Don’t worry about faster inflation. The Federal Reserve has a history over the past two decades of snuffing out consumer-price increases before they take hold. Instead, worry that even modest inflation could compel the Fed to undertake a late-cycle acceleration in the pace of tightening.

Inflation is rebounding in line with the Fed’s expectations, as weak numbers from last March drop out of the year-over-year comparisons. The weakness of last year was indeed transitory, and, on the back of a low unemployment rate, central bankers expect inflation to firm up a bit more and modestly overshoot the Fed’s 2 percent target by the end of 2019. Policy makers expect inflation to peak near 2.1 percent this cycle, according to the latest projections.

Even as inflation picks up, any fears of high inflation seem unwarranted. Former Fed Chairman Alan Greenspan, for example, has made the case that the economy is set for a case of stagflation unlike any since the 1970s. Indeed, it is fairly easy to draw such parallels. The Fed anticipates that unemployment will fall to 3.6 percent, a level it hasn’t reached since the late 1960s. Add on fiscal stimulus when the economy already operates near or beyond full employment, and the parallels grow even more eerie.

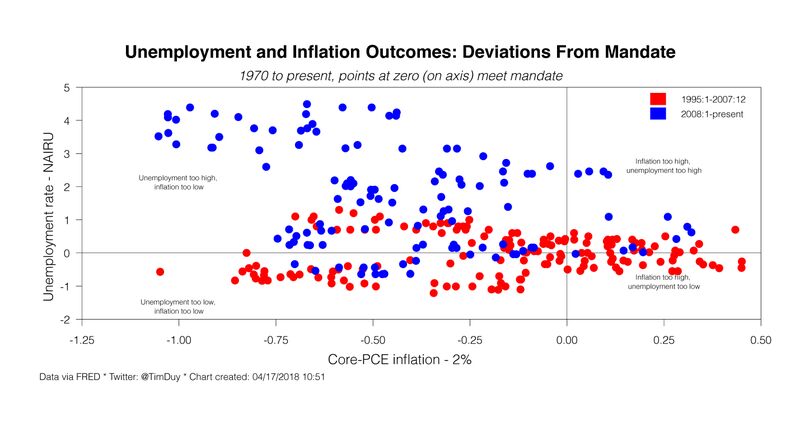

This Fed, however, is likely to act well before inflation rises enough to destabilize expectations. This is the takeaway of the central bank’s policy actions since the low and stable era of inflation began in the mid-1990s. The Fed hasn’t faced a period of high consumer-price inflation since then. Instead, the Fed’s main challenge has been fighting high unemployment.

This indicates that worrying about high inflation is unwarranted. The Fed has proved time and time again that it will act long before such concerns become relevant. New York Federal Reserve President William Dudley, who will soon step down, made this clear this week:

As long as inflation is relatively low, the Fed is going to be gradual. Now, if inflation were to go above 2 percent by an appreciable margin, then I think the gradual path might have to be altered.

The Fed is prepared to accelerate the pace of hikes if inflation makes an appearance. Still, what’s an “appreciable margin”? It’s hard to know exactly as the Fed has a specific inflation target of 2 percent rather than a range around that target. But based on their past behavior, central bankers are likely to be comfortable with core inflation within a 25 basis-point range of their 2 percent target as long as their forecast anticipated a return to target within a medium-term time horizon.

Let’s say, however, that a 25 basis-point overshoot is too hawkish and assume central bankers would tolerate a more dovish 50 basis-point overshoot. That would mean the worst-case scenario is that the Fed allows inflation to drift up to 2.5 percent and expect it to remain there or higher before central bankers accelerate the pace of rate hikes. That’s not exactly high inflation. It is certainly nothing like the stagflation of the 1970s.

In short, if there is any hint of sustained inflation at this stage of the business cycle — with low unemployment threatening to go lower with fiscal stimulus — past behavior indicates the Fed will risk and accept a recession before it allows a truly high inflationary environment to develop. That means your medium-term risk is more recessionary than inflationary. The caveat, however, is that it assumes the Fed remains independent. That independence will be tested as soon as it tightens policy sufficiently to slow the economy, and the testing will rise in tandem with the risk of recession.