Are you one of the 8 million consumers who noticed a credit score improvement and wondered how it happened?

Here’s the scoop:

Beginning in March 2015, The National Consumer Assistance Plan, a consortium of the three major consumer credit reporting companies – TransUnion, Experian and Equifax, began an effort to make credit reports more accurate and make it less intimidating for consumers to correct errors. The three-year initiative outlined the following objectives:

- Allow consumers to access a free credit report sooner than 12 months if a dispute that causes a modification is initiated. This change provides consumers the window of opportunity to verify that modifications have been completed.

- Medical debts won’t be reported until a 180-day waiting period which allows insurance payments to be applied. Past medical collections that have been paid by insurance will be removed.

- Unpaid traffic, parking tickets and fines will no longer appear on credit reports.

- Consumers who are victims of fraud will receive improved communications about credit report disputes and additional options to rectify fraud situations.

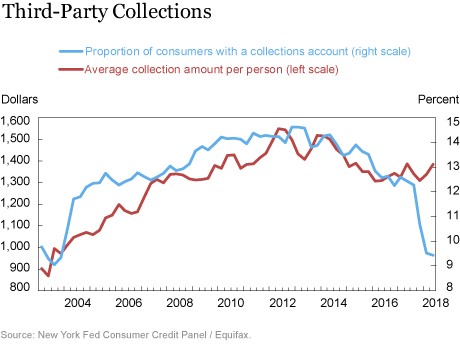

As a result of these efforts, the number of individuals with collections accounts (as identified by Equifax), dropped dramatically in the fourth quarter of 2017.

The New York Federal Reserve Bank Quarterly Report on Household Debt & Credit, outlined that 8 million people had collections accounts removed from their credit reports.

Consumers with the lowest credit scores benefitted the most from the NCAP initiatives with 18 percent of affected consumers experiencing a rise of 30 points or greater. Those who experienced a 40 or more boost in their scores began with an average of 529.

So, what actions can you take to monitor, maintain or boost your credit score?

Check your credit reports once a year.

It’s not that difficult. Place an activity on your calendar in January of every new year. The only source for free credit reports is http://www.annualcreditreport.com. The site is authorized by Federal law to provide a free copy of your reports every 12 months from each of the three credit reporting companies. Based on improvements by the NCAP, it’s easier than ever to report discrepancies (in most cases, online), and follow up to make sure errors have been removed.

Check your credit score annually.

Your credit history, activity, open and closed accounts are listed on credit reports which feed into the scoring algorithms used to create your three-digit numerical credit score. Consider scores and reports as joined pieces of a financial puzzle which form a story about your overall relationship and use of credit. Elements of a credit score include payment history, amounts owed, credit history, types of credit used and your application for new credit. The FICO® Score is an industry standard and the most popular.

A growing number of credit card vendors including major providers like Discover, Capital One, Chase and Bank of America now provide FICO® scores to customers. In addition, http://www.creditkarma.com will also allow free access to scores and reports. They will make product recommendations and are paid by a bank or lender if you obtain a product through one of their recommendations.

Payment history comprises a whopping 35% of your FICO® Score. Paying credit obligations on time is paramount.

If you’re retired don’t be afraid to utilize smart credit strategies.

I find new retirees suffer drops in their credit scores and refrain from using credit, which could be a mistake. The goal is to know when it’s smart to use credit compared to tapping precious liquid resources. This can be an incredibly advantageous endeavor through the early years of retirement where spending on discretionary categories like vacations, travel and major purchases pertaining to home improvement are at their zenith.

For example, a new retiree client recently decided to take advantage of Best Buy’s zero-percent interest credit card offer for quality home electronic upgrades. He takes comfort in knowing he has the cash to pay in full immediately but why do it when he can make minimum monthly payments and have cash earn interest in an online savings vehicle for two years?

Those who budget stay disciplined and motivated to boost cash flow through similar methods and utilize credit to work for them, not against them. In addition, smart credit management that includes timely payments, helps keep his respectable FICO® credit score (over 780), intact which can come in handy for future credit-based decisions.

Smart retirees are not in a hurry to close their credit card accounts. They’ll look to aggressively utilize the ones that provide the greatest benefits to their households; whether gathering points for travel, cash back or rewards for goods and services, credit card companies want your business and new retirees are active enough to take advantage of special offers.

Flex your credit muscle but don’t overdo it.

Credit scoring models reward usage and disciplined credit management. Don’t be afraid to flex your credit muscles by rotating the use of credit cards and utilizing credit overall as long as you don’t push the limits on every card you own. It’s important for credit agencies to observe responsible ongoing utilization of credit in conjunction with timely payments.

The world of credit scoring consistently evolves.

A credit score of 800 or above is considered excellent. A good or excellent score can save a consumer thousand in interest charges on automobiles and homes. The Loan Savings Calculator at http://www.myfico.com, calculates how the FICO® Score impacts the interest you’ll pay for the life of a mortgage or auto loan.