Wolf Richter wolfstreet.com, www.amazon.com/author/wolfrichter

China, Japan, other foreign investors, the Fed, US government funds? Nope.

Foreign private-sector investors and “foreign official” investors – central banks, governments, etc. – whittled down their holdings of US Treasury Securities by $21 billion at the end of July, compared to a year ago, to $6.25 trillion, according to the Treasury Department’s TIC data released Tuesday afternoon.

Over the same period, the US gross national debt – fueled by a stupendous spending binge and big-fat tax cuts – soared, despite a booming economy, by a brain-wilting $1.468 trillion, in just 12 months.

So, with foreigners having shed $21 billion over the 12-month period, who bought this $1.468 trillion in new US Treasury debt?

Here’s who didn’t buy:

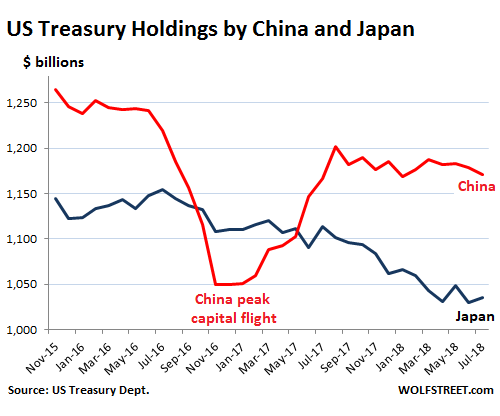

China’s holdings of marketable Treasury securities have remained roughly stable despite the arm-wresting match over trade, with its holdings at the end of July, at $1.17 trillion, up $4.7 billion from a year earlier.

Japan’s holdings fell by $78 billion year-over-year to $1.035 trillion, continuing the trend since the peak at the end of 2014 ($1.24 trillion):

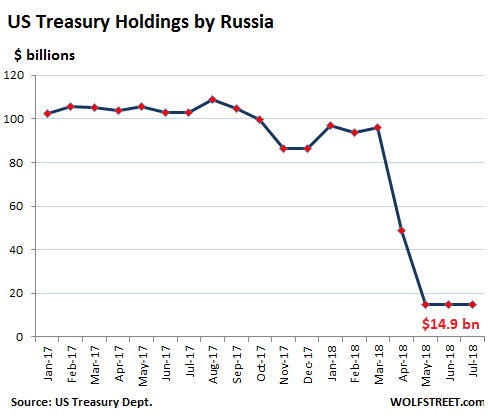

Russia, always a smallish holder of Treasuries compared to China and Japan, has liquidated 90% of its holdings, bringing them from $153 billion in May 2013 to just $14.9 billion in July:

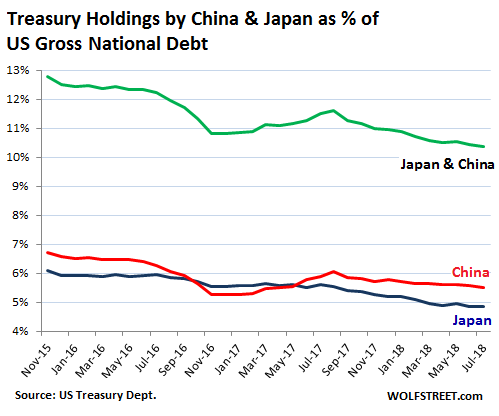

China and Japan have long played an outsized role as creditor to the US government. But their importance has been declining for years due to the growing pile of the US debt, and the simultaneous decline of their holdings. This caused their combined holdings (green line) to drop from nearly 13% of total US government debt at the end of 2015 to 10.4% in July, with Japan’s holdings (blue line) accounting for 4.9%, and China’s (red line) for 5.5%:

The Runners-up

Of the 12 largest holders of US Treasuries, after China and Japan, seven are tax havens for foreign corporate and/or individual entities (bold). The value in parenthesis denotes the holdings in July 2017:

- Ireland: $300 billion ($312 billion)

- Brazil: $300 billion ($271 billion)

- UK (“City of London”): $271 billion ($230 billion)

- Switzerland: $233 billion ($244 billion)

- Luxembourg: $222 billion ($213 billion)

- Cayman Islands: $196 billion ($240 billion)

- Hong Kong: $194 billion ($197 billion)

- Saudi Arabia: $167 billion ($142 billion)

- Taiwan: $164 billion ($184 billion)

- Belgium: $155 billion ($99 billion)

- India: $143 billion ($136 billion)

- Singapore: $128 billion ($112 billion)

The Americans are the only ones left.

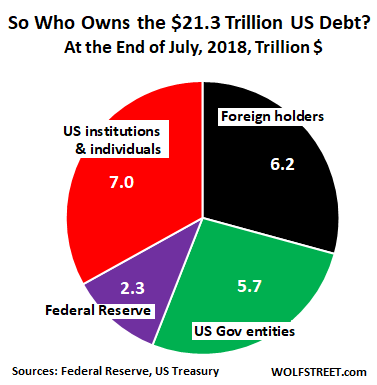

By the end of July, the US gross national debt had reached $21.31 trillion, up $1.47 trillion from July last year – as I said above, a truly brain-wilting increase for a booming economy. Here’s who bought or shed this paper over those 12 months:

- Foreign official and private-sector holders shed $21 billion, reducing their stake to $6.23 trillion, or to 29.2% of the total US national debt.

- The US government (pension funds, Social Security, etc.) shed $44 billion, reducing “debt held internally” to $5.70 trillion, or to 26.7% of the total.

- The Federal Reserve shed $128 billion through the end of July as part of its QE Unwind, reducing its pile to $2.337 trillion by the end of July, or to 11.0% of total US national debt.

- So if everyone shed, who bought? American institutional and individual investors, directly and indirectly, through bond funds, corporate or state pension funds, and other ways, owned $7.05 trillion, or 33.1% of the total US debt at the end of July, having added $1.66 trillion to their holdings over those 12 months!

And here’s how that rapidly growing elephantine US debt is now divvied up:

American private-sector investors are buying with a new-found passion. Yields have risen quite a bit, though they remain below the rate of inflation for everything up to three-year maturities: The one-month yield closed today at 2.05%, the one-year yield at 2.58%, the two-year yield at 2.81%, and the 10-year yield squiggled over the 3% line again, to close at 3.05%.

The fact that the 10-year yield is still so low, compared with short-term yields, shows that there is huge demand for long-term maturities. If there were less demand, the yield would have to rise to lure new investors into buying (prices fall when yields rise). And anytime the yield rises just a little bit on the 10-year, these new buyers emerge in force and that demand pushes the price up and pushes the yield back down. And this demand for US Treasuries is not coming from foreign entities, the Fed, or US government funds, but from American investors.