Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Five companies blow $55 billion in Q1 to prop up their own shares.

Apple was once again the biggest share buyback queen of them all: In the first quarter of 2019, it spent a new all-time record of $23.8 billion on buying its own shares, apparently because everyone else was selling them, and someone had to buy.

Over the past four quarters through March 31, Apple spend $75.1 billion on share buybacks to prop up its own shares, according to the latest report by S&P Dow Jones Indices. But Apple’s shares remain 16% below their peak last October. Over the past five years, Apple spent $284 billion on share buybacks.

When a company buys back its own shares, the shares get canceled and disappear, the cash used to buy them gets handed to sellers and is gone, and “stockholder equity” on the balance sheet drops by that amount.

Buybacks are at the core of financial engineering: They lower the share count, and so earnings are divided by a smaller number of shares, which generates a larger earnings-per-share figure, and a lower price-earnings ratio, to bamboozle people who still bother to look at these metrics after 10 years of being told that fundamentals don’t matter.

Share buybacks also cover up the dilutive effects of stock-based compensation plans and stock-based acquisitions of companies that have no earnings, such as startups, that Apple and others constantly gobble up.

Apple still has a rock-solid balance sheet and can afford to blow this kind of money. Other companies are not so lucky; nevertheless, they did blow a ton of money on share buybacks.

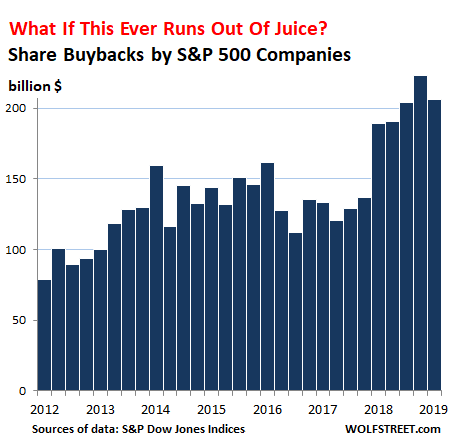

In total, companies in the S&P 500 index spent $205.8 billion in Q1, the biggest first quarter ever, the second biggest of any quarter ever, and up 8.9% from Q1 2018, but down 7.7% from the all-time dizzying record in Q4 2018:

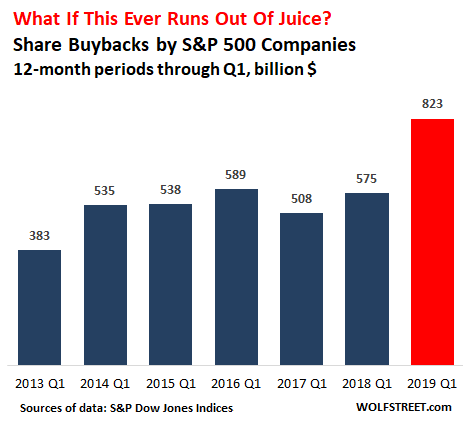

Over the past 12 months through March 31, share buybacks jumped 43% from the prior 12-month period, to a record $823 billion. And it’s adding up: Since 2012, share buybacks have totaled $4.03 trillion, which is about the magnitude of Germany’s annual GDP. The chart shows share buybacks for each 12-month period through Q1:

Higher share prices in Q1 than in Q4 – less bang for the buck – and the 7.7% decline in share repurchases in Q1 from Q4 resulted in 20% fewer shares being repurchased in Q1 than in Q4. The share count dropped in aggregate by 0.94% down from a 1.18% drop in Q4.

The buybacks are “top heavy,” with only five companies accounting for $55 billion, or 27%, of total buybacks in the quarter:

- Apple [AAPL]: $23.8 billion in Q1; $75.1 billion over the 12 months.

- Oracle [ORCL]: $10.0 billion in Q1; $35.3 billion over the 12 months.

- Pfizer [PFE]: $8.9 billion in Q1; $15 billion over the 12 months.

- Bank of America [BAC]: $6.3 billion in Q1; $21.5 billion over the 12 months.

- Cisco Systems [CSCO]: $6.1 billion in Q1; $22.8 billion over the 12 months.

And it’s getting increasingly top heavy: The top 20 share buyback queens – of the 389 companies that reported share buybacks in Q1 – accounted for 51% of total share buybacks in Q1, up from 41% during the 12-month period, and up from 36% in the prior 12-month period.

The tax cut did it. Obviously, everyone knew what would happen: Passed under the pretext of encouraging US corporations to “repatriate” their previously untaxed overseas profits and invest them in the US to produce more in the US and to hire more people in the US and to move the US economy forward, these provisions of the corporate tax cut have instead led to a tsunami of share buybacks.

Everyone knew in advance it would happen, despite rhetoric to the contrary, and so share prices surged first in anticipation of a tsunami of share buybacks and then as a result of it. And when the selling went wild last year, shares plunged less because there were buyers out there, buying back their own shares, at the highest possible prices with relentless bids whose sole purpose was to drive up the price of the shares they were buying.

But these profits registered in overseas mailbox entities that are being “repatriated” for share buybacks are not endless, and they’re being drawn down. And borrowed money that is also used for part of these share buybacks requires loosey-goosey credit markets, which we have now, but credit cycles turn, and when investors in bonds and leveraged loans get burned, they tighten the screws, and borrowing money to blow on share buybacks gets tough.

The Fed has already accomplished more with its verbiage this year than it had last time when it cut rates all the way to zero and did trillions of dollars of QE. My podcast.… THE WOLF STREET REPORT: Stealth Stimulus Has Arrived