One of the economic forces of 2022 has been the strength of the US Dollar and its impact on the rest of the world. There was something of a symbolic move yesterday as the Japanese Yen moved through 140 and indeed another one with the Euro falling through parity although a little care is needed with the latter because that is in film terms take three. The Federal Reserve calculates a broad trade-weighted or effective index and it is 123.2 whereas a year ago it was 113.8. Whilst that may bit seem a lot it has had quite an impact.

Reserve Currency

At a time of both rising and high inflation US Dollar strength exacerbates the problem for everyone else. Whilst we get plenty of talk about other currencies replacing the US Dollar the reality is that all the main commodities are priced in it. Thus the rest of us find ourselves paying more for basic commodities due to our currencies being weaker. The situation is asymmetric because the US gains very little. In explicit terms it gains nothing because one dollar remains one dollar but there may be implicit business gains due to others seeing higher costs and inflation. Those may be offset and indeed more than offset by US goods becoming more expensive abroad.

Debts in US Dollars

This is an issue because the debt has just got more expensive in other currencies. This is really rather awkward because the reason you issue in US Dollars is often a lack of faith in the domestic currency and thus there is a real danger of a downwards spiral.

Last summer the St. Louis Fed looked at the numbers. South America is one area of concern.

Compared with Asian countries, countries in Latin America have a much higher proportion of U.S. dollar-denominated debt. At the aggregate level, issued dollar-denominated debt makes up around 17% of total government debt in select Latin American economies,3 which far outstrips the 3% in select Asian economies. Moreover, for some countries, such as Colombia and Argentina, the share of dollar-denominated debt is even higher: Over 30% of government debt in Colombia and 55% of government debt in Argentina were issued in dollars.

As Asia gets a mention here are the main issues there.

Although only a small portion (less than 5%) of government debt is denominated in U.S. dollars for most of these economies, it is not the case for Israel, Indonesia and Saudi Arabia.2 For these three countries, over 10% of their government debt is dollar denominated.

Saudi Arabia is a special case in that via its energy resources it is hardly short of US Dollars right now! There is another issue which they do not cover but comes to mind as I note this from them.

Hong Kong is one with a notably increasing share of dollar bonds.

At 5% that may be an issue with the US Dollar peg but we also know that corporate China has been borrowing in US Dollars with its property sector in the van. I recall this from CNBC.

Between 2016 and 2020, the industry’s value of offshore U.S. dollar bonds grew by 900 billion yuan ($139.75 billion) — that’s nearly two times the growth of 500 billion yuan in onshore yuan bonds, according to Nomura.

As it happens we are seeing a slowing property market making things more difficult. I have pointed out before that I believe China is managing its currency to resist the US Dollar strength.

Then there is the issue of Turkey which we have noted on various occasions. From the Turkish central bank.

Short-term external debt stock recorded USD 134.8 billion at the end of June, indicating an increase of 10.9 percent compared to the end of 2021. Specifically, in this period, banks’ short-term external debt stock increased by 8.9 percent to USD 56.0 billion and other sectors’ short-term external debt stock increased by 12.0 percent to USD 49.4 billion.

It is not all in US Dollars as there re for example loans in Euros.

Private sector’s total outstanding loans received from abroad recorded USD 161.4 billion as of June, decreasing by USD 7.6 billion. With regards to the maturity, long-term loans recorded USD 153.7 billion as of June, decreasing by USD 7.8 billion; whereas short-term loans (excluding trade credits) realized USD 7.7 billion, increasing by USD 206 million in comparison to the end of 2021.

This is almost a type of test case as the Turkish Lira has done so poorly versus the US Dollar that international lenders do not want to use it. Which means more US Dollar denominated debt which means the situation is worse next time around. So far the story has been pretty much rinse and repeat.

US Debt

Care is needed because I do not have a vast amount of confidence in the numbers as some holders will not be keen for others to know their position. According to the US Treasury that totaled some US $7.4 trillion at the end of the second quarter. Should they take the funds home there is a currency gain.

Although bonds have not been the best investment in 2022 the traditional method for such holdings is to focus on the shorter-dates.

US Economy

Whilst changes in the exchange-rate have a reduced effect on the US economy they do have an impact. Firstly on inflation.

For example, a typical estimate is that an appreciation of the dollar of 10 percent causes U.S. non-oil import prices to fall only about 3 percent after a year and only slightly more thereafter.

Also on trade.

The low exchange rate pass-through helps account for the more modest estimated response of U.S. real imports to a 10 percent exchange rate appreciation shown by the thin red line in figure 2, which indicates that real imports rise only about 3-3/4 percent after three years.

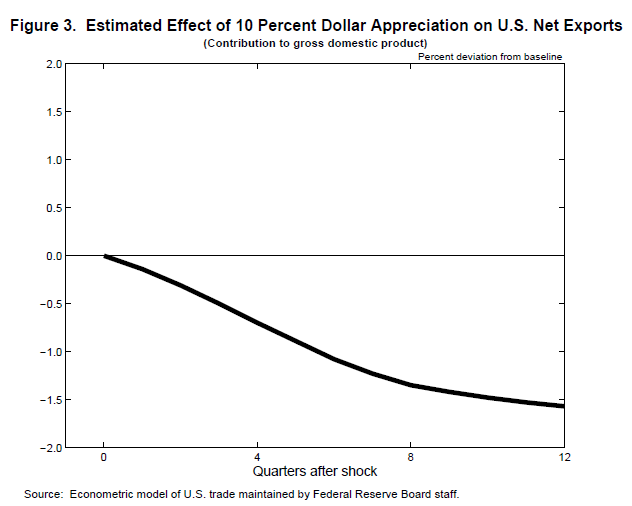

Then on economic output.

Figure 3 uses these results to gauge how a 10 percent dollar appreciation would reduce U.S. gross domestic product (GDP) through the net export channels we have just discussed. The staff’s model indicates that the direct effects on GDP through net exports are large, with GDP falling over 1-1/2 percent below baseline after three years. Moreover, the effects materialize quite gradually, with over half of the adverse effects on GDP occurring at a horizon of more than a year.

{kind=link}

These numbers were given by the then Fed Vice-Chair Stanley Fischer and so far we are seeing a move of the order of 80 per cent of that.

Comment

As you can see the King Dollar phase has a lot of consequences where the one step implications of economic text books are replaced by a sequence of flows. What may look balanced in the aggregate can be quite a crisis in the singular as we have seen in places like Argentina and Turkey. That may yet turn upon the Chinese property market and Hong Kong although China does have reserves on a grander scale.

Next in the chain is interest-rates because this phase has been fed by the relative hawkishness of the US Federal Reserve with its 0.75% increases. Others have followed it and indeed Canada responded with a 1% but it is a case of other central banks following the leader of the pack. So another consequence of the King Dollar phase is higher interest-rates elsewhere with the ECB for example now hinting at an 0.75% increase next week. So they are singing along with Tina Arena for now.

I’m in chains

I’m in chains

I’m in chains

I’m in chains