Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

The soothingly low mortgage delinquency rate is a deceptive indicator: the New York Fed weighs in.

Mortgage delinquencies at all commercial banks in the US inched down to 3.14% in the second quarter, the lowest since Q2 2007, according to the Federal Reserve. But after those soothingly low delinquency rates in 2007, something happened. By Q3 2008, the delinquency rate hit 5.2%, and in Q4 2009, it went over 10%, and stayed in the double-digits until Q1 2013. This was the mortgage crisis. And we’re a million miles away from it, thank God. Or are we?

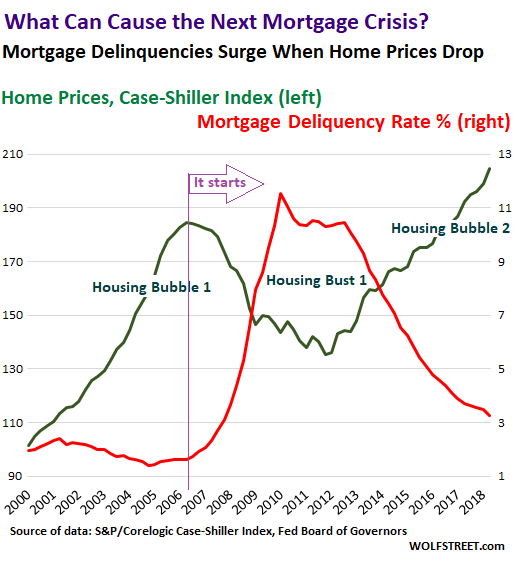

This chart compares home prices in the US (green, left scale) to delinquency rates (red, right scale). Delinquency rates started surging after home prices started falling. The inflection point is marked by the vertical purple line, labeled “it starts”:

Home prices began falling in 2006. By 2008, some homeowners were seriously “underwater” – they owed more on their house than the house was worth. When they ran into financial trouble because they were in over their heads, or because one of the breadwinners in the household lost their jobs, or because they’d lied on their mortgage application and never had enough income to begin with, or because they were investors who couldn’t make the math work out anymore, or whatever, they were stuck.

In a rising housing market, they would just sell the home and pay off the mortgage. But they couldn’t sell their home because it was worth less than the mortgage, and default was the only option.

The chart above shows the relationship between home prices and delinquencies. In a rising housing market, delinquencies will always be low but are not an indicator of future default risks. But home prices are an indicator of default risk.

“Borrowers’ ability to withstand economic shocks depends importantly on housing equity,” the New York Fed explained in its new Economic Policy Review. “This dynamic played a key role in the 2007-09 recession, when surging mortgage debt followed by falling home prices put many homeowners ‘underwater’ on their mortgages.”

When home equity turns “negative,” that’s when serious trouble begins. The New York Fed:

Over the first half of the 2000s, U.S. household debt, particularly mortgage debt, rose rapidly along with house prices, leaving consumers very vulnerable to house price declines. Indeed, as house prices fell nationwide from 2007 to 2010 and unemployment rates soared, mortgage defaults and foreclosures skyrocketed because many households were “underwater”…

But the national averages don’t do a good job. About a third of homeowners own their homes free and clear, and there is no risk associated with them. Another third of homeowners owe relatively small amounts or very manageable amounts on their homes, after years of having made payments without cash-out refinancing. And they’re not a risk factor either. They can always sell their home and pay off their mortgage, even if home prices drop 40%.

The risk lies at the remaining third of the homeowners, the most vulnerable, the most leveraged, those that bought recently at the highest prices, those that refinanced to cash out their home equity….

Then there’s the issue of home prices dropping a lot more in some regions – and this is averaged out in the national statistics. The New York Fed (emphasis added):

At a more disaggregated level, the time series of our leverage metrics clearly reflect the dramatic regional home price dynamics that others have observed, with the widest swings in prices found in the “sand states”: Arizona, California, Florida, and Nevada. Studying these states illustrates one of the key lessons from our analysis: Looking at measures of leverage based on contemporaneous housing values will often lead one to misestimate the vulnerability of a housing market to shocks.

Homeowners in the sand states were much less levered in 2005 than those in other regions, yet as home prices reverted to their mean, the leverage of these homeowners rapidly increased and extremely high mortgage defaults followed.

The paper warns: “Most importantly, higher leverage, and in particular a household being underwater on its mortgage(s), is a strong predictor of mortgage default and foreclosure.”

In fact, according to research cited by the paper, negative equity is a “necessary condition” for mortgage default:

Negative-equity loans represent a pool of default risks: If the borrowers are hit with liquidity shocks resulting from, say, a lost job, then default may be the only viable option. Positive-equity borrowers faced with liquidity shocks, on the other hand, are generally able to sell the property and avoid default.

Thus, “household leverage” blowing out is not a function of the mortgage, which doesn’t change much, but a function of the home price, which can decline sharply. This increases household leverage due to market forces, without even any input from the household. It happens on a case-by-case basis, and the national averages fail to predict this condition.

Even if they don’t default, households that have become overleveraged due to declining home prices impact the broader economy, the New York Fed points out:

- They may cut back consumption in response to a negative shock, in part because they lack “debt capacity” that could help them smooth consumption.

- They’re often unable to refinance to take advantage of lower mortgage rates.

- They may reduce spending on property maintenance or investments.

- The may not be able to move when opportunities arise for them elsewhere.

- High leverage in conjunction with down-payment requirements further reduces transaction volume and prices, “thereby generating self-reinforcing dynamics.”

And the differences, as real estate in general, are local, according to the report: “In cities where more homeowners are highly leveraged, house prices are more sensitive to shocks (such as city-specific income shocks).”

It all boils down to this: There can be no mortgage crisis unless home prices decline enough in some markets. And given how inflated home prices are in many markets, and that mortgage rates are now climbing, any reversion toward the mean of home prices in those markets would cause the delinquency rate to do a beautiful “déjà-vu all over again,” so to speak. That low national delinquency rate these days, often touted as a sign of low risk in the housing market, has zero meaning as an indicator of risk for the most vulnerable households when the prices of their homes begin to drop.