Global economy peaked? | Michael Roberts Blog

Optimism for global economic growth remains. But the acceleration in 2017 from the low growth rates experienced in 2015-6 now seems to have paused in the first quarter of 2018. To greet the semi-annual meeting of the IMF and the World Bank in Washington to discuss latest economic developments, Maurice Obstfeld, the IMF’s chief economist, stated that “the world economy continues to show broad-based momentum.” But “against that positive backdrop, the prospect of a similarly broad-based conflict over trade presents a jarring picture.”

The IMF hiked its forecast for global real GDP growth to 3.9% for this year and in 2019. This improvement from the poor levels of 2015 and 2016 is based on rising investment and a recovery in world trade (which now seems to be threatened). The major economies of world capitalism are doing better but the idiocies of protectionism in trade by the likes of Donald Trump are threatening that recovery. That seems to be the main worry.

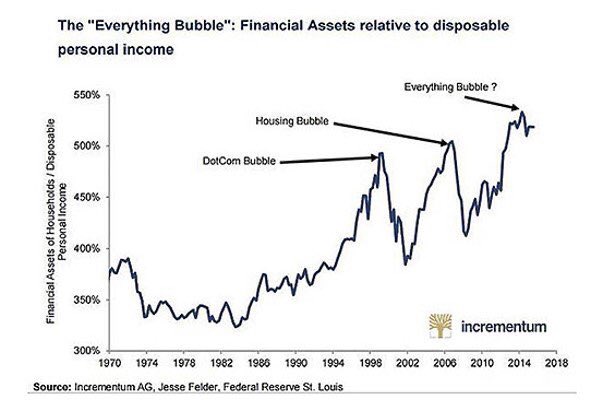

But Obstfeld is worried about the high levels of global debt, in households, corporations and governments. With interest rates set to rise, as the US Fed and possibly other major central banks start to raise their policy rates, the cost of servicing record-high debt will rise. That threatens further investment in productive (value-creating) assets and also instability in financial markets.

There has already been a ‘correction’ in world stock markets of about 13% since the beginning of the year as financial speculators begin to worry about an international trade war and rising costs of debt. And that is despite the huge handouts in tax cuts for US corporations introduced by Trump. Those tax cuts have sharply increased (temporarily) the profits of the largest US corporations, especially the banks. But that extra money (paid for by further cuts in US federal public services and a big increase in government borrowing) is not going mainly into extra productive investment. It is being used to buy back corporate shares to boost the share price of companies and into extra dividend payments to shareholders.

S&P 500 companies have already announced about $167bn of new buyback authorisations this year, and analysts at JPMorgan predict that trend will accelerate this quarter as boardrooms digest the full scale of the tax cuts passed in December. Overall, US companies will buy back about $800bn of their stock this year, up from $525bn in 2017, and boost dividend payouts by about 10 per cent to a record $500bn. While US companies will lift their spending on investments, research and development by 11 per cent to more than $1tn this year, shareholder returns in the form of buybacks and dividends will grow by 21.6 per cent to nearly $1.2tn. The buyback spree will also lift the amount of profit companies make per share. S&P 500 companies are expected to report earnings growth of 17.1 per cent in the first quarter, which would the highest growth since the start of 2011, according to FactSet. That is up sharply from the rate of 11.3 per cent that was projected at the start of the year.

In contrast, US business investment in new plant, machinery and technology, while rising in gross amounts, is barely keeping pace with depreciation (wearing out) of existing fixed assets. Despite the recent acceleration in investment, net business investment has not re-attained levels achieved in 2014Q3 (let alone on the eve of the last recession)….

Draghi sees growth peaking. That’s a big problem because rates are negative and the ECB didn’t even end QE yet.

The Market Is Controlling Central Bank PolicyThe Citi Economic Surprise index for Europe is extremely negative showing reports are missing economists’ expectations. The ECB’s Mario Draghi responded to this recent weakness by stating growth may have peaked for the cycle. This is a reasonable assessment, but it’s more than an economic forecast. Every statement by central bankers has monetary policy implications. This could mean more dovish policy. This is an interesting predicament because the ECB has interest rates in the negatives and QE hasn’t even ended yet. The ECB will wait until July to decide the fate of QE.