Earnings up, multiples down. Such seems to be a straightforward rationale for why investors should pile into markets as it enters a “new phase.”

Such was the suggestion made recently by Yahoo! Finance anchor Myles Udland.

“The stock market is entering a new phase. Investors right now are faced with a simple question: how much? How much do they want to pay for earnings growth that continues to blow away expectations but might also be peaking?”

It’s a good question.

With wealth investors expecting to earn 17% average annual returns, there currently does seem to be little concern about valuations.

“According to a new survey from Natixis that surveyed households that have over $100,000 in investable assets in March and April of 2021. Those same investors report they expect to earn 17.3% above inflation in 2021, which, while high, may be understandable.“

However, to assess “how much,” we need to understand what it means when the media makes comments about “forward earnings” and “future multiples.”

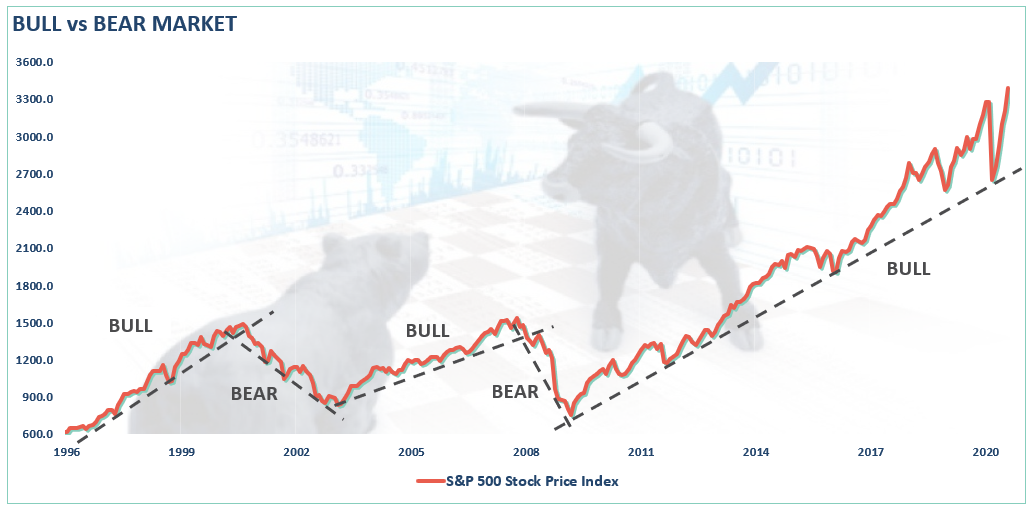

Not A New Cycle

We need to start by dispelling the myth that begins the article. The market is “not” entering a “new phase.” Yet, in a rush to pitch the bullish case for stocks, the media has continued to suggest the March 2020 decline was a “bear market cycle.” Such would support the idea a new “bull market cycle” has started.

However, as discussed in “Confusing Bear Markets & Crashes,” March was a “correction” within a “bull market cycle.” To wit:

“As Sentiment Trader notes, the 20% rule is arbitrary. The question is, after a decade-long bull market, which stretched prices to extremes above long-term trends, is the measure still valid? “

If a 20% decline is arbitrary, what measures accurately define a “bull” or “bear” market? To answer that question, let’s clarify the premise.

- A bull market is when the price of the market is trending higher over a long-term period.

- A bear market is when the previous advance breaks, and prices begin to trend lower.

The chart below provides a visual of the distinction. When you look at price “trends,” the difference becomes both apparent and valuable.

This distinction is vital for investors, particularly when discussing the starts of “new market cycles.”

- “Corrections” generally occur over short time frames, do not break the prevailing trend in prices, and are quickly resolved by markets reversing to new highs.

- “Bear Markets” tend to be long-term affairs where prices grind sideways or lower over several months as valuations are reverted.

The decline in March did not meet any of the criteria necessary to be classified as a “bear market.”

- The decline was unusually swift and did not break the prevailing bullish price trend.

- The recovery to new highs occurred quickly; and,

- Valuations did not revert from previously elevated levels.

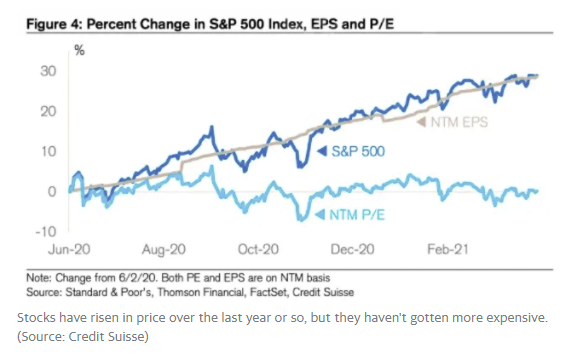

Stocks Are Eating Earnings

As noted, the correction in March did not revert the overvaluation in the markets that existed in February of 2020. While earnings declined, the price advance was so fast it kept valuations elevated throughout the “economic shutdown.” Thus, while valuations did not get more expensive, they did not get cheaper either.

“The chart, which came from Credit Suisse equity strategist Jonathan Golub, showed that while stock prices had been in rally mode for months, the market wasn’t getting more expensive.” – Myles Udland

In other words, the rise in prices “ate the recovery” in earnings. If this had been a “real bear market,” investors would have shunned stocks keeping prices depressed as earnings recovered, thereby lowering valuations.

That is also another characteristic of “bull market correction” and a “real bear market.” Following a “bear market,” investors do not rush back into the riskiest of assets.

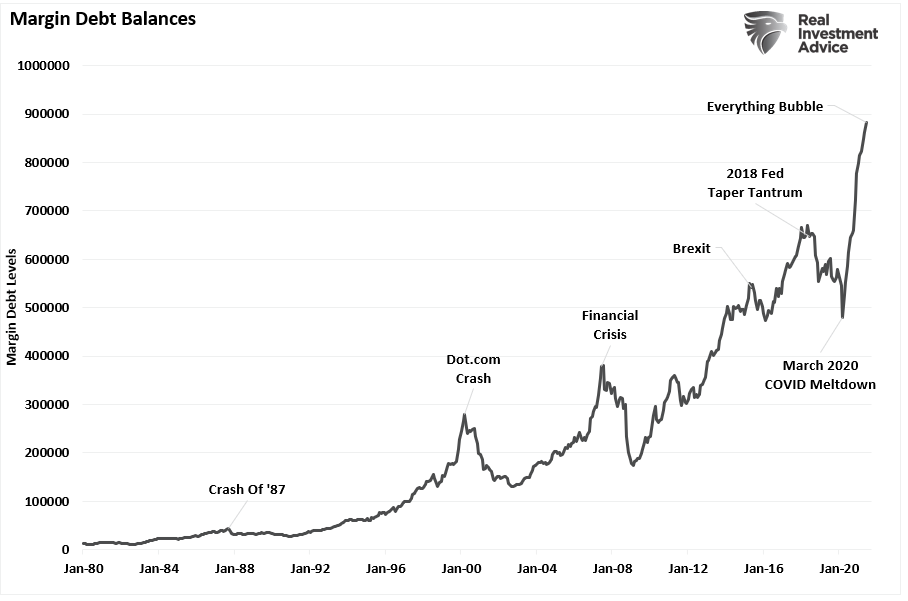

Most importantly, you don’t see investors piling into leverage at the beginning of a new “bull market cycle.”

The Problem With Lower Forward Valuations

However, here is the “ugly truth” of “forward valuations.” Let’s start with Myles’s analysis as a baseline.

“Right now, the S&P 500 currently trades at roughly 22x forward earnings. You might hear this referred to as the market’s multiple or its valuation. The terms are roughly interchangeable. And we say roughly because there are always exceptions.

So a simple way of thinking about the earnings multiple for the market is how much you need to pay as an investor for $1 of earnings power.” – Myles Udland

The S&P 500 recently traded at 4,353. According to the latest data from S&P, earnings estimates for the index at the end of 2022 are $189. Divide the index level by the expected annual earnings for the index, and you get the earnings multiple. In this case, 4,353 divided by 189 is 23.03. So, for every $22.03 you put into the S&P 500, you can expect to get back $1 in earnings based on today’s estimates.

Read that again.

23-Years To Get Your Money Back

While investors take this to mean the market will be cheaper in the future, therefore using that rationalization to “buy stocks,” such is not the case.

The correct way to interpret valuations of 23x earnings is to realize two things.

For earnings in the future to catch up with the market’s current price, price returns over the next 18-months must be ZERO.

If stocks continue to appreciate during the period, valuations can decline if earnings growth is faster than the price of appreciation. However, such does not necessarily resolve the overvaluation of the market.

Secondly, and to Myles’s last point, while it may seem like a “bargain” to pay $23 for each $1 of earnings, that is not precisely what that means. Here is the math:

“If you pay $23 for $1 in earnings, and the company distributes that $1 of earnings to you each year, it will only take you 23-years to get your money back.“

All of a sudden, that doesn’t sound like such a good deal.

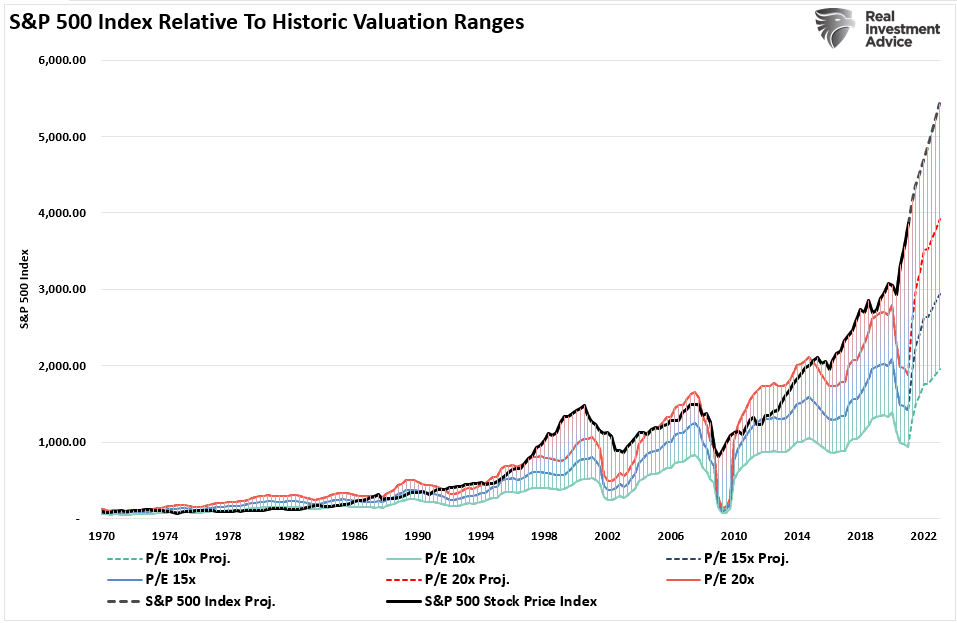

Valuations Are Astronomical

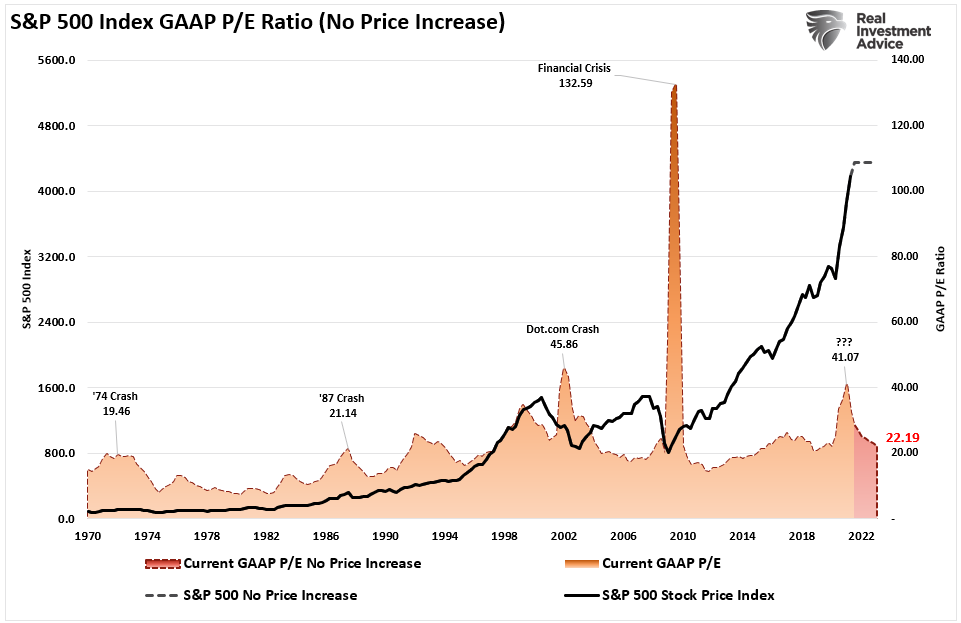

In 2013, valuations on stocks were around 19x trailing earnings. While certainly expensive, valuations had not yet eclipsed previous “bull market” excess of 23x earnings. As shown below, even if we assume no increase in the index price, the market will remain well above 20x earnings over the next two years assuming analyst estimates are correct.

I recently quoted Carl Swenlin on earnings. As Carl noted, there is nothing normal with GAAP earnings. But, of course, today, most companies report “operating” earnings which obfuscate profitability by excluding all the “bad stuff.”

The following table shows the expectations for reported earnings growth:

- 2020 (actual) = $94.13 / share

- 2021 (estimate) = $161.62 (Increase of 71.69% over 2020)

- 2022 (estimate) = $189.48 (Increase of 101.29% over 2020)

The chart below uses these earnings estimates and assumes NO price increase for the S&P 500 through 2022. Such would reduce valuations from 41x earnings currently to roughly 22x earnings in 2022. (That valuation level remains near previous bull market peak valuations.)

However, as stated above, investors always bid up prices as earnings increase. With earnings expected to double over the next two years, if we reduce wealthy investor return assumptions to just 15% annually, the picture changes. Instead of valuations declining, the increase in price keeps valuations hovering near 27x earnings.

Potentially Disappointing Outcomes

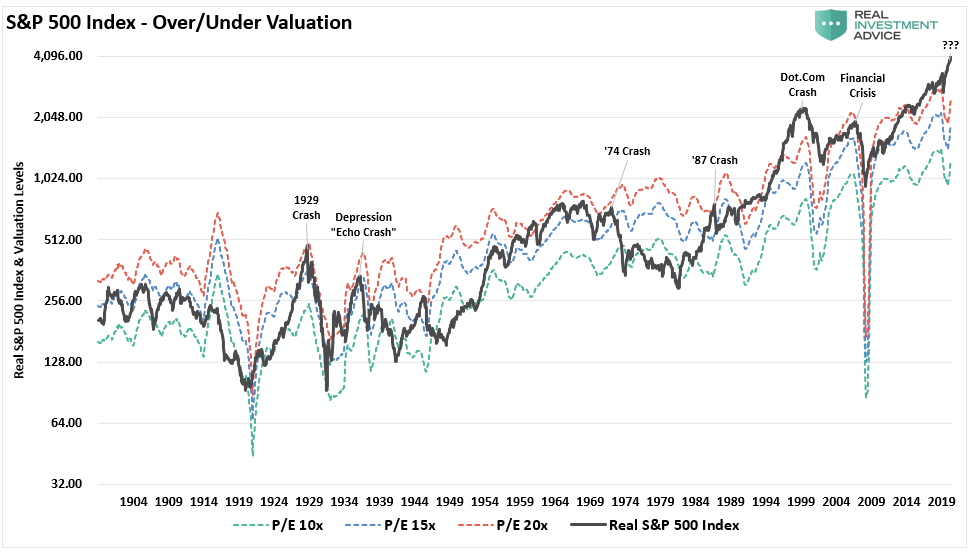

Given that markets are already trading well above historical valuation ranges, such suggests that outcomes will likely not be as “bullish” as many currently expect.

“Historically, price has usually remained below the top of the normal value range (red line); however, since about 1998, it has not been uncommon for price to exceed normal overvalue levels, sometimes by a lot. The market has been mostly overvalued since 1992, and it has not been undervalued since 1984. We could say that this is the ‘new normal,’ except that it isn’t normal by GAAP (Generally Accepted Accounting Principles) standards.” – Carl Swenlin

The hope, as always, is that earnings will rise to justify the over-valuation of the market. However, when earnings are rising, so are the markets.

Most importantly, analysts have a long and sordid history of being overly bullish on expectations of growth which fall well short. Such is particularly the case today. Much of the economic and earnings growth was not organic. Instead, it was from the flood of stimulus into the economy, which is now evaporating.

Conclusion

While Myles’ analysis is typical for mainstream media, it is essential always to consider the context in which it gets structured.

Throughout history, overvaluations of markets have never been resolved by earnings catching up with the price. Secondly, the two-fold problem of the temporary nature of the stimulus and inflation leaves the market vulnerable to a downshift in earnings expectations over the next couple of quarters. As noted, Wall Street has ratcheted up expectations to try and justify current prices.

However, a bit of analysis suggests that over-estimating earnings will lead to a price correction when it becomes realized. While that is something we do not expect immediately, we think markets will likely wake up to this reality in the last half of the year.

While monetary interventions allow market participants to ignore the reality of the economic ties to the market, such does not preclude hair-raising volatility and significant declines, as we saw in March 2020.

In 2021 and 2022, earnings are likely to come in once again lower than analyst’s exuberant estimates. But such shouldn’t be a surprise since they are never accurate historically. More importantly, if the Fed backs off, whether by its design or due to inflation, slower economic growth, or massive debt overhead, rich valuations will matter.

The risk of disappointment is high. And so are the costs of investing based on analysis without all of the facts.