I am still laughing over Fed-nominee Stephen Moore calling Ohio “the armpit of America.” But I wonder what Moore has to say about the idea of a new Fed quantitative easing scheme:

Federal Reserve officials are considering a new program that would allow banks to exchange Treasurys for reserves, a move aimed at ensuring liquidity during difficult times that also would help the central bank decrease the size of its nearly $4 trillion balance sheet.

The so-called standing repo facility is in its early discussion phases. Respected St. Louis Fed economists David Andolfatto and Jane Ihrig have authored two papers on the plan, which they say would ease the regulatory burden for banks that feel pressured into holding ultra-safe assets.

And on the repo front!

(Bloomberg) — U.S. short-term interest rates are on the rise again as a result of month-end funding dynamics.

Borrowing costs in one of the key U.S. funding markets soared on the final trading day of April, with the rate on overnight general collateral repurchase agreements climbing to levels unseen since the end of the first quarter. The rate reached around 2.88 percent in early New York trading hours, up from roughly 2.57 percent on Monday, ICAP data show.

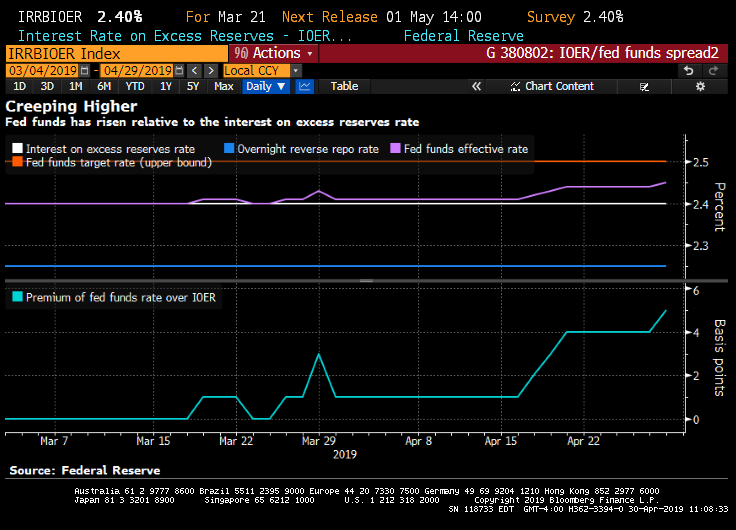

The benchmark targeted by the Federal Reserve in its implementation of monetary policy is also continuing to tick higher, with the effective fed funds rate rising to 2.45 percent on Monday, according to central bank data released Tuesday.

Repo rates typically move higher at the end of the month as some dealers curtail activity in the financing markets to shore up their balance sheets. Adding to the upward pressure is a potential influx of additional collateral, with settlements on Tuesday for around $235 billion in new Treasury bills and coupon-bearing securities. On top of that, recent outflows from government money-market funds means there’s been less cash to lend in the repo market, which could also be contributing to elevated rates.

The move in repo may be helping to drive up the effective rate for the central bank’s benchmark because it can draw some lenders away from fed funds and into the more attractive rates offered by the secured market. The effective fed funds rate has already moved well above the central bank’s interest on excess reserves rate — a level that’s historically acted as a cap for the benchmark and currently stands at 2.40 percent — prompting questions about a possible response from policy makers. While it’s still within the Fed’s overall target range for fed funds of 2.25 percent to 2.50 percent, it is creeping higher within that band.

The increase in the repurchase agreement rate is also likely to have a knock-on effect for the Secured Overnight Financing Rate, the repo-linked heir presumptive to the London interbank offered rate.

The Fed is also considering NEGATIVE Fed Funds rates (which have not helped Japan and Europe). This reeks of … Frank Booth in Blue Velvet.