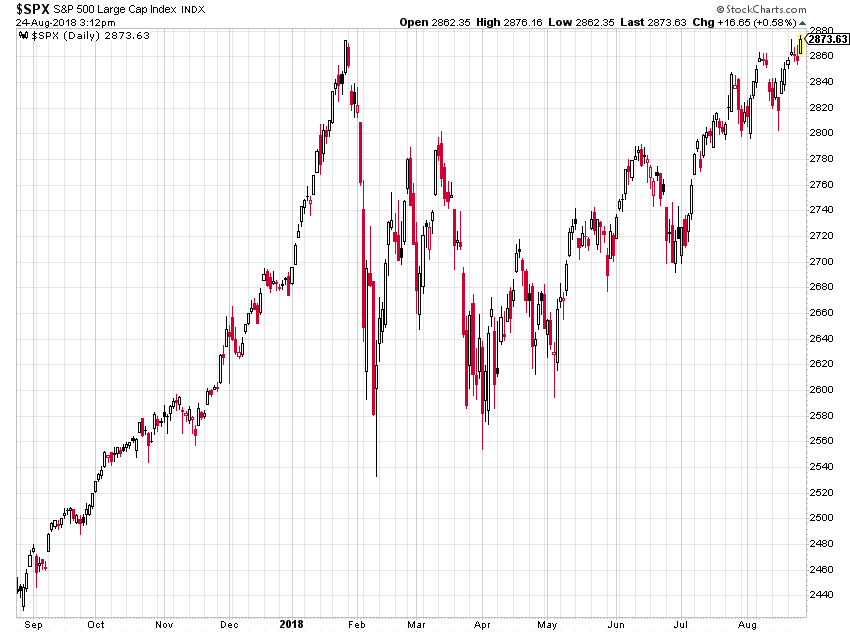

The S&P 500 hit an intraday record of 2,876.16 today, surpassing its January 2018 peak that occurred before the violent 12% correction that ensued in February. The official reason for today’s bullish action is Fed Chairman Jerome Powell’s speech in which he outlined his expectations for gradual interest rate increases. Powell’s speech didn’t contain any new information, and that’s exactly why the market rallied – relief.

As discussed in Part 1 of this series, record low interest rates are the primary reason for both the overall U.S. household wealth bubble as well as the U.S. stock market bubble. The chart below shows how U.S. interest rates (the Fed Funds Rate, 10-Year Treasury yields, and Aaa corporate bond yields) have been at record low levels for a record period of time since the 2008 financial crisis. The fact that credit has been so cheap for so long explains why the household wealth bubble is so extreme and why the stock market bubble is so inflated, as valuation indicators later on in this piece will show.

Low interest rates contribute to the inflation of asset and credit bubbles in numerous ways:

- Investors can borrow cheaply to speculate in assets (ex: cheap mortgages for property speculation and low margin costs for trading stocks)

- By discouraging the holding of cash in the bank versus speculating in riskier asset markets

- By encouraging higher rates of inflation, which helps to support assets like stocks and real estate

- By encouraging more borrowing by consumers, businesses, and governments

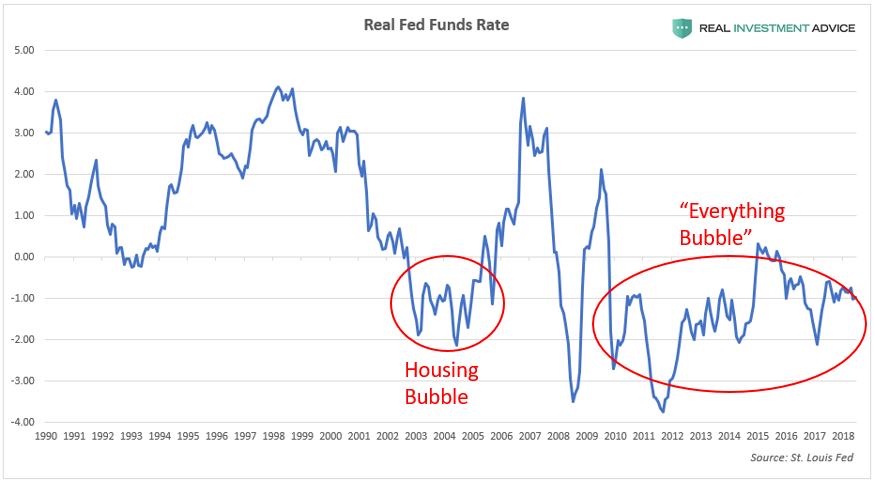

The chart of real (inflation-adjusted) interest rates below confirms just how loose U.S. monetary policy has been since the Great Recession. In recent decades, the only time the U.S. has experienced negative real interest rates for a significant amount of time was during the mid-2000s housing bubble and during the current “Everything Bubble” period that started after 2009. (Note: “Everything Bubble” is a term that I’ve coined to describe a dangerous bubble that has been inflating across the globe in a wide variety of countries, industries, and assets – please visit my website to learn more.)

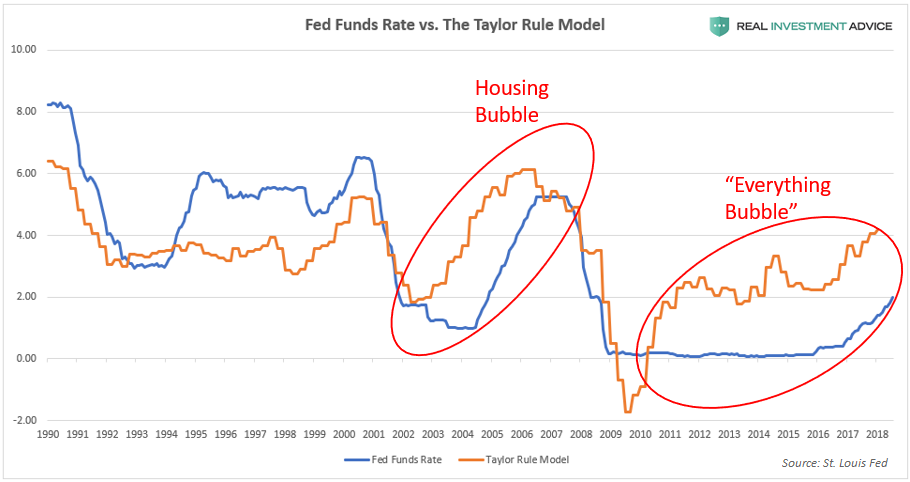

Another way of determining how excessively loose (or tight) U.S. monetary conditions are is by comparing the Fed Funds Rate to the Taylor Rule model. The Taylor Rule is a proposed guideline created by economist John Taylor to estimate the ideal level for central bank-controlled benchmark interest rates – such as the Fed Funds Rate – for the purpose of maximizing the stability of economic growth. When the Fed Funds Rate is much lower than the Taylor Rule model, it means that interest rates are likely too low relative to economic growth and inflation, which greatly increases the probability of forming a dangerous economic bubble. The chart below shows that the Fed Funds Rate was much lower than the Taylor Rule model during the formation of both the mid-2000s housing bubble as well as the current “Everything Bubble.”

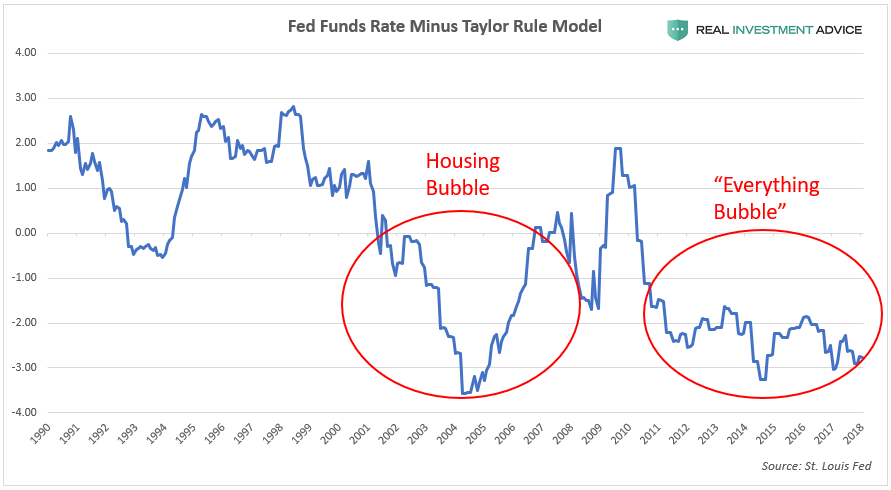

The chart below plots the difference between the Fed Funds Rate and the Taylor Rule model to show when U.S. monetary policy is likely too tight (when the chart is in positive territory) or too loose (when the chart is in negative territory). Both the U.S. housing bubble and the current “Everything Bubble” formed when the difference between the Fed Funds Rate and the Taylor Rule model was negative (the Fed Funds Rate was lower than the Taylor Rule model).

If you are like most investors, the U.S. household wealth bubble means that your own investments, wealth, and retirement fund are extremely inflated and exposed to grave risk of another crash. Most investment firms have absolutely no clue that another storm is coming, let alone how to navigate it. Clarity Financial LLC, my employer, is a registered investment advisor firm that specializes in preserving and growing investor wealth in precarious times like these.