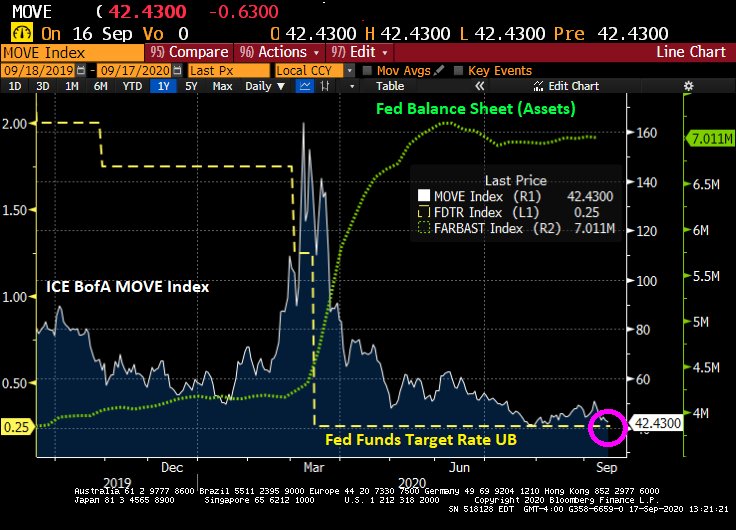

ICE BofA MOVE 1-, 3-month indexes spread highest since 2013

Trump election, positioning, postal voting elevate volatility

(Bloomberg) — Treasury options markets are pricing the Nov. 3 U.S. presidential election as one of the biggest isolated event risks in at least a decade.

The ICE BofA MOVE Index, which measures expected swings in Treasury yields across the curve, shows the spread between one- and three-month indexes rising to a level seen only once in the past decade. The latter captures the election between President Donald Trump and Democratic nominee, Joe Biden.

Investors’ nervousness about the potential for short-term turmoil can be seen in cross-asset volatility, particularly spreads for FX and Treasuries. Outside the U.S., the election is also starting to stress investors in the emerging world, and strategists and investors are urging caution as implied volatility rises.

The options markets on interest-rate swaps, commonly known as swaptions, also show traders are bracing for aggressive swings. A one-month option on the 10-year swap rates – which doesn’t start till a month’s time – has a terminal breakeven of 17 basis points. That implies a swing of down to 0.51% or up to 0.85%, from current level of 0.68%.

At least the MOVE index has been hammered-down by Fed monetary policy, including yesterday’s dot plot indicating QE Infinity!!!