limit their exposure to both kinds of financial assets. Additionally, they will want to ensure that they have adequate exposure to other asset classes, most importantly real ones.