by orangebubly

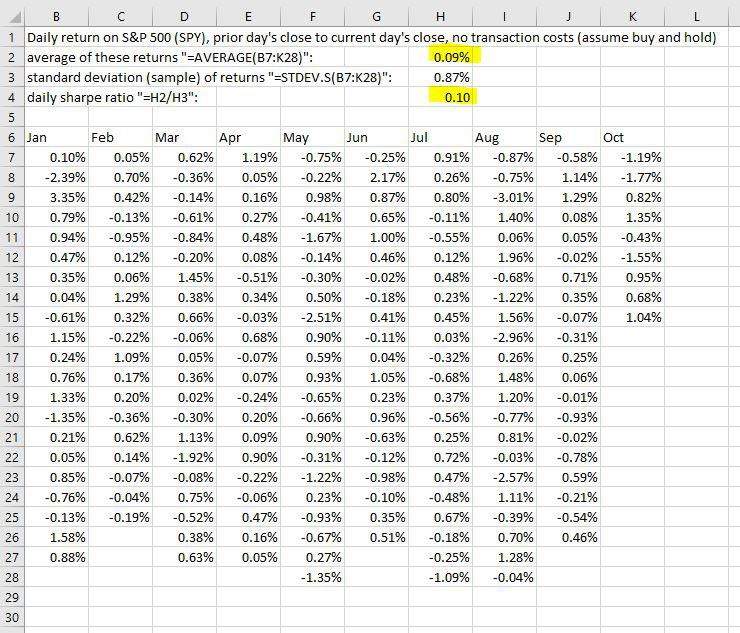

In a prior post, some people criticized the daily return and sharpe ratio of my algos, so I thought I’d show people how to do the calculation. Below is the daily return and sharpe ratio of simply buying and holding the s&p500 throughout 2019 (no transaction costs, assume you buy on the last day of the prior year and hold until now). In this amazing year, you would have earned 0.09% per day, with a daily sharpe ratio of 0.1. This should show you that a daily sharpe ratio of 0.1 or more is good.

If you’re curious, if you would have purchased and held a 3x leveraged s&p 500 fund for the year, your daily return would grow from 0.09% to about three times that, or 0.27%, but your daily sharpe ratio would not change. It would still be 0.1. The daily sharpe ratio is a decent rule of thumb way of checking if your trading strategy is working, and if it’s better than another strategy. [Edit: To add some nuance, this year a 3x leveraged s&p fund, e.g. SPXL, would have earned 0.24% per day due to something called volatility decay, and In no way am I advising you to invest in a 3x leveraged s&p fund. Sure, it would have earned you 60% this year, but it would have wiped you out in 2007-2008. I only mentioned it here to note how, although its average daily return is about 3x the s&p, its sharpe ratio is the same, and so this is an example of how higher returns don’t necessarily mean a better strategy. I intended to criticize spxls, not recommend it.]

If you’re curious, buying and holding the s&p since 1993 would give you a daily return of 0.04% with a daily sharpe ratio of 0.04. That’s why I say if your daily sharpe ratio is 0.1 or higher, you’re doing well. If your daily sharpe ratio is under 0.04, then you might be better off just buying and holding the s&p.

https://i.redd.it/u18hg5euybs31.jpg

Disclaimer: Consult your financial professional before making any investment decision.