Authored by Richard Rosso via RealInvestmentAdvice.com,

An article, a reflection of his childhood, The Financial Times’ Berlin Correspondent Tobias Buck recently wrote of Germany’s immutable obsession with saving money. His behind-the-scenes account of piggy banks and children’s decorated money boxes (some, 400 years old), stored in a back shelf of the German Historical Museum stirred the memory dust for some guy in Texas. Me!

The recollection of a husky awkward second-grader at Morris H. Weiss School P.S. 215 in Gravesend, Brooklyn who couldn’t wait until (every) Thursday when a representative from Brooklyn Savings Bank came to collect coin and dollars for FDIC-insured coffers. His name I can’t recall; I do remember feeling the excitement of having my blue-pleather passbook savings book marked by another financial milestone. Stamped with the date and a new (higher) balance. It made me happy.

As a society, we made kids excited about saving money, once. Sure, we spent. When I was a kid I drove my mother crazy because I was only interested in popular name brands of food. I was a sucker for television advertising. For example, I would only eat the bacon with the Indian head profile complete with full headdress, on the front of the package – can’t recall the name now. Of course, it was the most expensive and as a single parent household, mom was on a tight budget.

I still remember catching her placing a less popular bacon in an old package of the brand I liked. Come to think of it, I think she did this often. I recall on occasion my Lucky Charms not having as many marshmallows. As I age I realize I’m fine with tricking children. Buy the Frosted Flakes, keep the box and replace with the generic brand to save money. Today, less expensive brands are tough to tell apart from the premium ones, anyway. Try it.

But I digress…

Throughout the financial crisis, nations threw fiscal stones at Germany for guarding their budget surpluses like Indiana Jones cradling the Holy Grail. The world demanded Germany spend, spend, spend – get all Keynesian, purchase imports from beleaguered brethren, get their citizens to purchase junk they don’t need. C’mon Germany, we’ll be your best friend if you give Greece a free pass.

Before the Great Recession the sovereign was a magnificent fiscal vacuum. Still is. A juggernaut of an export-oriented economy sucking in the bucks from European nations. Even today, Germany can’t catch a break for their ingrained (it’s in the blood), austerity. Donald Trump, the European Commission, IMF Chief Christine Lagarde beat up on Merkel for her nation’s trade surplus. Recently, Lagarde urged Berlin to increase domestic spending and boost imports, lamenting over the burgeoning account surpluses she claims are partly responsible for the rise of protectionism. Yep. Believe that? Most of the world abhors savers and adores spenders.

On the government and household level, Germany maintains a pristine track record of achieving and maintaining budget surpluses. It’s an obsession to be a saver on the Rhine. No debt on the Danube. Saving money, avoiding debt doesn’t merely affect German pockets, it touches their souls. It exists at the center of who they are. Germans are proud savers.

Per Tobias Buck’s article, the German Historical Museum is hosting a new exhibition called Saving – History of a German Virtue. I mean, how serious can you get? Saving =Virtue. Stock markets are frowned upon, perceived as gambling (they are – sorry, but they are). German savings banks are legally mandated to promote savings especially among children in conjunction with support of local school authorities. Banks provide play money and expose kids early to personal finance basics.

It motivates me to ask: What happened to us in America? When did consumption, especially of things we don’t need, gain sustained importance over saving for tomorrow? Instant gratification is a deep, dangerous affliction. Call it a disease.

In Germany, they’re all about delayed gratification; we’re all about the right now. Is there a middle ground we can agree upon? Where are the passbook savings accounts and the weekly elementary school visits to collect deposits? I remember how the girls back then safety-pinned their filled brown bank-deposit envelopes to their outer garments and dresses. Imagine? I’m dating myself. I get it. Hey, we perceive through personal prisms; who we are, is through experience. What kind of experience about saving are we providing for our children when it comes to saving?

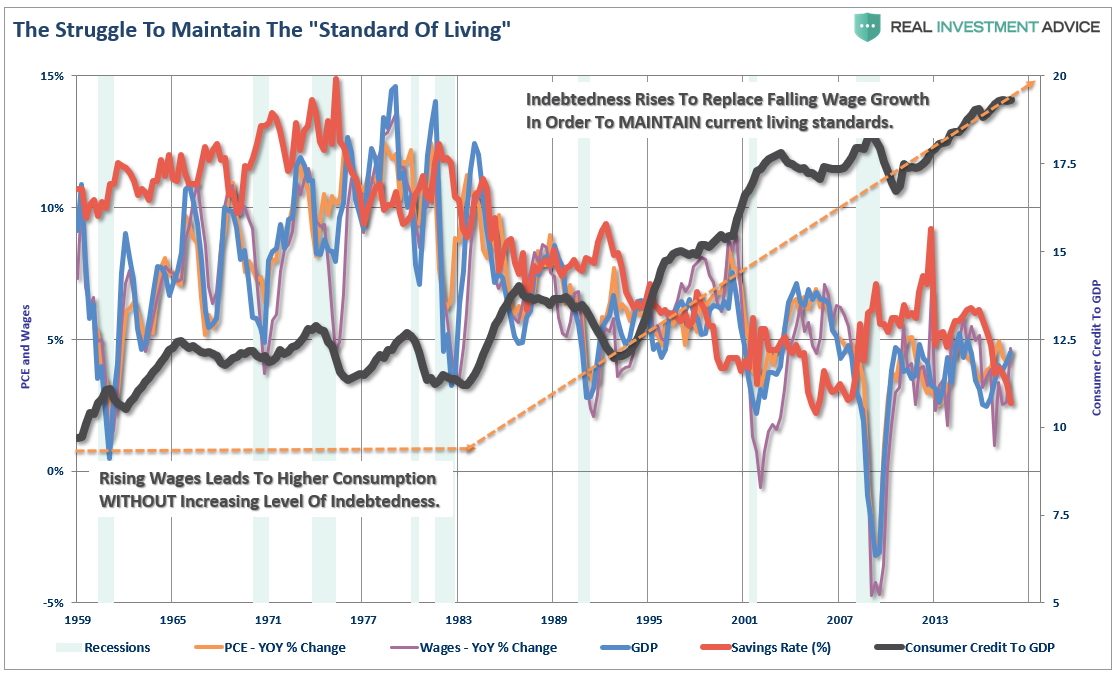

As wage growth deteriorated, seemingly our ability to adjust to the adverse structural condition did, too. After all, those ethereal wage increases were “right around the corner,” until we ran out of corners but decided we were still entitled to maintain a standard of living through credit. Tough decisions needed to be made, especially by Baby Boomers in the early 80s. If they were made, they weren’t passed down effectively.

My belief is Germans from the top down, from government desk to kitchen table, would have acted with alacrity and made uncomfortable decisions to adjust the slightest of imbalance. Perhaps downsizing, or a fiscal priority on increasing the skills of the labor force. Anything but cutting the saving rate. German households save 10% of their disposable income, twice as much the average across the globe, writes Mr. Buck. Amazingly, their saving rate has been stable and unaffected by economic crises and changes in interest rates.

In contrast, in the U.S.

On a somewhat positive note, the U.S. personal saving rate has ticked up to 3.4% as of February. Makes you all warm and fuzzy, doesn’t it?

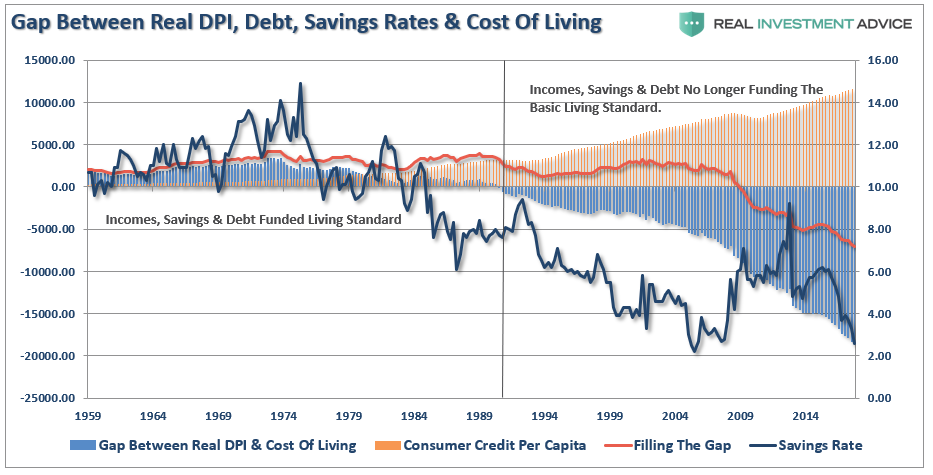

We are at a crisis level in America. Real (inflation-adjusted) incomes, the personal saving rate and debt are no longer funding basic living standards. It’s time for us to “German up” a bit and take control, make tough decisions within our own households to ‘mind the gap.’

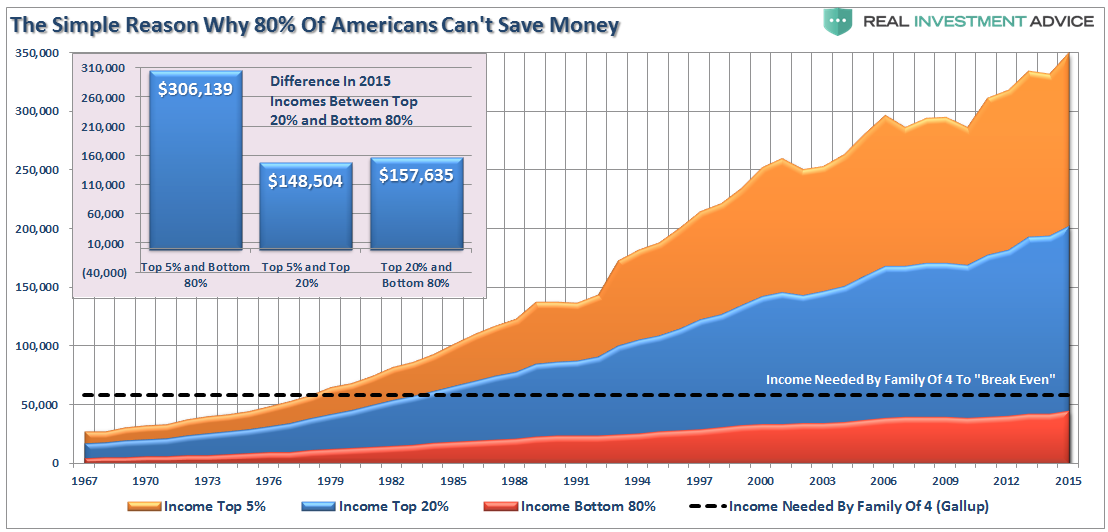

There are pervasive macro-economic charts created by the Fed, posted on their regional websites and plastered all over social media which display how Americans carry less debt than they did a decade ago; how wages are beginning to bust out of a long-term malaise. I’m happy about that. The micro story differs, however as income growth for the bottom 80% of Americans has been left in the dust. The top 20% however, are thriving. Unfortunately, it’s the masses who still need to make massive adjustments to bolster savings.

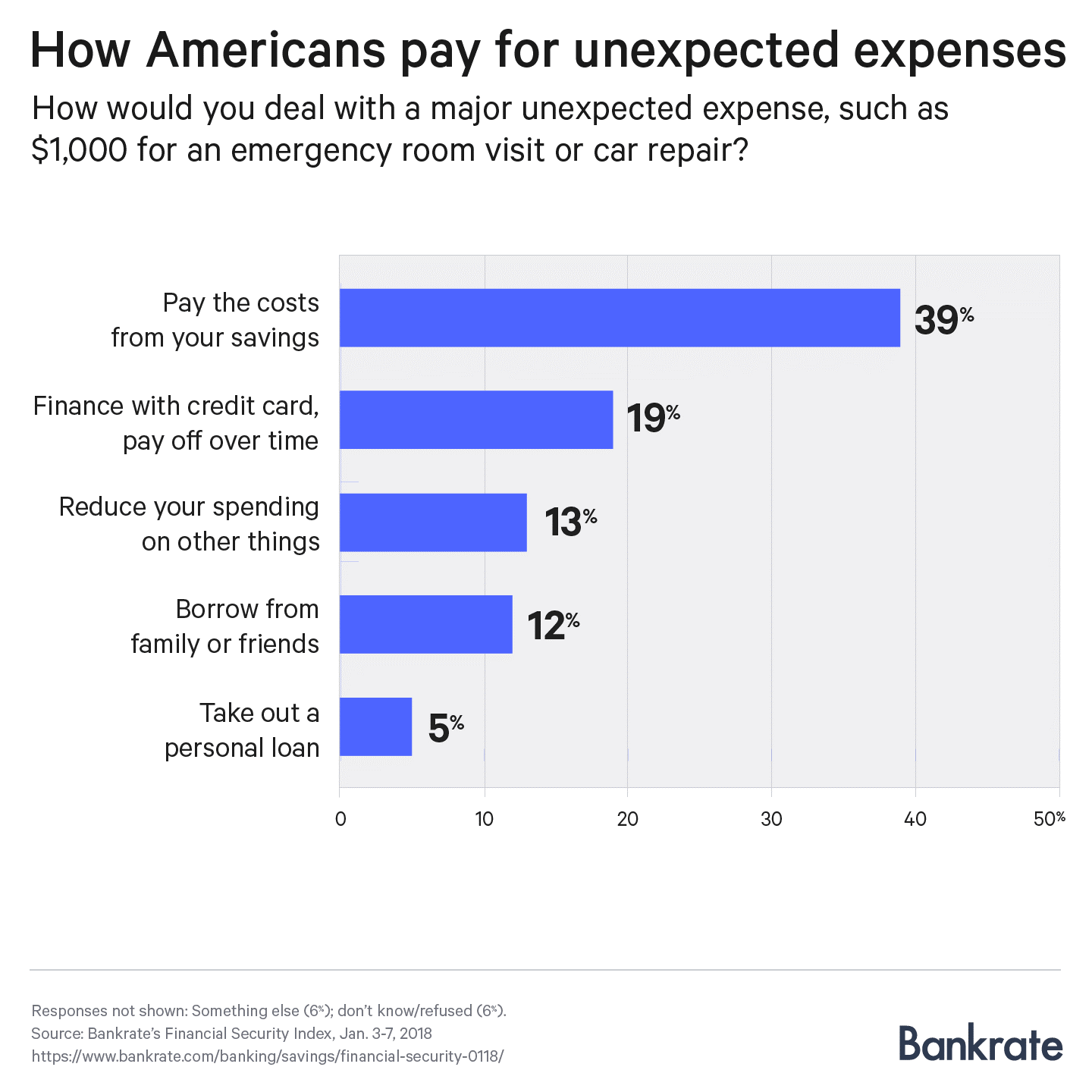

Per Bankrate’s latest financial security index survey, a majority of Americans can’t raise $1,000 for unexpected expenses (is my German friend Alda, reading? I may need to hit him up for a loan).

From the study:

“A sizable chunk of consumers seemingly haven’t seriously considered what they’d do in case of a crisis. One in 8 would count on reducing spending from other parts of their budget, 6 percent would resort to something else and 4 percent simply don’t know.”

It’s a disparate tale I write – one of virtue overseas, another of domestic heartache.

So, what can we do to become savers?

Begin with the following 5 questions. Write them by hand. Answer them in pen. Go back to them. Be thoughtful and truthful with responses:

- What is the motivation for spending on wants vs. needs? Needs are rent, lights, food. You get it. It’s about survival.

- How can you go from Needs Squared to Needs Basic? Needs on credit vs. needs paid from household net income. Tough, life-changing decisions required, perhaps. What would the Germans do?

- What statement can you create and repeat that will eventually link saving to virtue?

- Think Gross Personal Product. Most metrics of economic health are based on consumption; personal consumption comprises 70% of America’s Gross Domestic Product. Through the 60s and 70s, the U.S. personal saving rate rarely fell below 10%. Our ensemble culture or the culture overall has become obsessed with owning more, status through the acquisition of goods and services. In your household, it must be different. The movement must be grassroots, the individual one by one, taking action to shore up their personal and family household balance sheets. Think GPP, not GDP. Nobody is going to bail you out when the economy cycles in reverse. As a matter of fact, when our economy falls into the abyss, it’s we the taxpayers who bear the brunt of the costly, ineffective patchwork that fiscally duct-tapes systems back together.

- How can you get the family involved in the creation of “financial virtue-isms?” For example, what mutually agreed upon boundaries can be initiated around spending? How as a family unit, can saving become a virtuous activity? As a parent, I made a big deal of my daughter’s ability to save, even when it came down to three coins in her piggy bank.

- Saving is ethos for an honorable life.

- Saving isn’t a chore, it’s part of who you are. Deep. In the soul kind of deep.

- A living standard stretched by credit will eventually catch up, set you back.

- Living on household cash flow alone is an honorable goal.

- Wealth on credit is “Instagram Currency” – Social media appearance fodder, ‘living large,’ for image. “Likes” aren’t gonna pay the bills.

- No increase in spending without the wages or bonuses to back it up.

- The errant spending behavior of your parents does not define you.

So, I shared my personal philosophies around saving and spending to get you started.

“Austerity is an integral part of the image that Germans have of themselves – And a characteristic they feel sets them apart from other nations. There’s a deeply ingrained conviction that saving money and avoiding debt is not just a prudent approach to managing your income, but of something deeper.”

– Tobias Buck. The Financial Times.

Americans were savers once.

It’s not too late for our government, corporations and households to embrace similar lessons.

Richard Rosso, MS, CFP, CIMA

Richard Rosso is the Head of Financial Planning for Clarity Financial. He is also a contributing editor to the “Real Investment Advice” website and published author of “Random Thoughts Of A Money Muse.” Follow Richard on Twitter.