Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Debt out the wazoo, but someone is still buying it.

The US gross national debt has ballooned by $1.33 trillion over the past 12 months to $21.8 trillion as of December 14, according to Treasury Department data. Over the past six months alone, this debt has ballooned by $740 billion, despite a strong economy: Fueled by a stupendous spending binge and big-fat tax cuts, the government has been increasing its debt at a rate of $123 billion a month on average over the past six months.

But who’s buying all this debt?

US government debt is an income-producing asset for investors — the creditors of the US. And when the pile of US debt increases, by definition, someone has to buy it. But who? China, Japan, and other foreign investors? Nope. They’re shedding this debt. So here we go.

Foreign investors in total reduced their holdings of marketable Treasury securities in October by $25.6 billion from September, to $6.2 trillion, having shed $125 billion since the end of October 2017, according to the Treasury Department’s TIC data released Tuesday afternoon.

Foreign holders of marketable Treasury securities fall into two categories: “Foreign official” holders, such as central banks and government entities; they cut their holdings by $132 billion over the 12 months, to $3.95 trillion. And private-sector investors; they added about $7 billion to their holdings, totaling $2.25 trillion at the end of October.

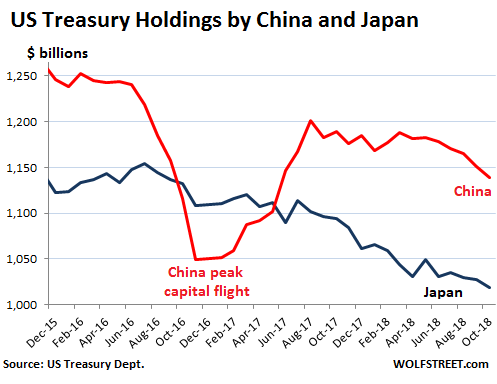

By country, the two biggest holders are China and Japan, but both have been shedding Treasury securities:

- China’s holdings of Treasury securities fell by $50 billion from a year earlier to $1.14 trillion.

- Japan’s holdings fell by $76 billion from a year ago to $1.02 trillion, continuing the trend since the peak of its holdings at the end of 2014 ($1.24 trillion).

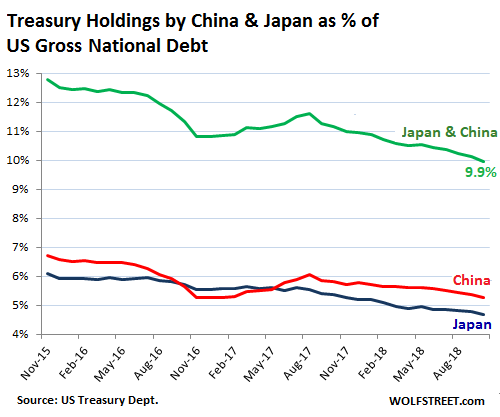

But over the same 12 months through October 31, 2018, as China and Japan reduced their holdings by $126 billion, the US gross national debt soared by $1.26 trillion, to $21.7 trillion, and both countries hold a smaller share of it. China’s holdings (red line in the chart below) accounted for 5.2% of US gross national debt, and Japan’s holdings (blue line) for 4.7%. For the first time since this cycle started many years ago, their combined holdings (green line), at 9.9%, fell below 10% of US gross national debt:

Other Big Foreign Creditors of the US government

Of the 12 largest holders of US Treasuries, after China and Japan, seven are tax havens for foreign corporate and/or individual entities (bold) and one (Belgium) is the location of Euroclear, a massive outfit that provides, as it says, Financial Market Infrastructure services, holds about $32 trillion in assets in fiduciary accounts, and settles about $830 trillion in trades per year for its clients. The value in parenthesis denotes the holdings in July 2017:

- Brazil: $314 billion ($270 billion)

- Ireland: $287 billion ($312 billion) as US corporations “repatriate” their US Treasury holdings — part of the famous “overseas cash.”

- UK (“City of London”): $264 billion ($226 billion)

- Luxembourg: $225 billion ($218 billion)

- Switzerland: $225 billion ($254 billion)

- Cayman Islands: $208 billion ($247 billion). More US corporate “overseas cash” being repatriated?

- Hong Kong: $185 billion ($192 billion)

- Saudi Arabia: $171 billion ($145 billion)

- Belgium: $170 billion ($99 billion)

- Taiwan: $164 billion ($116 billion)

- India: $138 billion ($141 billion)

- Singapore: $133 billion ($30 billion)

Russia has dumped most of its holdings, reducing them from $153 billion in May 2013 to $14.9 billion by May 2018, and has roughly kept them steady at this level. Russia’s Treasury holdings are now among the small fry.

On net, foreign investors reduced their holdings of Treasury securities in October by $125 billion from a year ago to $6.2 trillion.

So who is buying?

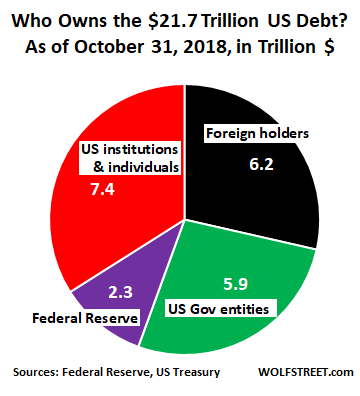

So let’s see. Over the 12-month period ended October 31, the US gross national debt rose by $1.26 trillion, to $21.7 trillion. Here’s who bought or shed this paper over those 12 months:

- Foreign holders (official and private-sector) shed $125 billion, whittling down their stake to $6.2 trillion, or to 28.6% of the total US national debt.

- US government entities (pension funds, Social Security, etc.) increased their holdings by $168 billion to 5.9 trillion. This “debt held internally” is owed the beneficiaries of those funds; it’s their money, invested in Treasury debt, and the US government owes every dime of it. They now hold 27.0% of the total US national debt.

- The Federal Reserve shed $190 billion over the 12 months through October as part of its QE Unwind, reducing its pile to $2.27 trillion by the end of October, or to 10.5% of the total US national debt.

- American institutions and individual investors increased their holdings by $1.41 trillion, directly and indirectly, through bond funds, pension funds, and other ways. Banks are very large holders of Treasury debt. Together, all these entities combined owned the remainder, $7.37 trillion, or 34% of the total US debt!

This is how the gargantuan US debt is carved up as of October, in trillion dollars:

The simple fact that long-term Treasury yields have been low relative to short-term yields (which are more responsive to Fed rate hikes), and that the yield curve has become nearly flat shows just how much desperate buying-pressure there is, especially when there is turbulence in the stock market and investors seek the safety of Treasury debt.

The 10-year yield, while up sharply from a year and two years ago, has been vacillating between 2.8% and 3.25% since early February. The massive buying-pressure in the Treasury market, in part triggered by stock-market sell-offs, has been easily mopping up the flood of new Treasury debt that the government has been issuing at an average rate of $123 billion a month over the past six months.

But foreign investors, as alluring as these Treasury yields may be in a negative-interest-rate world, would take on currency risk, and hedging against it has become prohibitively expensive at current Treasury yields.