We are in the winter of household finances. The “Fourth Turning” is upon us, as we explore how to navigate an uncertain future and maintain financial stability.

To everything there is a season and a time to every purpose under the heaven. – Ecclesiastes 3.

William Strauss’ and Neil Howe’s seminal tome – The Fourth Turning: An American Prophecy – What the Cycles of History Tell Us About America’s Next Rendezvous with Destiny – is a popular read among the RIA Advisor team. We reference it often, especially as the premise of The Fourth Turning grows increasingly prevalent.

As there are seasons to life, there are periods of heat and freeze to a culture – eras of discovery, turmoil, tranquility, war. Winter is the powderkeg. The cold front began in 2007. At grassroots levels, we must prepare for the coldest of seasons to follow that will last through 2030.

Households must gain a renewed level of resolve and prepare financially for a harsh cycle. The wheels of cultures turn from ‘Crisis’ to ‘Awakening’ and back again to ‘Crisis,’ with astounding regularity. A new round of time doesn’t fade into the good night. On the contrary: Sharp breaks or razors of transition are common as cultures traverse seasons of time.

Although the penning of this book was in 1997, it eerily predicts the events we witness today. The current turmoil isn’t unusual. Over the last five centuries, Anglo-American society has entered a new era or turning approximately every two decades. At the start of each turn, people change how they feel about everything – themselves, the future, the very foundation of the nation.

The Fourth Turning

Each turn spans eighty to one hundred years and represents a seasonal rhythm of growth, maturation, entropy, and destruction. The Fourth Turning is Crisis, an era of secular upheaval where the old civic order replaces the new. Winter is history’s greatest break between one season and another.

Previous estimates suggested winter would start around 2005 when remnants of the old social order would disintegrate, political and economic trust would implode. Severe distress would ignite questions of class, race, nation and empire. Americans would share a regret about recent mistakes and correct them, although harshly. I believe winter began with the Great Recession in 2007. The authors’ estimation is not far off.

The survival of the nation will feel at stake. Per the book, before the year 2025, America will pass through a great historical gate commensurate with the American Revolution, Civil War, and twin emergencies of the Great Depression and World War II.

In ‘Crisis,’ the risk of catastrophe is high. A nation in ‘Crisis’ can ignite into insurrection or civil violence, break apart geographically or succumb to authoritarian rule. If war arises, it will be total and all consuming. It will ratchet up the willingness to use greater technologies of destruction.

Winter Of Finances

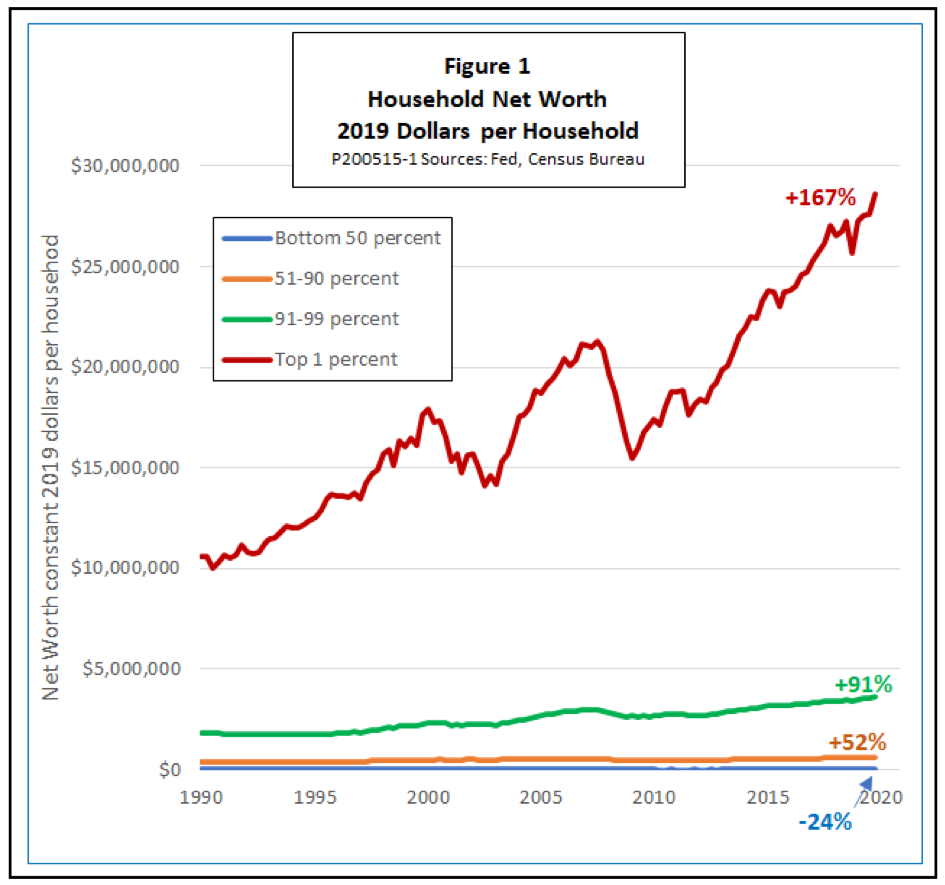

Winter has formed. The great wealth and income inequalities are fueled by Central Bank policies coupled with structural publicly-traded corporate actions of malinvestment. These initiatives placed employee wage and career growth on the backburner for decades.

In 2009, I was extremely worried how unrest would grow strong if nothing changed. Many of the issues that concern me began as early as the late 1980s. They accelerated post-Great Recession. Close to 50% of households have never recovered financially.

Chart courtesy of the Niskanen Center.

The Great Divide

I’ve been impressed with overall analysis by the Niskanen Center. Their recent commentary – How Fragility of Household Wealth Threatens the Economic Recovery, is worth a read. Lance Roberts has written of this topic, extensively.

Keep in mind, the stock market isn’t the economy. Per Federal Reserve analysis, the wealthiest 10% of U.S. households own close to 90% of all stocks and mutual funds. Less than 50% of families who lost a job due to the pandemic, can raise $400 bucks in an emergency.

I want to make sure your family’s finances survive. Many advisors will remain complacent. Not our style. The design of the next war plan will require hours spent at dining room tables where revolutionary ideas are forged and followed.

I am certain the majority of readers of RIA have already considered additional, even unconventional, household finance austerity measures. If so, please communicate your habits, share the following ideas with loved ones and friends who may not be as disciplined:

A Revolution & Revitalization Of Household Finances

So, have you scheduled your colonoscopy? How’s the diet going? How much weight have you lost? How many hours of sleep do you get a night? Welcome to client/advisor conversations of the future. And the future is now.

It’s easy to comprehend how unhealthy people accumulate less wealth, may be forced to retire sooner and suffer shorter life expectancies. If anything, being unhealthy in retirement even if one has the finances, makes for an emotionally challenging existence.

Based on COVID, we have yet to estimate the long-term costs to Medicare and Medicaid as workers retire sooner which portends to continued above-average inflation, possibly close to 7% for Medicare Part B premiums, Medigap supplemental coverage and Medicare Advantage. As advisors, our group is increasingly vigilant when it comes to monitoring of information that requires us to alter our inflation estimates for financial plans.

The Financial Cost Of Being Unhealthy

According to De Nardi, Pashchenko and Porapakkarm authors of NBER Working Paper 23963 The Lifetime Costs of Bad Health, unhealthy people accumulate substantially less wealth than healthy people. Among 65-year-old males with a high-school degree, the median wealth of healthy individuals is almost twice that of those who are unhealthy – $230,000 vs. $120,000 in 2015 dollars.

Per Fidelity Investments, the average couple will spend a total $280,000 in today’s dollars for medical expenses throughout retirement not including long-term care. In retirement, I’ve witnessed unhealthy couples spend close to half of their annual income on healthcare costs which includes Medicare premiums plus out-of-pocket costs. I’ve seen their annual inflation rates hit close to 6% and the quality of their retirements deteriorate.

For me, it was a wake-up call to make dramatic improvements to my health habits over three years ago. I don’t want a retirement, especially if I need to continue to work saddled by poor health. Nor do I want to witness clients go through a lifetime of hard work just to face a poor-quality retirement.

Start With The Basics

You can make dramatic improvements to battle the top 3-most common health issues we face in America: Lack of physical activity, being overweight or obese, and tobacco usage. Improvements in these areas are squarely in your control. Like a financial discipline to pay yourself first, small, steady improvements over the years can lead to big results.

When people come to me to help analyze their spending habits and create a budget, I make sure to discuss the importance of additional spending on high-quality, unprocessed foods. Many seek to cut the gym expense. I outline the importance of continuing the membership. I look for ways for people to invest in a personal trainer and possibly a nutritionist to hold them accountable.

A Mental Trick

I created a mental trick that helps keep my long-term financial and physical health on the right track and at the forefront of my thoughts. Before I indulge in an activity, I mentally increase or reduce my retirement savings by $100. For example, if I trade out a burger and fries for a salad, I add $100. If I’m about ready to indulge in something unhealthy or miss a workout, I subtract $100. All this mental ruse compels me to halt, consider what I’m about to do, and operate less on impulse.

At the end of the week, I review my additions and subtractions. The goal is to finish the net positive. Some weeks, I’m 100% positive and reward myself with a treat. It’s at the point where this mental accounting exercise is on auto-pilot and has been highly useful to keep me on a healthy path.

One of the positive trends emerging from the COVID crisis is the focus of families on physical activity. Bike sales are through the roof; Peleton’s revenues are higher. Kids are outside instead of cooped up with electronics. All good!

People lament that it’s expensive to eat healthily. I may have found a solution. I purchase fresh produce and other foodstuffs from http://www.imperfectfoods.com. Listen, this is the misshapen apple, the dented eggplant, grocery, and farm overstock. I customize my basket and timing of delivery. Upfront, I chose the grocery plan that fit my lifestyle, selected the groceries, and their service delivers to my door. They provide suggestions; I adjust, add or reduce items weekly as needed. Overall, very affordable and convenient. Check it out!

Household Debt-To-Income Ratios Are Dangerous

Touted mortgage and financial industry ratios are ridiculous. They’re designed to extend the latitude of consumerism and ultimately place households into more debt. They’re not designed to fortify fiscal health. You must ignore them and redefine the financial boundaries of your household.

The standard rule is a house payment shouldn’t exceed 28% of pre-tax income. It’s a horrible rule. It’s designed to push the boundaries on cash flow and sell you more house than necessary. Throw it out if you desire financial flexibility, cash to cover emergencies and save for a prosperous financial future. Dave Ramsey suggests 25% of after-tax income. Not bad. However, you can do better.

Our rule at RIA is a total mortgage payment should not exceed 15% of after-tax income.

A Personal Example

I didn’t extract this percentage out of thin air. I’ve watched how households over the last two decades who utilized this rule continue to increase their wealth by thinking of a primary residence as a place to live, not an investment. In other words, an intimidating mortgage obligation was just too painful for couples who employed long-term consideration of other important goals they sought to fund. I isolate my mortgage, HOA, and homeowner’s insurance payments and divide the sum by my ‘take-home’ monthly income. Currently, my ratio is 7.6%.

I then consider my household’s variable and specific fixed expenses – entertainment, groceries, clothing. I also examine costs for utilities, car insurance (not cheap with a college-bound daughter driving). The general rule is 30% of after-tax income for ‘wants.’ Obviously, auto insurance is a need, not a want. However, with the ability to shop around for better rates or utilize insurance company ‘drive-pay’ programs which reward responsible drivers, I place auto insurance into the variable category.

Currently, my variable expenses are 10% of monthly after-tax household income. I understand I no longer have a household with young children where variable expenses are greater. However, that doesn’t mean as a growing family, you shouldn’t create your own rules which still allow financial ‘breathing room.’

At RIA, we believe variable monthly expenses shouldn’t exceed 20% of after-tax income.

It’s time to do simple math and manage household debt-to-income ratios with ongoing vigilance.

Get Educated About Social Security

According to a working paper by Andrew G. Biggs, ‘How the Coronavirus Could Permanently Cut Near-Retirees’ Social Security Benefits,’ for the Wharton Pension Research Council, some groups of near-retirees are likely to suffer substantial permanent reductions to their Social Security Retirement benefits.

Those born in 1960 or later could see annual benefits in retirement reduced by around 13% with losses over their retirement period by close to $70,000. The basis of the assumption was a 15% decline in the Social Security Administrations measure of economy-wide average wages in 2020.

The Social Security benefits formula examines an individual’s highest 35-years of earnings and the National Average Wage Index (AWI) to calculate a worker’s PIA or Primary Insurance Amount. ‘Bend points’ in the formula are usually increased along with average wages in the economy. For the 1960 birth cohort, the bend point values used to calculate benefits will be equal to those in 2020, adjusted by the growth of the Average Wage Index between 2018-2020. For 2018, the most recent year for data available, the AWI was $52,146. The projection for 2020 in the Social Security Trustees’ Report was to be $56,396 – 8% higher!

The 2020 Impact

A significant decrease in the 2020 projection would reduce Social Security benefits for future recipients age 60 or younger. Those age 62 or older and current benefit recipients are not affected by changes to the AWI. I believe the author is too conservative when it comes to the negative long-term effects of the pandemic on the Average Wage Index. I foresee a challenge with wage growth over the next five years, which means the AWI estimates may decrease again. The possibility of this event requires close monitoring for financial planning purposes.

Also, retirees and their financial partners need to remain aware of the overall state of Social Security, which is funded primarily by payroll taxes. Payroll taxes may be cut for a period by Congress and the Executive Branch or simply by less of the population working and paying in over an extended period. Per Alicia H. Munnell, Director at the Center for Retirement Research at Boston College, the sudden collapse in payroll taxes due to COVID-19 may accelerate the depletion of the trust fund by two years – 2033 – which means benefits could be reduced by 25% at that time.

It’s crucial for financial professionals to keep abreast of the pandemic’s economic aftermath and to determine whether financial plans maintain an adequate level of guaranteed income to compensate for future changes.

Household Cash Flow Will Remain Uncertain

The priority is to start a Financial Vulnerability Cushion for as long as it takes to accomplish the task. As a general rule, we consider a year’s worth of living expenses in cash, an adequate goal. Why? We believe chronic underemployment will be an ongoing concern as business trends change and companies seek to radically reduce the cost of labor due to lessons learned during the pandemic.

Currently, investors are allowed to distribute from retirement accounts without penalty to survive the pandemic’s financial destruction. Prospective first-time homebuyers are permitted to raid retirement accounts for down payments. My view? If you need to reduce retirement funds to buy a house, you can’t afford it.

The financial services industry has always aggressively peddled investors fund contributions to pre-tax accounts above all else. Such leaves households with very little liquid savings to tap in case of emergencies or even worse, financial vulnerabilities. Our rule at RIA – Households require 3-6 months of living expenses in cash, to cover unexpected events – car repairs, etc. You get it.

However, our team over the last six months has communicated over the radio and in meetings, the importance of an additional six months of savings to cover the serious stuff – job loss, major illness. This rule is more important than ever in the face of ongoing uncertainty.

I implore readers to consider this initiative before funding retirement accounts. In case of longer-term household cash flow disruption, retirement accounts can remain intact for the stated goal – RETIREMENT. Naturally, if an employer match is offered (matches have been placed on hold at many organizations), fund a retirement plan enough to capture it. Direct the rest of your savings into a FVC. Investigate online, FDIC-insured savings accounts with higher yields such as http://www.marcusbank.com and http://www.synchronybank.com.

Be Increasingly Sensitive To Spending

I love westerns, especially “The Big Valley.” Rich story lines and robust acting by Barbara Stanwyck as the matriarch of the Barkleys, along with Lee Majors and Richard Long as members of a California ranching family, have captivated me for years.

Your spending in retirement is mostly a big valley. I’ll explain:

Several of the Certified Financial Planners at RIA partner with clients who have been in retirement-income distribution mode for over a decade. In other words, these clients are re-creating paychecks through systematic portfolio withdrawals and Social Security/pension retirement benefits. Although we formally plan for an annual cost-of-living increase in withdrawals, rarely if at all does this group contact us every year to increase their distributions!

There’s a time series in retirement where active-year activities, big adventures conclude, and retirees enter the big valley of level consumption. I call it the “been there done that,” stage where a retiree has moved on; the overseas trips have been fulfilled and enrichment thrives a bit closer to home.

Retirees move from grandiose bucket list spending to a long period or valley of even-toned, creative, mindful endeavors. It’s a sweet spot, an extended time of good health; so, healthcare is not so much an inflationary or heavy spending concern. The big valley stage is just a deeper, relaxed groove of a retirement lifetime.

Inflation Is Real

I often refer to a thorough analysis, as it reflects the reality I witness through clients, conducted by David Blanchett, CFA, CFP®, and Head of Retirement Research for Morningstar. The research paper, “Estimating the True Cost of Retirement,” is 25 pages and should be mandatory reading for pre-retirees and those already in retirement (along with financial professionals).

David concludes:

“While research on retirement spending commonly assumes consumption increases annually by inflation (implying a real change of 0%), we do not witness this relationship within our dataset. We note that there appears to be a “retirement spending smile” whereby the expenditures actually decrease in real terms for retirees throughout retirement and then increase toward the end. Overall, however, the real change in annual spending through retirement is negative.”

David eloquently defines spending as the “retirement spending smile.” As a fan of westerns, I envision the period as a valley bracketed by the spending peaks of great adventures on one side and healthcare expenditures. Hey, I live in Texas. This analogy works better for me.

In comprehensive financial planning, it’s prudent to incorporate an inflation rate to each spending need.

Medical costs affect retirees differently. Unfortunately, it’s tough as we age to avoid healthcare costs and the onerous inflation attached to them. Thankfully, proper Medicare planning is a measurable financial plan expense as most retirees’ healthcare costs will are covered by Medicare and Medigap or supplemental coverage.

Retirees Aren’t Prepared Financially

Unfortunately, many retirees are ill-prepared for long-term care expenditures which are erroneously believed to be covered by Medicare. Generally, long-term care is assistance with activities of daily living like eating and bathing. At RIA, we use an annual inflation factor of 4.8% for additional medical expenses (depending on current health of the client), and the cost of long-term care.

David suggests an alternative inflation proxy for older workers. The Experimental Consumer Price Index for Americans 62 Years of Age and Older or the CPI-E, reflects contrast of category weightings when compared to CPI-U or CPI-W, the CPI for urban consumers and urban wage earners, respectively.

Unfortunately, don’t expect CPI-E to gain traction as it would result in robust COLA or cost-of-living adjustments to Social Security benefits. Intuitively, it makes sense that greater relative importance is placed on medical care for seniors. However, based on the burden of social programs on the federal budget, don’t expect CPI-E to be employed anytime in the foreseeable future.

An Important Caveat

Inflation is indeed the omnipotent boogeyman in the room and must be addressed. Due to globalization, technological advancement, increased competition and decreased domestic energy dependence, inflation overall has progressively trended lower for decades (thankfully).

An important caveat – Although the overall landscape is deflationary, there are cold, inflationary winds stirring. First, there’s the possible impact of COVID on future healthcare premiums. Second, the costs of sanitary measures will pass on to consumers. Last, the cry for domestic production grows stronger daily. All this has the potential to impact inflation in a way we have rarely witnessed. The situation warrants monitoring.

Those with life expectancies that exceed the mortality tables need to take extra care to ensure against the risk of possibly higher living expenses through the use of reverse mortgages and long-term care insurance options.

Per the book, the outlook isn’t all dire. Every cycle creates a Phoenix from the ashes: Innovation, opportunity.

We all just need to survive a hard winter.

I hope I’ve provided protection tips to weather your families through the imminent storm.