via heisenbergreport:

BofA’s Mark Cabana – who repeatedly warned about a possibly imminent squeeze in short-term funding markets prior to the acute episode that grabbed headlines late last month and caught the Fed flat-footed – is worried that a “combustible cocktail” may create the conditions for another such episode at the end of the year.

The Fed has, of course, taken decisive steps to ameliorate the situation, grease the proverbial wheels and otherwise address reserve scarcity. Overnight and term repos (instituted in the wake of September’s chaos, upsized on demand and now set to run through January) and front-loaded organic balance sheet growth have brought things under control, but there’s reason to believe that no matter what the Fed does, year-end will be challenging.

Specifically, Cabana is worried about reserve shortage and dealer intermediation constraints related to GSIB. That’s the “combustible cocktail”.

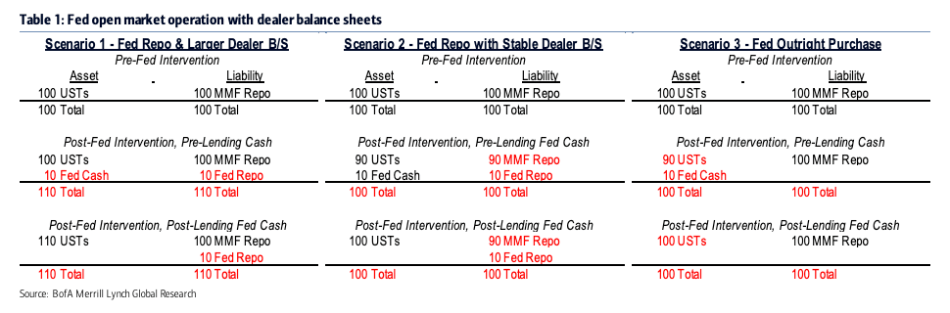

Those two concerns are inextricably bound up with one another. “The way that Fed repo and GSIB issues are linked is through the Fed’s short-term temporary repo operations”, Cabana writes, in a new note. While the TOMOs increase the size of dealer balance sheets, GSIB realities prompt dealers to cut market making activity. The following table is a (highly) stylized effort to illustrate the interplay.

(BofA)

As Cabana goes on to detail, scenarios 1 & 2 “demonstrate complications with the Fed repo operations and dealer balance sheet: either the dealer expands balance sheet to ease repo funding pressures but worsens their GSIB score or the dealer adjusts the mix of their liabilities to facilitate Fed repo but does not increase the amount of financing available”.

Naturally, dealers will prefer something akin to scenario 2 into the year-end GSIB date. “This risks MMF getting pushed away from the dealers and having few options to lend into the repo market outside of Fixed Income Clearing Corporation sponsored repo”, Cabana notes.

So, what to do? How will the Fed address a situation where, even if reserve shortage is addressed by increasing the amount of reserves in the system, dealers are reluctant to intermediate them?

Before offering some suggestions, Cabana notes that the “reserve hole” is now larger than $200 billion. Over time, temporary repos will need to be soaked up via outright purchases (i.e., the Fed’s just-launched monthly bill buying program). The chart on the right below shows how that should evolve. (Remember also that over time, the need for reserves will grow, hence the necessity of perpetual “organic” balance sheet growth.)

(BofA)

Note on the right that at the current rate of bill purchases, the Fed will confront year-end with a still-large reliance on repo. That, Cabana goes on to warn, “creates GSIB-related dealer intermediation issues especially if repos are concentrated at short tenors”. Here’s a great table that shows how this all interacts:

(BofA)

As for how to reduce the risk of another funding squeeze, BofA has several suggestions which Cabana details extensively over the course of five pages.

Focusing on the three most likely “solutions”, BofA suggests Treasury might do the Fed a solid by lowering its year-end cash balance projection. That would “eliminate any additional reserve drain from the TGA”, Cabana writes, adding that it’s feasible given that “Treasury previously indicated they desire to hold a level of cash sufficient to cover one week of outflows, which is historically around $300bn in December and we estimate could be covered by a cash balance around $360bn”. In August, the forecast was $410 billion.

If you’re wondering why Treasury would be keen on helping the Fed fix its own issues, the answer is that it isn’t just the Fed’s problem. To wit, from BofA:

The US Treasury has $16+ tn in marketable debt held by the public and over $1 tn of this debt is financed in the Treasury repo market on a daily basis. UST repo issues could impact the broader liquidity of the Treasury market and the US Treasury should have a vested interest in ensuring the market functions smoothly.

…

…